Key Takeaways for Caris Life Sciences Stock

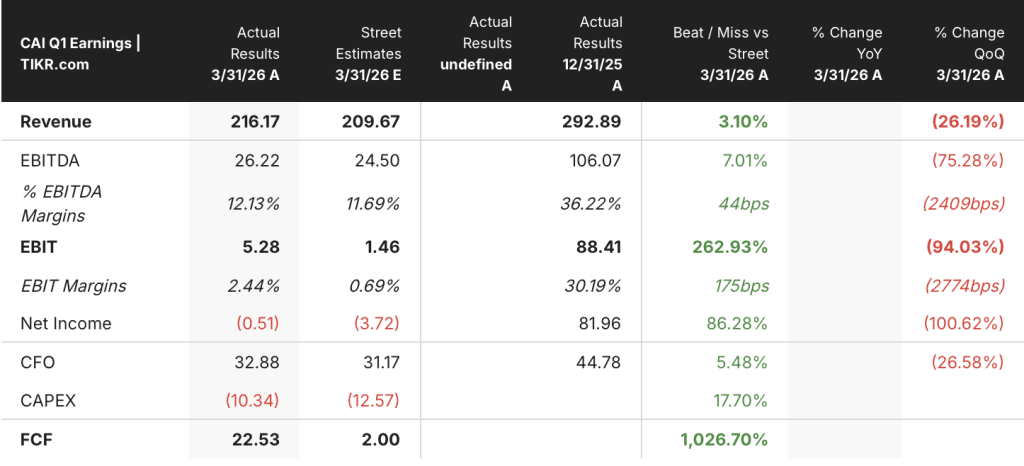

- Total revenue grew 79% year-over-year to $216.2 million in Q1 2026, with molecular profiling services leading at 85% growth to $211 million.

- Gross margins expanded from 47% in Q1 2025 to 65% in Q1 2026, an improvement of 18 percentage points in four quarters.

- TIKR’s mid-case model values Caris Life Sciences stock at approximately $159 by December 2030, implying around 560% total return from the current price of $18.

- Caris Detect delivered 60% Stage I and Stage II sensitivity with 99% asymptomatic specificity across 3,014 subjects in the Achieve 1 study.

The income statement shows 79% revenue growth with gross margins already at 65%, but the stock is trading near its 52-week low. Pull up Caris Life Sciences stock financial data on TIKR for free →

Caris Life Sciences Stock Turns Profitable on ASP Surge as Detect Launch Approaches

Caris Life Sciences (CAI) reported Q1 2026 revenue of $216.2 million, up 79% year-over-year, following a sales force realignment that disrupted January but drove record activations in February and March.

The company provides comprehensive molecular profiling for cancer patients, using whole exome and transcriptome sequencing across 23,000 genes to identify therapy options, clinical trial eligibility, and resistance markers. Every profiled patient feeds a proprietary dataset now exceeding 1 million cases, which powers both clinical AI tools and biopharma partnerships.

Molecular profiling services, which accounted for $211 million of Q1 revenue, grew 85% year-over-year on two engines running simultaneously: a 15% increase in clinical case volume to 52,800 cases, and a 61% increase in average selling price (ASP) for comprehensive profiling tests.

CFO Luke Power attributed the ASP expansion directly to MI Cancer Seek, the company’s FDA-approved whole exome and transcriptome tissue assay: tissue ASP increased 70% to over $4,300 and blood ASP increased 14% to just under $2,500, driven by payer contracting wins and over 225 million covered lives now secured for MI Cancer Seek.

CCO Bobby Hill stated on the Q1 earnings call: “Activations in February and March grew approximately 20% year-over-year compared with the same 2 months period last year.”

The exit run rate from February and March implied approximately 56,000 completed cases per quarter, supporting management’s guidance for over 58,000 cases in Q2, a 10% sequential increase from Q1.

Two new products launched in Q2: Caris ChromoSeq, a whole-genome therapy selection assay for hematological cancers priced at $3,228, which received MolDX approval; and Caris MI Clarity, a digital pathology AI test for breast cancer recurrence risk. Neither is included in the current full-year guidance of $1.0 billion to $1.02 billion in revenue.

The most consequential near-term catalyst remains Caris Detect, the company’s multi-cancer early detection test built on whole genome sequencing. The Achieve 1 study, a 3,014-subject cohort, reported 60% Stage I and Stage II sensitivity with 99% asymptomatic specificity. CSO Milan Radovich described the result as generated using only one of nine potential biological pillars, suggesting significant upside in performance as the platform matures. Commercial launch with Everlywell is planned for Q2 2026.

The sales realignment disrupted January but February and March proved the demand is real. The volume data, ASP trends, and Detect timeline are all on TIKR. See the full financial history of Caris Life Sciences stock on TIKR for free →

Is Caris Life Sciences Stock Undervalued? The Gross Margin Story Says Yes

Caris Life Sciences stock’s gross margin expanded from 38% in Q2 2024 to 65% in Q1 2026, a 27-percentage-point improvement across seven quarters driven almost entirely by ASP catching up to the cost of whole exome and transcriptome sequencing.

The cost of goods sold remained nearly flat across that same period, holding between $0.06 billion and $0.07 billion per quarter while revenue more than doubled, which is the operating leverage signature of a platform where fixed sequencing infrastructure serves a growing revenue base.

The gap between gross margin (65%) and operating margin (2%) in Q1 2026 reflects a deliberate reinvestment cycle: SG&A of $0.10 billion and R&D of $0.03 billion consumed nearly all of the gross profit generated during the quarter, as the company expanded its salesforce from 82 to 146 territories and prepared for the Detect launch.

Gross profit grew 148% year-over-year in Q1 2026 while total operating expenses grew only 18%, a ratio that shows the reinvestment is not outrunning the underlying margin engine.

The trough in operating margin came in Q2 2024 at negative 67%, crossed into positive territory in Q3 2025 at 15%, peaked at 30% in Q4 2025, and compressed to 2% in Q1 2026 as the company front-loaded Detect and salesforce investments. That compression is an investment cycle, not a margin reversal.

CAI Has Closed the Gross Margin Gap on GH and Now Trades at Parity With Both Peers

Caris Life Sciences stock’s gross margin sat 22 percentage points below Guardant Health (GH) in Q2 2024, with CAI at 38% and GH at 59%, a gap that reflected CAI’s earlier stage of reimbursement maturity rather than any structural cost disadvantage.

By Q3 2025, Caris Life Sciences stock had closed that gap entirely, reaching 68% against GH’s 65%, the first quarter in which CAI crossed above its liquid biopsy peer on gross margin, driven by the same ASP expansion engine that pushed tissue pricing up 70% year-over-year.

Tempus AI (TEM) held gross margins in the 60% to 63% range throughout the entire comparison period, providing a stable ceiling that both CAI and GH have now reached, which suggests 65% represents the category norm for scaled molecular diagnostics platforms rather than a Caris-specific ceiling.

The strategic implication for Caris Life Sciences stock is that the gross margin catch-up trade is largely complete, and the next margin expansion lever sits in operating expense normalization as Detect, ChromoSeq, and MI Clarity convert from investment-stage launches into recurring revenue contributors at the existing 65% gross margin base.

TIKR’s $159 Mid-Case on CAI Stock: What Has to Hold for the Numbers to Work

TIKR’s base case values Caris Life Sciences at approximately $159 by December 2030, implying around 560% total return from the current price of $18, or roughly 51% annualized over 4.5 years.

If revenue growth sustains around the mid-case trajectory of approximately 13% CAGR with net income margins converging toward 18%, the model supports that target. The mechanism is the gross margin base already established at 65%, plus the operating leverage embedded in a fixed sequencing cost structure as revenue compounds from new products including ChromoSeq, MI Clarity, and Detect.

In the low case, with approximately 12% revenue CAGR and approximately 17% net income margins, the model produces a stock price of around $112 by December 2030, implying around 523% total return, or roughly 24% annualized.

In the high case, with approximately 15% revenue CAGR and approximately 19% net income margins, the model produces approximately $218, implying around 1,113% total return, or roughly 34% annualized.

The condition separating the mid from the low case is not revenue volume, which is tracking ahead of guidance, but the pace of operating expense normalization as Detect and new salesforce additions mature into recurring revenue contributions.

Is Caris Life Sciences stock a buy right now?

Caris Life Sciences stock is trading near its 52-week low of $17 while the underlying business is delivering 79% revenue growth and 65% gross margins.

TIKR’s mid-case model values the stock at approximately $159 by December 2030, implying around 560% total return from current levels.

The investment case depends on the company sustaining gross margin discipline while converting Detect and ChromoSeq launches into durable revenue streams.

Should You Invest in Caris Life Sciences, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Caris Life Sciences, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Caris Life Sciences, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CAI stock on TIKR for Free →