Key Stats

- Current Price: ~$335

- Q1 2026 Revenue: $1.15B, up 3.5% YoY

- Q1 2026 Adjusted EPS: $3.96, down 8.6% YoY

- U.S. Same-Store Sales Growth (Q1): +0.9%

- International Same-Store Sales Growth (Q1): -0.4%

- Full-Year U.S. SSS Guidance (updated): Positive low single digits (prior: ~3%)

- Full-Year International SSS Guidance (updated): Positive low single digits

- Full-Year Global Retail Sales Growth (updated): Mid-single digits

- Full-Year Operating Income Growth (updated): Mid- to high single digits (ex-FX, ex-gains)

- TIKR Model Price Target: ~$554

- Implied Upside Over ~5 Years: ~65%

Domino’s Pizza Stock Misses on EPS as Q1 Comp Disappoints

Domino’s Pizza stock (DPZ) delivered a quarter that fell short on the bottom line, with Q1 2026 adjusted EPS of $3.96, down 8.6% from $4.33 in the prior-year period.

Domino’s Pizza stock has fallen 20% year-to-date, sliding from around $425 in late December to $335 following the Q1 earnings release, with the post-earnings drop representing the sharpest single-day move of that decline.

Revenue came in at $1.15B, up 3.5% year over year from $1.11B in Q1 2025, but the growth masked a meaningful deceleration in same-store sales momentum that rattled investors.

U.S. same-store sales grew just 0.9% in the quarter, driven by a balance of positive order counts and a positive average ticket, according to CFO Sandeep Reddy on the Q1 2026 earnings call.

Carryout comps held up better at +2.4%, while delivery slipped 0.3%, with the divergence attributed to macro pressure on lower-income consumers and competitive promotional activity from national pizza rivals.

CEO Russell Weiner noted on the Q1 2026 earnings call that consumer sentiment reached COVID-level lows in March, intensifying pressure late in the quarter beyond what management had anticipated.

The company added 19 net new U.S. stores in Q1, bringing the domestic system count to more than 7,200, while international net openings totaled 161 stores.

International same-store sales declined 0.4%, but Reddy confirmed on the Q1 2026 earnings call that excluding Domino’s Pizza Enterprises (DPE), the international business met expectations.

On capital returns, Domino’s repurchased approximately 446,000 shares for $170M year-to-date through April 21, and the Board approved an additional $1B repurchase authorization in April, leaving approximately $1.29B remaining on the program.

Management cut its full-year U.S. same-store sales guidance to positive low single digits, down from the prior 3% target, and reduced international SSS guidance to the same range, citing macro and geopolitical uncertainty.

Full-year global retail sales growth is now expected at mid-single digits, with operating income growth (ex-FX, ex-gains) revised to mid- to high single digits.

Weiner was direct about the revision on the call: the internal goal of 3% U.S. same-store sales for the year remains unchanged, and the company is pulling forward unplanned pizza innovation and adjusting its marketing calendar for the second half to close the gap.

Domino’s Pizza Stock: What the Income Statement Shows

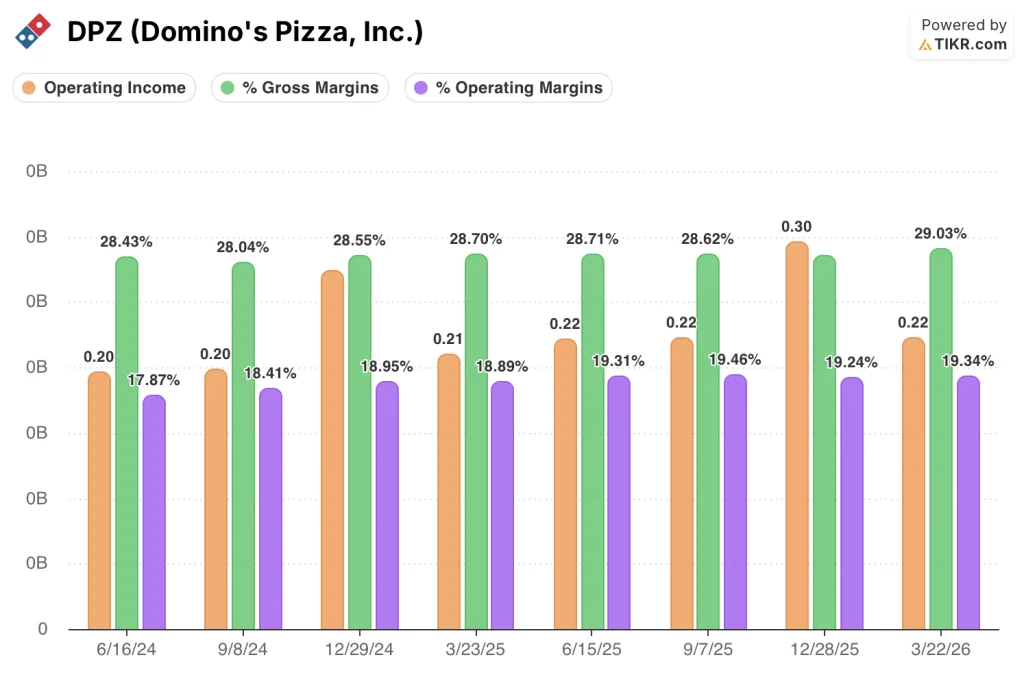

Domino’s Pizza stock enters the post-earnings session with an income statement that tells a story of gradual margin recovery interrupted by a soft Q1 comp.

Gross margin reached 29% in Q1 2026, the highest reading in the eight-quarter window shown, up from 28.7% in the year-ago Q1 2025 period and above the 28.5% recorded in Q4 2025.

Operating margin came in at 19.3% in Q1 2026, flat with the prior-year quarter and consistent with the 19.2% posted in Q4 2025, representing a stable plateau after the 18.9% trough in Q1 2025.

Operating income grew to $220M in Q1 2026 from $210M in Q1 2025, a 5.9% year-over-year increase, consistent with management’s revised full-year operating income growth guidance of mid- to high single digits.

The multi-quarter operating margin trend shows the business has expanded from a low of 17.9% in Q2 2024 to a range of 19% to 20% across the last five quarters, suggesting the operating leverage story remains structurally intact even as comp growth softens.

Reddy noted on the Q1 2026 earnings call that operating margins at the company level are expected to continue expanding in 2026, with supply chain margins also expected to improve on gross profit dollar growth from volume.

TIKR Valuation Model Take

TIKR’s model prices Domino’s Pizza stock at a target of ~$554, implying approximately 65% upside from the current price of ~$335, with full realization modeled by December 2030.

The mid-case assumptions underlying that target are a revenue CAGR of 4.3% through 2035, a net income margin of 13.3%, and EPS growth of 8.4% annually, reflecting moderate expansion from the current 12.4% net income margin and 5.3% one-year EPS CAGR.

The Q1 miss and guidance cut do not structurally alter the model, but they increase execution risk on the revenue growth assumption: the business needs to sustain low-to-mid single-digit comp growth through H2 to stay on the trajectory the mid-case demands.

At ~$335, Domino’s Pizza stock is trading meaningfully below intrinsic value on TIKR’s model, and the risk/reward skews favorably for investors who believe management can close the gap between the revised guidance and the 3% internal comp target in the back half of 2026.

The central tension here is whether the Q1 comp shortfall is a macro-driven pause in a durable share-gain story, or the early signal of a structural ceiling on Domino’s growth algorithm.

What Has to Go Right

- U.S. same-store sales must accelerate from the Q1 0.9% print to sustain positive low single-digit full-year growth; management is pulling forward pizza innovation and adjusting the H2 marketing calendar specifically to close this gap

- Competitor store closures (approximately 450 announced by the two largest public pizza players for 2026) need to translate into tangible traffic and sales transfers for Domino’s franchisees in affected markets

- Carryout market share must continue expanding from the current 20%, well below Domino’s 33% delivery share, as the AI-powered Pizza Tracker and DomOS back-of-house agent drive operational improvements

- Supply chain margin improvement and continued operating leverage must sustain operating income growth at mid- to high single digits even if revenue growth stays closer to the low end of guidance

What Could Still Go Wrong

- Consumer sentiment at COVID-level lows, per management’s Q1 2026 earnings call commentary, could persist into Q2 and Q3, making the acceleration needed from the 0.9% Q1 comp increasingly difficult to achieve

- DPE remains a multi-year drag on international results; despite a new CEO starting in August and active restructuring discussions with DPE leadership, the turnaround timeline is undefined and the risk to international SSS guidance is skewed to the downside

- Competitors matching Domino’s Mix & Match and Best Deal Ever promotions created measurable short-term headwinds in Q1; if rivals sustain this posture longer than management expects, the damage to Domino’s comp could extend beyond a single quarter

- EPS fell 8.6% year over year to $3.96 in Q1 despite revenue growing 3.5%, pointing to cost pressures from labor, food basket, and insurance at company stores that could weigh on reported earnings if comp growth does not recover sharply

Should You Invest in Domino’s Pizza, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DPZ stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Domino’s Pizza, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DPZ stock on TIKR for Free →