Key Takeaways for Formula One Group Stock

- Formula One Group stock reported Q1 2026 revenue of $711 million, up 59% year over year, beating the $670 million consensus estimate.

- Operating income swung from a loss of $67 million in Q1 2025 to a gain of $64 million in Q1 2026, a 196% improvement driven by revenue scaling faster than costs.

- The TIKR mid-case model values Formula One Group stock at approximately $165, implying around 82% total return over 4.5 years at roughly 14% annualized.

- CEO Derek Chang confirmed the Apple TV partnership is delivering higher viewership and a younger, more female audience across the first three U.S. races, reinforcing the long-term commercial foundation.

Formula One Group Delivered Its Highest Q1 Revenue on Record as Apple and a Third Race Compressed the Mispricing

Formula One Group (FWONK), the Liberty Media tracking stock that holds commercial rights to the FIA Formula One World Championship and recently acquired MotoGP, reported Q1 2026 revenue of $711 million following its May 7 earnings call, the highest first-quarter figure the series has ever recorded.

The company held three races in Q1 2026 versus two in Q1 2025, with Japan added to the current-year period, and the calendar shift drove outsized revenue recognition across every stream.

CFO Brian Wendling explained the mechanism directly on the Q1 earnings call: “Revenue grew 53%. Adjusted OIBDA grew 102% driven by the extra race held and growth across all revenue streams from underlying contractual fee increases.”

With three of 22 scheduled races recognized in the quarter, approximately 14% of season-based revenue flowed into Q1, compared to roughly 8% when only two of 24 races were recognized in the prior-year period.

Sponsorship was a standout driver, with new partners including Standard Chartered and FanDuel added to a renewal cycle that CEO Derek Chang described as increasingly front-loaded, with partners coming back early before expiry.

Formula One Group stock’s Apple TV partnership, now in its first full U.S. season, delivered early results that Chang called “everything that we envisioned when we did the deal with them last year and more,” with viewership rising through the first three races, the audience skewing younger and more female, and the platform enabling broadcast innovations including IMAX screenings and Netflix syndication that would have been structurally blocked under a traditional linear rights agreement.

The Paddock Club, Formula One’s premium trackside hospitality product, is already sold out for nearly all remaining races in the season, with over 65,000 tickets sold as of the Q1 call, matching the full-year 2025 total attendance in just the opening months.

The 2026 season is running on a 22-race calendar versus 24 in 2025 after the Bahrain and Saudi Arabian Grands Prix were cancelled in April due to the conflict in the Middle East, and management flagged Q2 as the most structurally impaired quarter with only five races expected versus nine in Q2 2025.

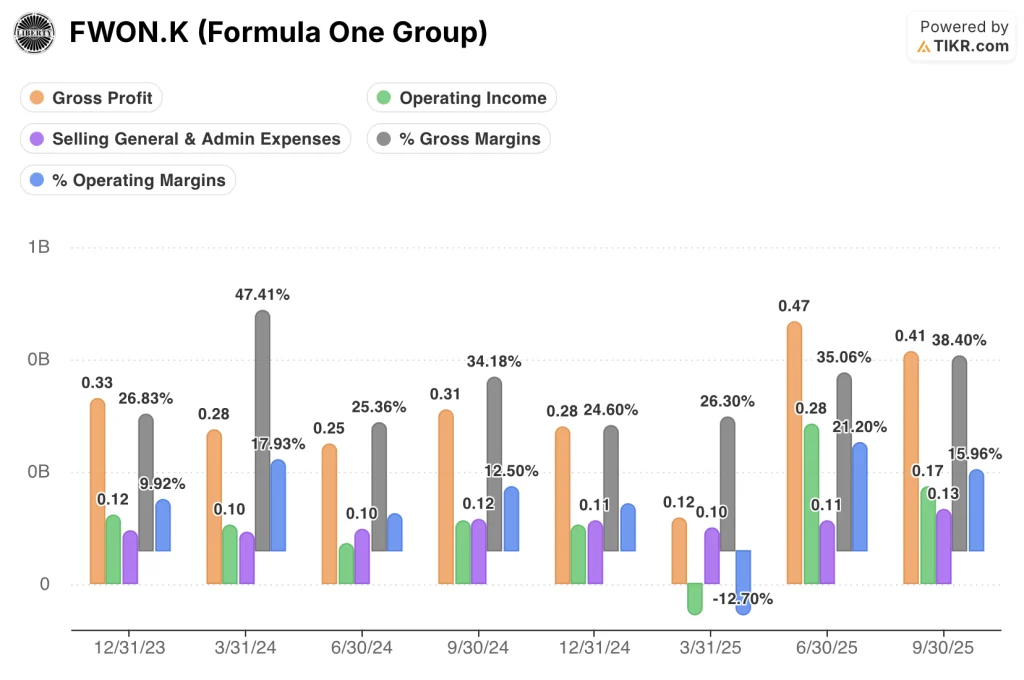

Formula One Group Stock’s Gross Margin Expansion in Q1 2026 Shows the Operating Leverage the Market Is Not Pricing

Formula One Group stock’s gross margins expanded from 26% in Q1 2025 to 42% in Q1 2026, a 16-point improvement in a single year that reflects the revenue base growing materially faster than the cost of goods sold.

Gross profit reached $298 million in Q1 2026 against $413 million in cost of goods sold, compared to a gross profit of $117 million on $330 million in COGS in Q1 2025, demonstrating how the additional race event and contractual fee increases dropped directly into gross profit.

Operating income landed at $64 million in Q1 2026 after a $67 million operating loss in Q1 2025, a $131 million swing in four quarters that was powered by revenue scaling at 59% while total operating expenses grew at a fraction of that rate.

Operating margins reached 9% in Q1 2026 against a negative 13% in the prior-year period, and the trajectory across the trailing four quarters, from a negative reading in Q1 2025 through 21% in Q2 2025, 16% in Q3 2025, and now 9% in Q1 2026 on the lowest-revenue quarter of the seasonal cycle, confirms that margin volatility is calendar-driven, not structural.

SG&A pressure was real in Q1 2026, with CFO Wendling citing unfavorable foreign exchange, higher personnel costs, and increased IT spend, partially offset by lower marketing expense tied to the prior year’s 75th anniversary event, which means the SG&A headwind is front-loaded and partially non-recurring.

Formula One Group Stock Leads Live Nation on Operating Margins Across Every Comparable Quarter, but TKO’s Consistency Frames the Gap

Formula One Group stock posted a 21% operating margin in Q2 2025 and 15% in Q3 2025, outpacing Live Nation Entertainment (LYV), which delivered 7% and 9% in the same periods, a spread of 14 and 6 percentage points respectively that reflects the structurally different cost bases of a rights holder versus a live event operator.

TKO Group Holdings (TKO), which holds the UFC and WWE rights portfolios under a structure most comparable to Formula One Group’s commercial model, ran operating margins of 21% in Q2 2025 and 16% in Q3 2025, sitting near parity with Formula One Group stock in both quarters and demonstrating that a sustained 15% to 21% operating margin band is achievable for a sports rights business at scale.

The Q1 2025 trough, where Formula One Group stock printed negative 13% against TKO’s positive 22% and Live Nation’s positive 3%, was calendar-driven rather than structural, and the 34-point recovery to 21% in Q2 2025 confirms that Formula One Group stock’s margin profile, when the race calendar is fully loaded, competes directly with the strongest rights-based peers in the entertainment sector.

Is Formula One Group Stock Undervalued in 2026? TIKR’s $165 Model Prices the Rights Base, Not the Race Count

TIKR’s mid-case model values Formula One Group stock at approximately $165 by December 2030, implying around 82% total return from the current price of $90, or roughly 14% annualized over the next 4.5 years.

If contracted media rights with Apple, Sky, CCTV, and other partners continue to compound at the rate locked in through recent renewals, and if the 22-race 2026 calendar proves temporary rather than durable, the path to approximately $165 requires around 7% annual revenue growth, which sits inside the range management has delivered for four consecutive years.

If the Middle East disruption extends beyond 2026 and the race calendar contracts further, the low-case model output of approximately $165 by 2035 still implies around 7% annualized return from current levels, meaning the downside scenario carries more upside than the current market price reflects.

If MotoGP’s commercialization ramp accelerates alongside Formula One’s contracted base, the high-case output of approximately $254 by 2035 implies roughly 13% annualized return, a scenario that requires no heroic assumptions beyond Liberty Media executing the same playbook at MotoGP that it ran at Formula One.

Is Formula One Group stock a buy in 2026?

Formula One Group stock trades at $90 against a TIKR mid-case target of approximately $165, implying around 82% total return over 4.5 years at roughly 14% annualized.

The Q1 2026 operating income swing from a $67 million loss to a $64 million gain shows the business has real operating leverage at elevated revenue levels.

The contracted commercial base, including multi-year media deals with Apple, Sky, and CCTV, is intact regardless of the 2026 calendar disruption.

Is Formula One Group stock undervalued or overvalued?

The TIKR low-case model, which assumes conservative revenue growth, still produces approximately $165 per share by 2035, implying the downside scenario carries a positive annualized return from the current $90 price.

Gross margins expanded 16 percentage points year over year in Q1 2026, from 26% to 42%, signaling that the underlying cost structure is not growing proportionally with the revenue opportunity.

The market appears to be pricing the 2026 race count reduction as structural impairment, not a one-year disruption.

Should You Invest in Formula One Group?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Formula One Group stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Formula One Group alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FWONK stock on TIKR for Free →