Key Stats for Lam Research Stock

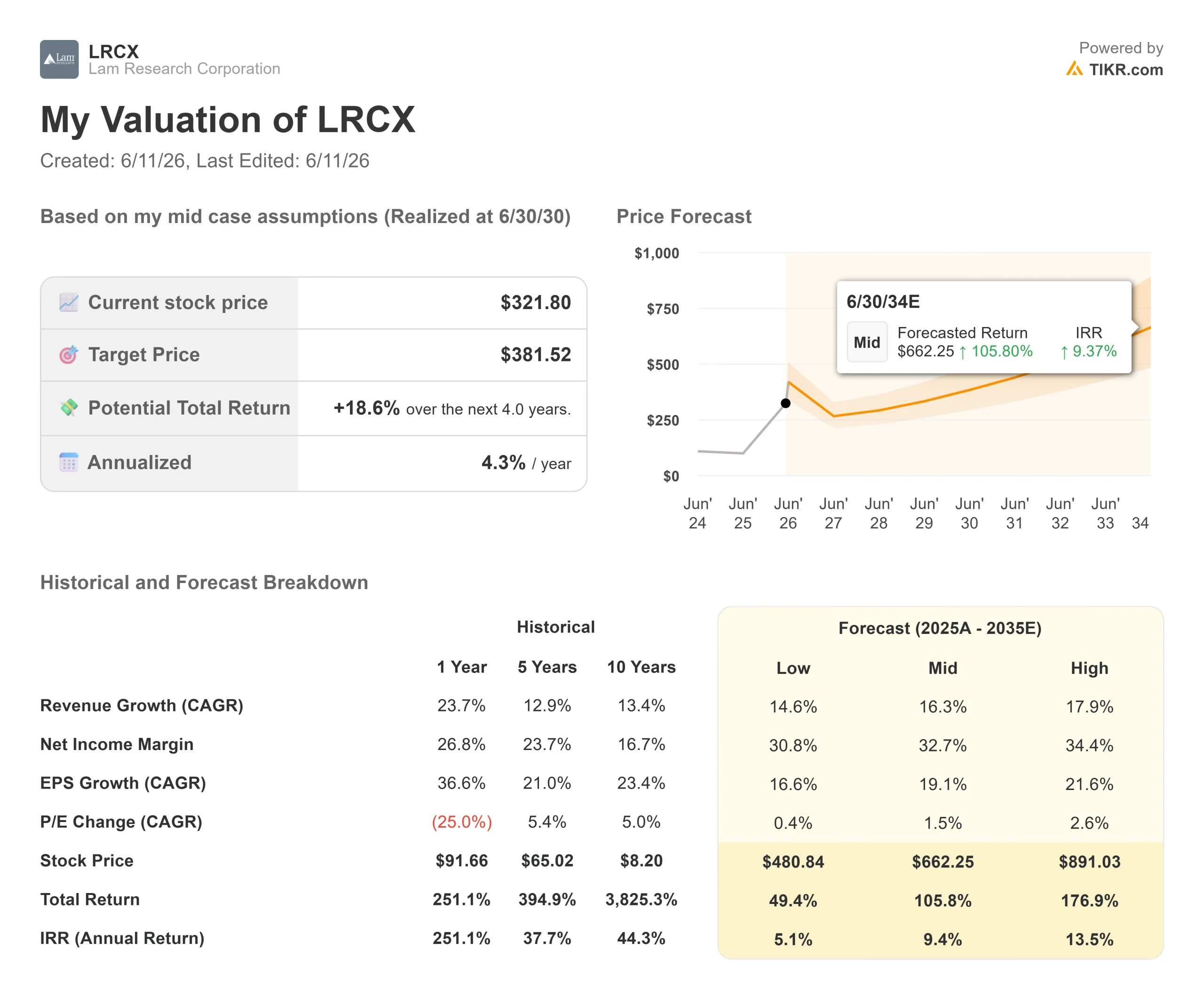

- Current Price: $359.62

- TIKR Mid-Case Target: ~$662

- Potential Total Return (Mid): ~106%

- Annualized IRR (Mid): ~9% per year

- Earnings Reaction: (2.63%) on April 22, 2026

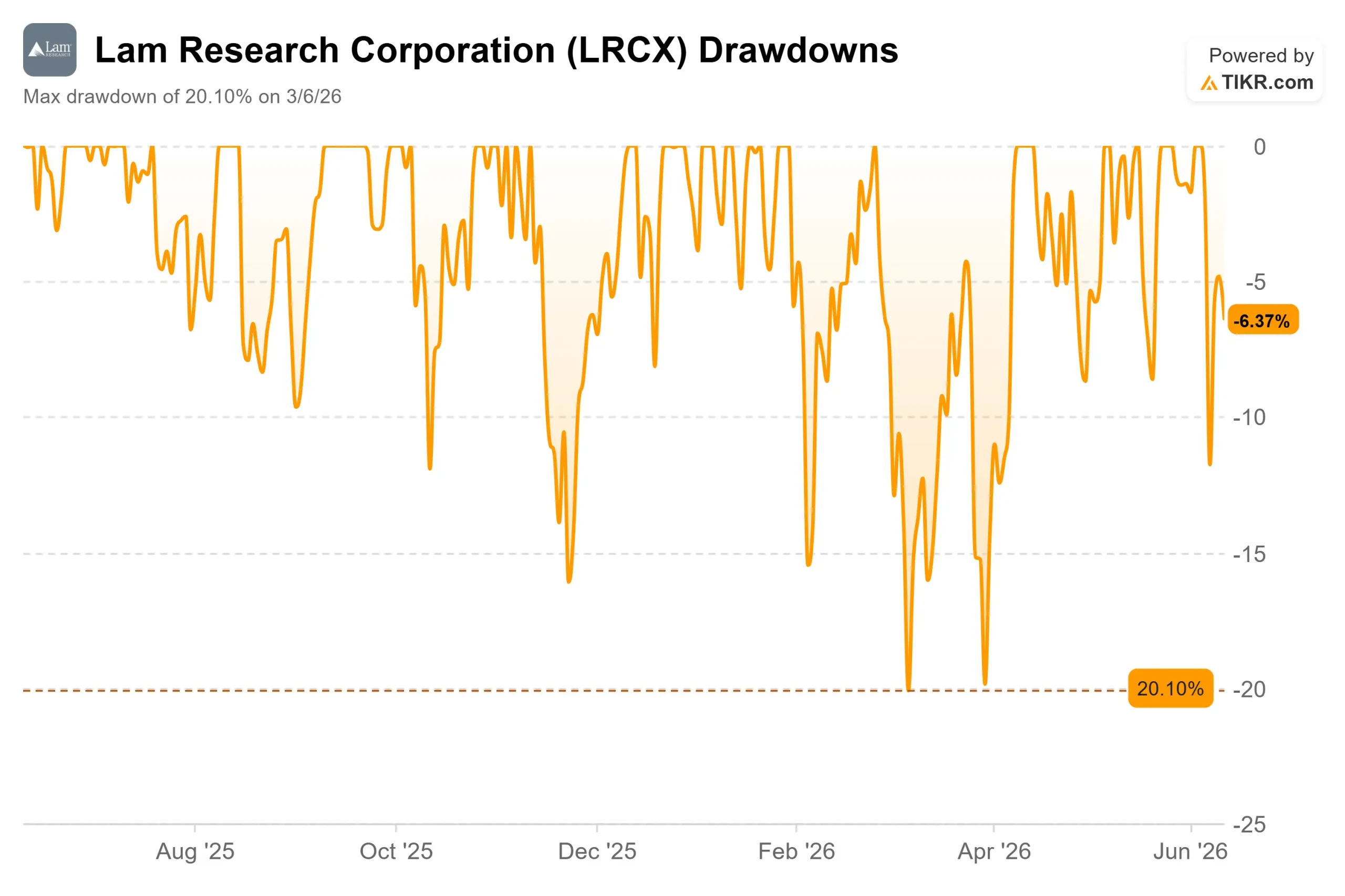

- Max Drawdown: (20.10%) on 3/6/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Lam Research Corporation (LRCX) closed at $359.62 on June 11, breaking above its prior 52-week high of $349.09. But behind the record price is something more durable than a momentum trade: three consecutive quarters of record revenue, a wafer fabrication equipment (WFE) market running above its own forecasts, and a CFO who just described demand visibility as the richest he has seen in his entire career.

That last point came from Douglas Bettinger, Executive Vice President and CFO, at the Bank of America 2026 Global Technology Conference on June 2. Speaking about multi-year conversations with customers, he said: “The robustness of these conversations is as strong as I’ve ever seen it, frankly, in all the time I’ve been in the industry.” For a financially conservative executive, that is a precise and meaningful statement.

What Drove the Recent Surge

LRCX gained 11.75% on June 11, capping a three-day rally driven by a wave of analyst target hikes. UBS raised its price target to $375 from $310 on June 9. Cantor Fitzgerald lifted its target to $425 from $320, and Barclays raised to $335 from $275, both on June 11, according to TipRanks. Wells Fargo raised its target to $365 from $320 on June 1, maintaining an Overweight rating.

These upgrades were built on Lam’s Q3 fiscal 2026 earnings report on April 22, where revenue came in at $5.841 billion, up 24% year over year, and adjusted EPS of $1.47 beat the top end of the company’s own guidance range. The stock fell 2.63% on earnings day. Since then, LRCX has climbed roughly 70%.

One detail every new buyer should note: LRCX has already run past the Street consensus. According to TIKR, the mean analyst price target across 32 estimators stood at approximately $322 as of June 10; the stock closed at $359.62 on June 11. When a stock clears consensus, the burden shifts to the bulls. The next round of target hikes needs to follow the price higher, or the premium becomes harder to defend.

See historical and forward estimates for Lam Research stock (It’s free!) >>>

What Wall Street Is Still Missing

Most LRCX coverage rests on the same thesis: AI drives chip demand, chip demand drives WFE, and Lam makes WFE equipment. That is correct and incomplete. The BofA conference surfaces two structural points that rarely get discussed.

The served available market (SAM) is expanding faster than most models assume. SAM is the share of total WFE spending addressable by Lam’s etch and deposition tools. At Lam’s early 2025 Investor Day, SAM stood at roughly 32% of total WFE. By the BofA conference, Bettinger confirmed it had already reached the mid-30s and expects it to reach the high 30s over the next several years. “We’re already in the mid-30s because of the evolution of these architectures,” he said.

The reason is structural. Everything at the leading edge of chip manufacturing is moving into three dimensions: gate-all-around transistors in foundry logic, high-bandwidth memory (HBM) stacks in DRAM, growing NAND layer counts, and through-silicon via (TSV) steps in advanced packaging. As Bettinger put it: “When things inflect in the third dimension, etch and deposition intensity grow. That’s all we do.” Foundry accounted for 54% of Lam’s systems revenue in the March 2026 quarter and 59% the quarter before. The stock’s reputation as a NAND-only play is significantly outdated.

CSBG is a recurring revenue engine that most investors underweight. The Customer Support Business Group, which Bettinger called “my favorite part of the business model,” crossed $2 billion in quarterly revenue for the first time in Q3 FY2026, up 25% year over year. It runs on spares, service, upgrades, and Lam’s Reliant mature-node tools. It does not need new equipment orders to grow its compounds through the utilization of the installed base. “Fabs are always running,” Bettinger said, “which means they consume spares and service.” That free cash flow funds Lam’s commitment to return 85% of FCF to shareholders, including 15% annual dividend growth for three consecutive years, as stated explicitly by Bettinger in the conference.

The 2027 setup is the most underpriced element. Bettinger said the industry is constrained right now by clean room space, meaning demand exceeds what fabs can currently absorb. That unmet demand rolls into 2027 as new fab projects complete. “I think ’27 is going to be a pretty darn good year,” he said. Morgan Stanley, which upgraded LRCX to Overweight in May, independently projects NAND systems growth of 59% in calendar 2027, which would push NAND WFE above its 2021 peak. NAND is Lam’s strongest end market and the segment that has grown slowest this cycle. When it accelerates, Lam’s outperformance versus WFE tends to widen.

How Lam Stacks Up Against Peers

Lam is not cheap. According to TIKR’s Competitors page, LRCX trades at 36.67x NTM EV/EBITDA, above Applied Materials (AMAT) at 28.73x and ASML Holding (ASML) at 33.83x. KLA Corporation (KLAC) is the only direct peer with a higher multiple, at 44.87x. The peer group means NTM EV/EBITDA is 35.48x, putting Lam modestly above the group.

Morgan Stanley’s May upgrade explicitly rotated out of AMAT and into LRCX, arguing that NAND revisions now look more favorable than DRAM and that Lam’s growing SAM in foundry and advanced packaging makes it better positioned for 2027. Whether 36.67x is the right multiple for those advantages is the question every buyer at current prices has to answer.

See how Lam Research performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $359.62

- TIKR Mid-Case Target: ~$662

- Potential Total Return: ~106%

- Annualized IRR: ~9% per year

See analysts’ growth forecasts and price targets for Lam Research stock (It’s free!) >>>

The mid-case runs on a 16.3% revenue CAGR, driven by two factors: the multi-year WFE expansion in AI-driven DRAM, NAND conversion, and advanced packaging; and CSBG compounding on a growing installed base. On margins, the model projects net income expanding to around 33% from roughly 29% in FY2025, as manufacturing scale from the Malaysia facility and mix shift toward higher-margin services take hold.

The bull case (around 18% revenue CAGR, net income margins near 34%) produces approximately $891, a roughly 14% IRR. The low case (around 15% CAGR, margins near 31%) produces approximately $481, around 49% total return, still positive, but likely insufficient for a volatile semiconductor equipment name held through a cycle trough.

The primary risk is timing. Clean room construction takes years. If fab projects expected in 2027 slip to 2028, systems revenue faces a gap quarter. China, described by management as “flattish to slightly up” in 2026 and declining as a percentage of total revenue, adds a second layer: further export restrictions could clip estimates quickly.

Conclusion

The next test is July 29, 2026, Lam’s Q4 FY2026 earnings date. Skip EPS; Lam has beaten estimates every quarter for over a year. Watch the June quarter revenue result against management’s guidance of approximately $6.6 billion, which Lam provided at the April earnings call. A result at or above that figure confirms Bettinger’s BofA commentary with hard data. A result meaningfully below $6.2 billion, suggesting clean room constraints are pushing more demand into 2027 than planned, and the stock will likely correct sharply from a multiple that has already priced in the best-case setup.

Bettinger said his customer conversations right now are as strong as he has ever seen them. July 29 is when the numbers either back that up, or they don’t.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Lam Research?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lam Research, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lam Research alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Lam Research on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!