Key Stats

- Current price: ~$337

- Q1 2026 revenue: $1.474B, up 19% YoY

- Q1 2026 non-GAAP EPS: $1.96

- Q1 2026 non-GAAP operating margin: 44.7%

- Record backlog: $8B

- 2026 full-year revenue guidance: $6.125B to $6.225B (approximately 17% YoY growth)

- 2026 full-year non-GAAP EPS guidance: $7.85 to $7.95

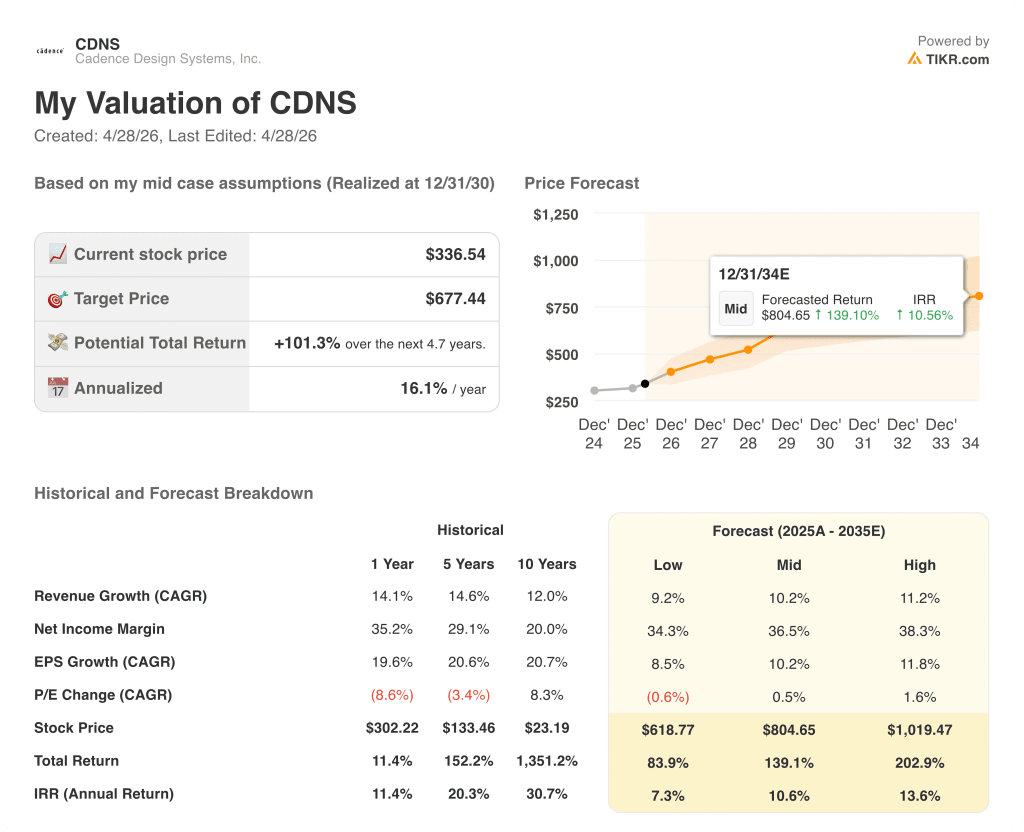

- TIKR model price target: $677 (mid case, realized 12/31/30)

- Implied upside: approximately 101% from current price

Cadence Design Systems Q1 2026 Earnings Breakdown

Cadence Design Systems stock (CDNS) delivered $1.474B in Q1 2026 revenue, up 19% year over year, with non-GAAP EPS of $1.96 and a record backlog of $8B that management described as ahead of plan.

All three business segments contributed to the beat.

Core EDA grew 18% year over year, driven by expanding proliferation at market-shaping customers and what CEO Anirudh Devgan described on the Q1 2026 earnings call as the best hardware emulation quarter in company history, led by AI and HPC customers.

IP revenue grew 22% year over year, according to Devgan on the Q1 2026 earnings call, driven by accelerating demand across AI, HPC, and automotive workloads, with a record-sized IP deal closed at a leading global foundry tied to 2-nanometer node work and expanded content.

System Design and Analysis grew 18% year over year, with strong momentum in 3D-IC and multiphysics simulation as AI-driven system complexity continues to rise.

The quarter also marked a significant product milestone.

Cadence introduced AgentStack, ViraStack, and InnoStack at CadenceLIVE Silicon Valley, extending its agentic AI platform across RTL, analog, and digital implementation, with a new Google Cloud collaboration layering Gemini reasoning into the ChipStack AI Super Agent.

The Hexagon Design and Engineering acquisition, which closed earlier in the year, contributed approximately $20M of revenue in Q1 and diluted EPS by roughly $0.01, according to CFO John Wall on the Q1 2026 earnings call.

Management raised full-year 2026 revenue guidance to $6.125B to $6.225B (approximately 17% growth), up $65M at the midpoint on an organic basis, and raised non-GAAP EPS guidance to $7.85 to $7.95, up $0.08 organically after absorbing $0.28 in Hexagon dilution.

Q2 2026 guidance calls for revenue of $1.555B to $1.595B and non-GAAP EPS of $2.02 to $2.08.

Cadence repurchased $200M in shares during the quarter and guided to approximately 50% of free cash flow allocated to buybacks for the full year.

Cadence Design Systems Stock: What the Financials Show

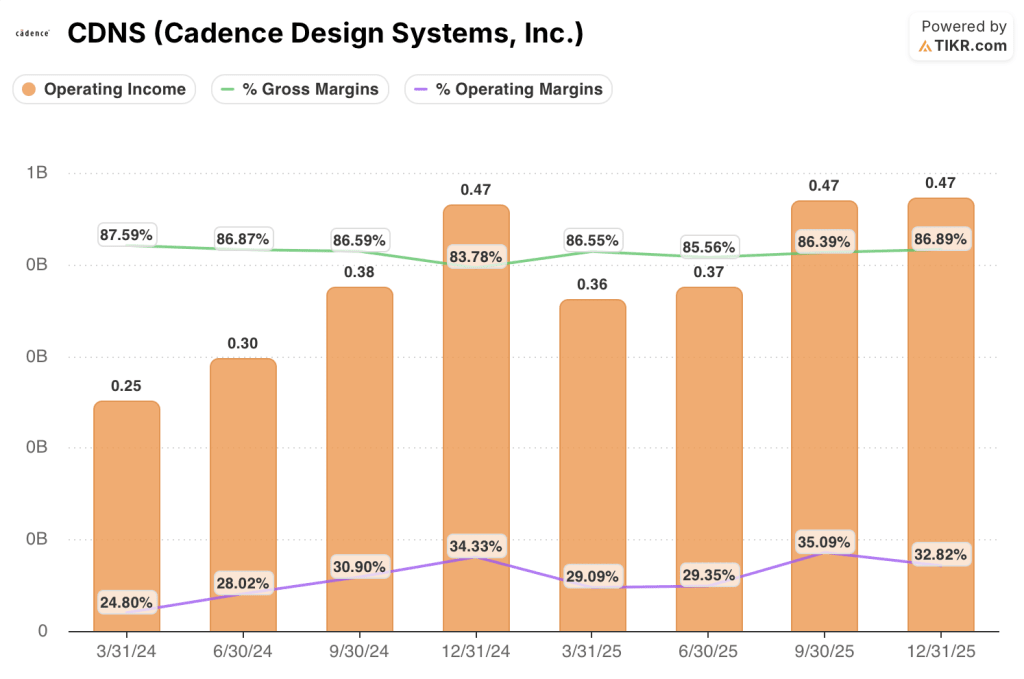

The income statement shows a business rebuilding operating leverage after a soft early 2024, with gross margins holding steady and operating margins recovering sharply into the back half of 2024 and sustaining through 2025.

Gross margins tracked between 83.8% and 87.6% across the eight quarters ending December 2025, with the December 2025 quarter settling at 86.9%, in line with the 86.5% recorded in the March 2025 quarter.

Operating income grew from $250M in March 2024 to $470M by September 2025, with the December 2025 quarter also posting $470M at a 32.8% GAAP operating margin.

Operating margin expanded from 24.8% in March 2024 to a peak of 35.1% in September 2025 before moderating to 32.8% in December 2025, a compression of approximately 2 percentage points quarter over quarter.

That moderation reflects a step-up in R&D and SG&A spending, with R&D expenses rising from $380M in March 2024 to $460M by December 2025 as Cadence invested in its agentic AI platform buildout.

Wall confirmed on the Q1 2026 earnings call that Q1 2026 non-GAAP operating margin reached 44.7%, a meaningfully higher figure than the GAAP margins in the historical screenshot, reflecting the scale of non-GAAP adjustments including stock-based compensation and acquisition-related costs.

The revenue trajectory from the screenshot shows consistent sequential acceleration through late 2024, with the March 2024 quarter at $1.01B, September 2024 at $1.22B, and December 2024 at $1.36B, before a reset to $1.24B in March 2025 and a steady rebuild to $1.44B by December 2025.

Valuation Model Take

The TIKR model prices Cadence Design Systems stock at $677 in the mid case, realized at December 31, 2030, implying approximately 101% upside from the current price of approximately $337.

The mid-case assumptions require a 10.2% revenue CAGR from 2025 through 2035 and a 36.5% net income margin, both achievable given that the business delivered 14% revenue growth over the past year and 35.2% net income margins.

The Q1 2026 report strengthens the investment case on two fronts: the organic guidance raise confirms that the underlying demand environment is accelerating beyond what management assumed in February, and the record $8B backlog provides visibility that was not priced into the February guide.

The Hexagon dilution is a near-term drag but a finite one, with Wall explicitly guiding to accretion in 2027 following the BETA acquisition playbook, which delivered sharp margin improvement one year after close.

Cadence Design Systems stock is not cheap on a current-year basis, but the valuation model suggests the market is not fully pricing in the agentic AI consumption expansion that management described as a new incremental revenue layer on top of the existing subscription base.

The fundamental struggle for Cadence Design Systems stock is whether agentic AI monetization accelerates within the current contract cycle or remains a 2027-and-beyond story.

What Has to Go Right

- Agentic AI tools (ChipStack, ViraStack, InnoStack) drive consumption-based revenue on top of the core EDA subscription base, beginning to show up materially in 2026 bookings and renewals

- IP revenue sustains 20%-plus growth as the record foundry deal at 2-nanometer scales and portfolio expansion into HBM and UCIe captures share at Samsung, Rapidus, and Intel 14A

- Hexagon integration follows the BETA trajectory: dilutive in 2026, accretive in 2027, with the physical AI simulation market adding a meaningful new vertical to total addressable market

- Non-GAAP operating margin holds at 43.5% to 44.5% for the full year as organic incremental margins of approximately 60% absorb the Hexagon cost base over the next 12 months

What Could Still Go Wrong

- Second-half guidance embeds management’s stated conservatism: the implied average quarterly revenue run rate in H2 2026 is below Q2’s $1.555B to $1.595B midpoint, and any macro or export control disruption could make that flat profile a ceiling rather than a floor

- China, at 13% of Q1 revenue, carries year-over-year growth optics that flatter a weak prior-year comparison, and the export control carve-out in guidance is an explicit hedge against a risk management cannot price

- Hexagon’s first-half-weighted revenue profile creates H2 lumpiness that management acknowledged on the Q1 2026 call, adding execution risk to an integration year where margins are already compressed to the 5% to 10% range for the acquired business

- Agentic AI monetization on a usage or consumption basis remains undisclosed in the financial model: Wall confirmed it is not assumed in the 2026 guide, meaning any delay in commercial adoption has no offset in current numbers

Should You Invest in Cadence Design Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CDNS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cadence Design Systems, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CDNS stock on TIKR for Free →