Key Stats for Marvell Technology Stock

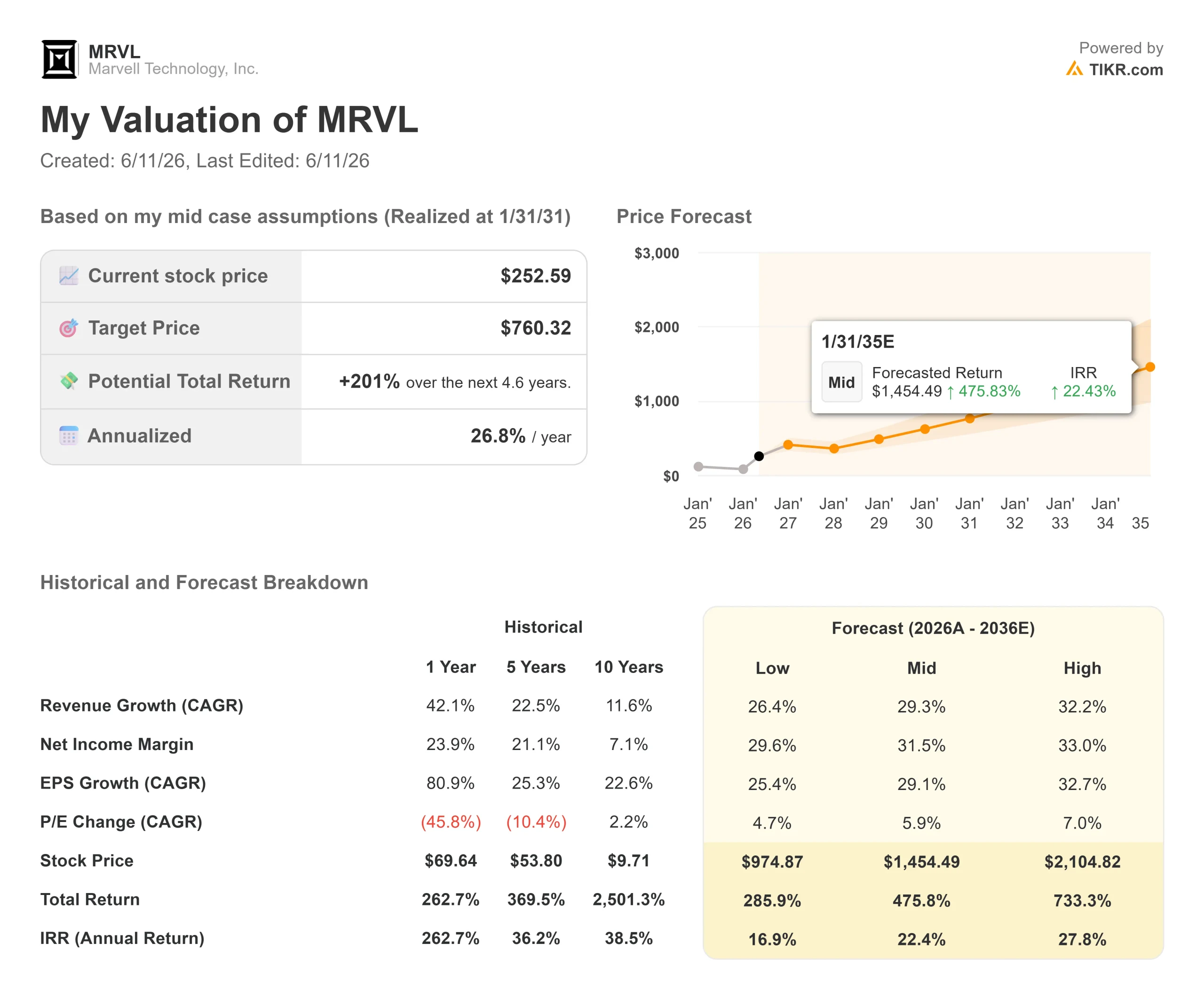

- Current Price: $278.02

- Target Price (Mid): ~$760

- Potential Total Return: ~201%

- Annualized IRR: ~27% / year

- Street Consensus Target: ~$233

- Earnings Reaction: +3.09% (reported 5/27/26)

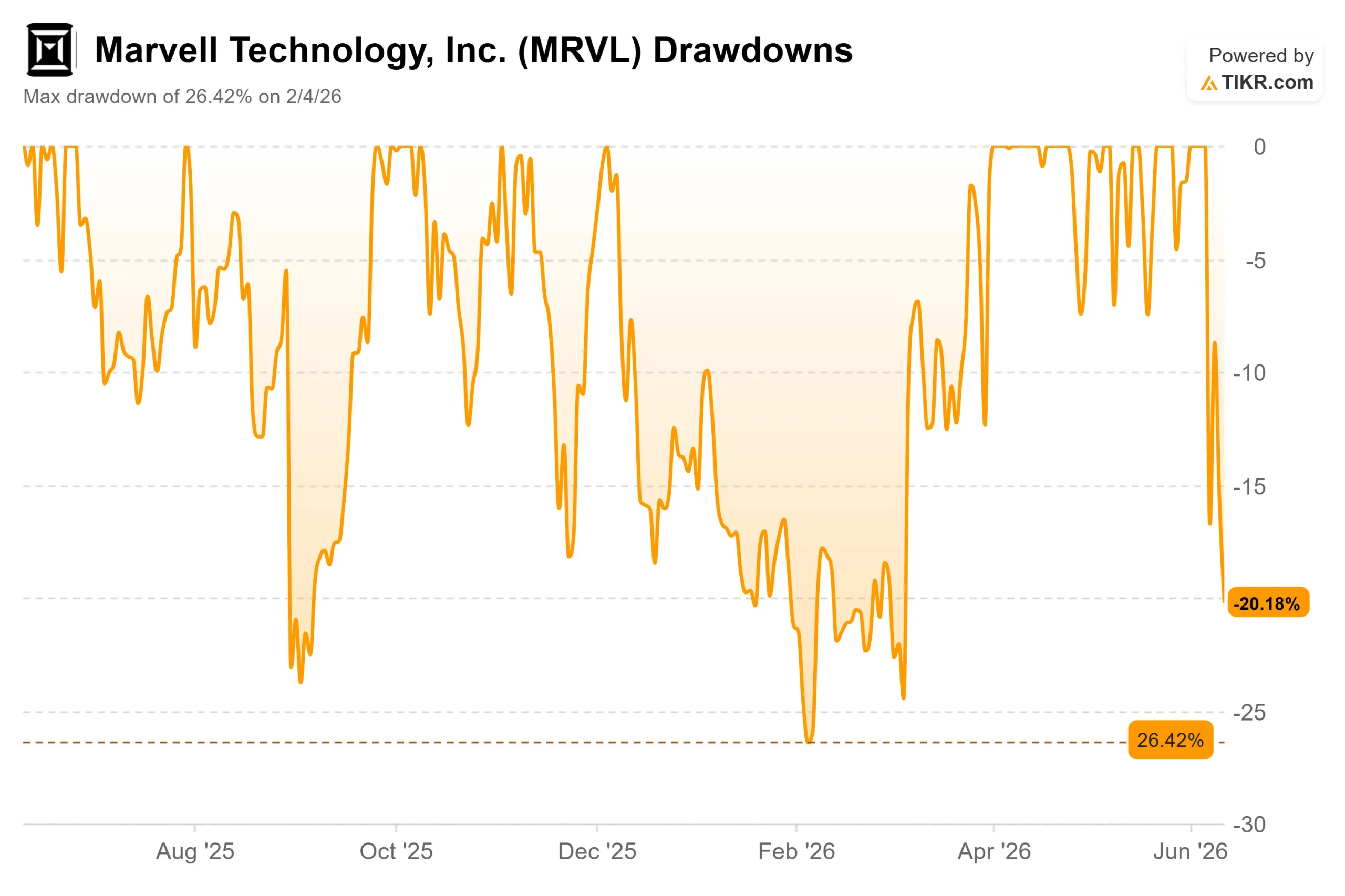

- Max Drawdown: 26.42% on 2/4/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Marvell Technology (MRVL), the data infrastructure chipmaker behind the optical interconnects and custom silicon inside the world’s largest AI clusters, just put together one of the fastest rallies in semiconductor history. From the mid-$160s in late May to a 52-week high of $324.20 on June 3, the stock surged over 90% in roughly two weeks before pulling back to the $252–$278 range. The move was driven by three catalysts that hit simultaneously, and understanding each one is the only way to answer whether this pullback is an entry point or a trap.

Three Catalysts, One Week

Earnings beat. On May 27, Marvell reported Q1 fiscal 2027 revenue of $2.418 billion, up 28% year-over-year and above analyst estimates of $2.408 billion, per TIKR’s Beats & Misses data. Non-GAAP EPS came in at $0.80, beating the $0.79 estimate. Management guided Q2 revenue to $2.7 billion at the midpoint, implying 35% year-over-year growth, and raised its full-year outlooks for fiscal 2027 and 2028. The stock moved +3.09% on the day, modestly, relative to what followed.

NVIDIA partnership. On March 31, NVIDIA announced a $2 billion investment in Marvell and integrated the company into NVLink Fusion, a rack-scale platform that lets hyperscalers build semi-custom AI infrastructure fully compatible with NVIDIA’s software stack. That investment converted a thesis into an alliance.

Jensen Huang’s endorsement. On June 2, NVIDIA CEO Jensen Huang appeared onstage at COMPUTEX 2026 alongside Marvell CEO Matt Murphy and called Marvell “the next trillion-dollar company.” The stock jumped over 30% in a single session. S&P Dow Jones Indices then confirmed Marvell would join the S&P 500 on June 22, replacing Pool Corp. Passive funds tracking the benchmark must now hold MRVL, meaning billions of dollars in programmatic buying is expected to concentrate around the June 22 effective date.

See historical and forward estimates for Marvell Technology stock (It’s free!) >>>

What the BofA Conference Reveals

Speaking at the Bank of America Global Technology Conference on June 3, the same day shares hit their all-time high, CEO Matt Murphy made the strategic case that most investors are missing.

Marvell is not a GPU company. Connectivity and I/O make up the majority of its revenue, which is exactly why NVIDIA invested. “We’re very complementary to the rest of the ecosystem,” Murphy said. “We’re not battling it out in some compute war.” Because Marvell’s chips are required whether a cluster runs NVIDIA GPUs, AMD accelerators, or custom XPUs, the business has a kind of structural independence that pure compute players lack.

Murphy also described three businesses each approaching $1 billion in annual revenue that barely existed at scale three years ago: cloud switching (on pace for over $1 billion this fiscal year), DCI (data center interconnect, the long-haul optical links that move AI workloads between facilities), and broadband analog components for emerging 6G and AI radio networks.

The part that deserves most attention is what is not in any analyst model yet. Murphy stated clearly that scale-up switching the chip-to-chip links inside a single AI cluster contributes $0 to current revenue or guidance. Marvell’s Head of IR, Ashish Saran, put the opportunity plainly at the same conference: “Scale-up switching is completely greenfield. It’s fully available. We could be leading the market from day 1.”

On co-packaged optics (CPO, meaning optical components integrated directly into the chip package rather than connected externally), Murphy said the scale-up optics revenue target for the next fiscal year has already doubled from $150 million at the time of the Celestial AI acquisition in February 2026 to $300 million, going from $0 this year to $300 million in twelve months.

Valuation: Expensive, But Not Without a Case

At $278.02, Marvell trades at 44.22x NTM EV/EBITDA and 55.73x NTM P/E. Per TIKR’s Competitors table, NVIDIA trades at 16.05x NTM EV/EBITDA, Broadcom at 19.03x, and the sector median sits at around 20x. Marvell commands a large premium, and the growth rate is the justification.

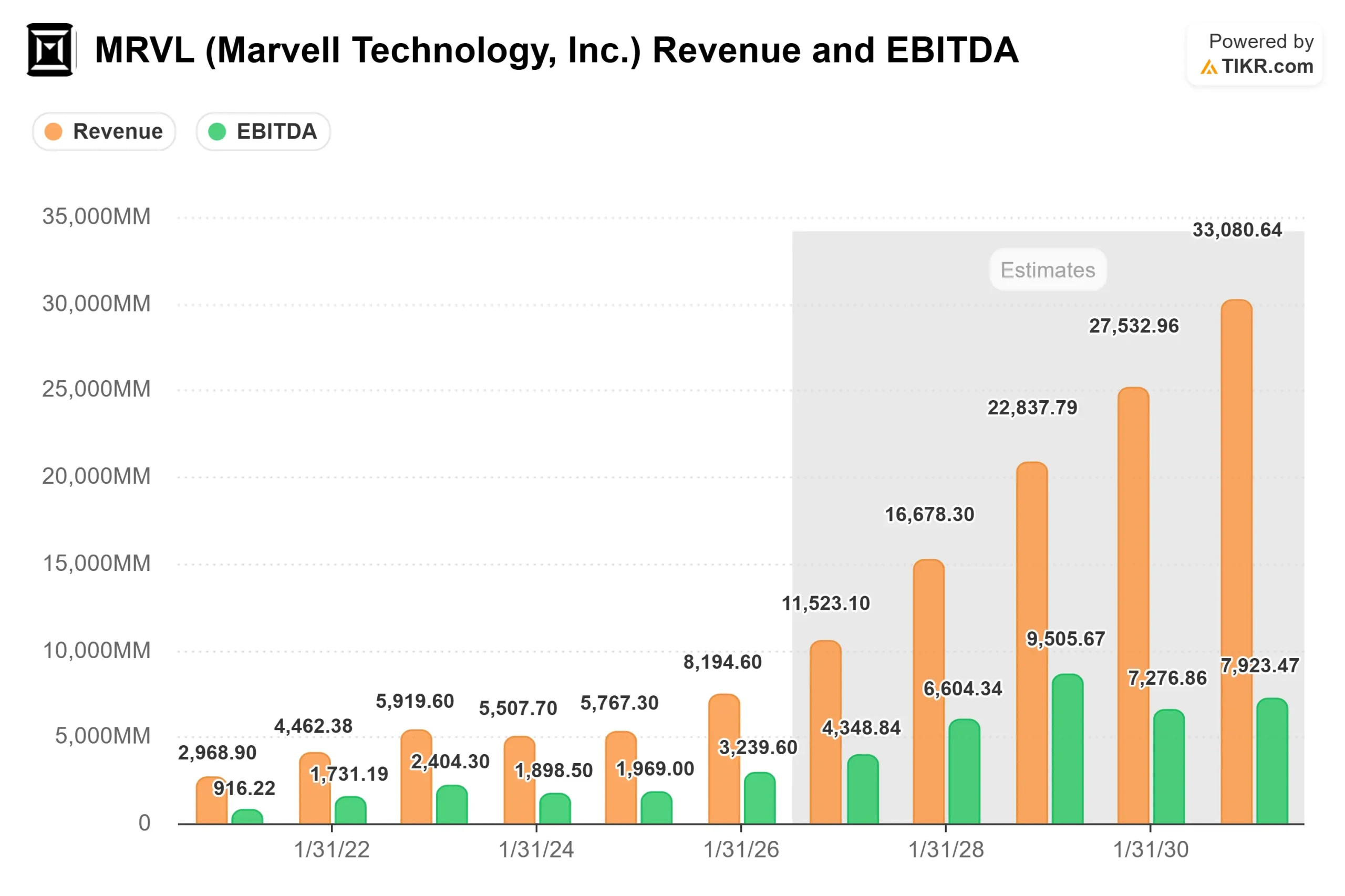

TIKR’s Actuals and Forward Estimates show free cash flow supported by revenue growing from $8.2 billion in fiscal 2026 to approximately $11.5 billion in fiscal 2027 and approximately $16.7 billion in fiscal 2028. That represents a two-year forward revenue CAGR of approximately 43%, the fastest projected growth rate in large-cap semiconductors. EBITDA profit margins are expected to compress to 37.7% in fiscal 2027 as Marvell absorbs the Celestial AI and XConn acquisitions, then recover to approximately 40% in fiscal 2028 as scale kicks in.

The risk is not that the business is broken. It is that the price already prices in much of what has to go right. Murphy acknowledged at BofA that the company’s $16.5 billion fiscal 2028 target assumes hyperscaler CapEx moderates by around 30%. If cloud spending stays elevated, Marvell likely outperforms. If it slows harder than assumed, the model faces real pressure. Customer concentration is also a live risk: per Marvell’s fiscal 2026 annual filing, two customers each accounted for at least 10% of total revenue. Murphy’s answer is diversification: 15 to 18 custom products across multiple hyperscalers in production by fiscal 2028, with no single program capable of breaking the company’s trajectory.

See how Marvell Technology performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $278.02

- Target Price (Mid): ~$760

- Potential Total Return: ~201%

- Annualized IRR: ~27% / year

See analysts’ growth forecasts and price targets for Marvell Technology stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of approximately 29% from fiscal 2026 through fiscal 2036, with net income margins expanding from 30.1% in fiscal 2026 toward approximately 31.5% in the mid-case as operating leverage takes hold. The two revenue drivers are optical interconnect compounding Marvell’s silicon photonics business, which has been in production for ten years, with 15 billion field hours across four manufacturing generations and custom silicon breadth, with custom revenue expected to more than double year-over-year in fiscal 2027 per Murphy’s own guidance.

The primary risk is CapEx timing. If hyperscaler AI spending moderates faster than assumed, the 29% CAGR becomes harder to sustain. The upside scenario, if scale-up networking revenues begin materializing as Murphy described, points to the model’s high-case target of approximately $2,100 by January 2035, though that depends on a longer compounding runway than the base case requires.

Conclusion

The most important near-term signal is not Q2 earnings on August 26, though the Street expects $2.7 billion in revenue. It is whether MRVL holds above the $252–$260 range through the S&P 500 inclusion on June 22. If the stock absorbs the index buying without giving it back, conviction capital is building alongside the passive flows. A failure to hold that range would suggest the move pulled forward more demand than the fundamentals can currently support.

The thesis rests on one number: $16.5 billion in fiscal 2028 revenue. Murphy has raised that target three times in under six months. If the August call delivers a fourth upward revision, the valuation debate shifts in a decisive direction.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Marvell Technology?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Marvell Technology, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marvell Technology alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Marvell Technology on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!