Key Stats for LendingClub Stock

- Current Price: $17.18

- Street Target (Mean): ~$23

- TIKR Mid-Case Target: ~$37

- Potential Total Return (Mid): ~117%

- Annualized IRR (Mid): ~18% / year

- Max Drawdown: -38.28% (March 18, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

LendingClub (LC) stock had been grinding sideways heading into earnings, sitting about 21% below its 52-week high of $21.67 and carrying real uncertainty.

Bulls argued that LendingClub’s credit outperformance and origination momentum had created a mispriced opportunity. Bears pointed to the absence of expected Fed rate cuts and rising expenses.

The question the market was asking: Can this company grow profitably in a higher-for-longer rate environment?

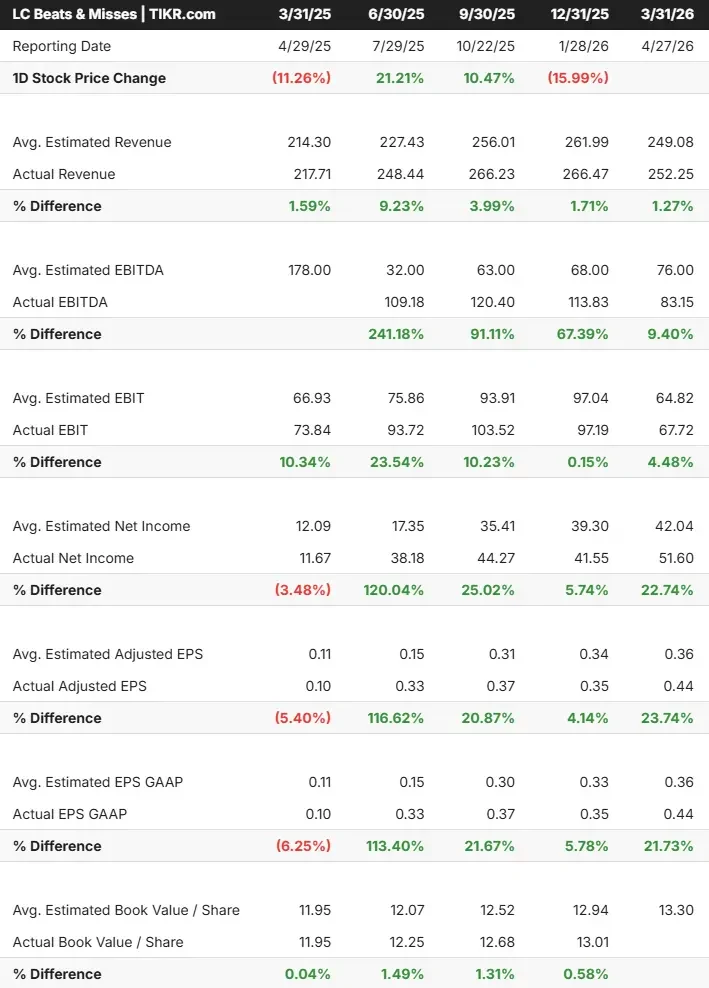

After the close on April 27, LC stock jumped 13% to $19.73 immediately following the results. LendingClub’s investor relations materials show the company delivered Q1 2026 net revenue of $252.3 million, up 16% year-over-year, with record pretax income of $67.3 million. Diluted EPS came in at $0.44, more than quadrupling from a year ago and beating the high end of guidance. Originations reached $2.7 billion, up 31%, above the high end of guidance.

Two strategic moves landed alongside the print.

On April 21, LendingClub announced it is rebranding as Happen Bank this summer, signaling its evolution from online lender to a diversified digital-first bank.

Simultaneously, the company launched home improvement financing through Wisetack, a platform embedded with over 40,000 contractors, targeting the estimated $500 billion U.S. home improvement market with loans up to $65,000.

“We’re starting 2026 with exceptional momentum, delivering 31% year-over-year growth in originations while achieving record pretax earnings of $67 million and ROTCE of 14.5%,” said Scott Sanborn, CEO of LendingClub.

On the home improvement launch, Sanborn was direct on the earnings call: “The bigger contribution will really be next year. This year will be kind of laying the pipes.” Home improvement is a 2027 earnings driver, not a 2026 one.

See historical and forward estimates for LendingClub stock (It’s free!) >>>

Is LendingClub Undervalued Today?

Even after the 13% post-earnings jump, LC still trades at just 9.4x NTM earnings and 1.82x NTM EV/EBITDA. For perspective, Upstart Holdings trades at 14.45x NTM EV/EBITDA and Dave Inc. at 12.31x, per TIKR’s Competitors page. LendingClub is growing originations at 31%, posting a 27% pretax profit margin, and has returned to record earnings. The discount to those peers is hard to square with the fundamentals.

The credit picture is the clearest argument for the stock. LendingClub has sustained more than 40% credit outperformance relative to competitors across five years of quarterly vintages, as cited by Sanborn on the call. Net charge-offs fell to 3.5% from 6.1% a year ago, and provision for credit losses dropped to less than $1 million in Q1. CFO Andrew LaBenne acknowledged charge-offs will likely normalize toward 5% as the newer vintage season, but the trajectory has consistently beaten management’s own forecasts.

The risks are genuine. The company entered 2026 expecting 75 basis points in Fed rate cuts that are no longer coming. LaBenne confirmed on the call that loan sale prices will likely come down in Q2 because all Q1 deals were priced before the U.S.-Iran conflict pushed benchmark rates higher.

That headwind is already embedded in the maintained full-year EPS guidance of $1.65 to $1.80. Expenses also rose 28% year-over-year in Q1, partly tied to the fair value accounting transition and the rebuild of paid marketing channels that are still in early stages.

What the market may be underpricing is the sum of three overlapping catalysts: the Happen Bank rebrand targeting deposit growth, the home improvement vertical entering a $500 billion market, and over 60 active AI initiatives that have already driven a greater than 90% loan automation rate and record-low production costs per issued personal loan. The Street’s mean target of around $23 implies about 31% upside from the April 27 close, with the highest analyst target sitting at $29.

See how LendingClub performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $17.18

- TIKR Mid-Case Target: ~$37

- Potential Total Return: ~117%

- Annualized IRR: ~18% / year

See analysts’ growth forecasts and price targets for LendingClub stock (It’s free!) >>>

The mid-case model projects around 19% revenue CAGR through 2031, driven by two factors. First, origination volume growth toward management’s medium-term target of $20 billion annually, supported by new verticals and expanding marketing channels. Second, deposit-led net interest income growth, with deposits already at $10.2 billion and growing 14% year-over-year. The margin driver is operating leverage from AI automation scaling across the business as the rebrand investment costs roll off. The primary risk is rate sensitivity: a sustained higher-rate environment compresses loan sale margins and pushes the stock toward the low-case scenario, which still targets around $56 per share by 12/31/31. The high-case scenario, which assumes stronger home improvement adoption and accelerated deposit growth, points to around $100 per share by the same date.

Conclusion

The metric to watch at Q2 2026 earnings in late July is originations. Management guided $3.0 to $3.1 billion. If LC delivers above the top of that range while holding EPS within the $0.40 to $0.45 guidance despite the higher benchmark rate environment, it confirms the rate headwind is already priced in. LendingClub is a digital bank with record profitability, superior credit discipline, and multiple growth catalysts trading at a material discount to its peers. The gap between a 9.4x earnings multiple and what that combination is actually worth is the investment thesis in one sentence.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in LendingClub?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LendingClub, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track LendingClub alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze LendingClub on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!