Key Stats for SLB Stock

- Current Price: $56.15

- High-Case Target: ~$74

- High-Case Total Return: ~32%

- High-Case IRR: ~3% / year

- Street Target (Mean): ~$57

- Jefferies Price Target: $65 (raised April 25, 2026)

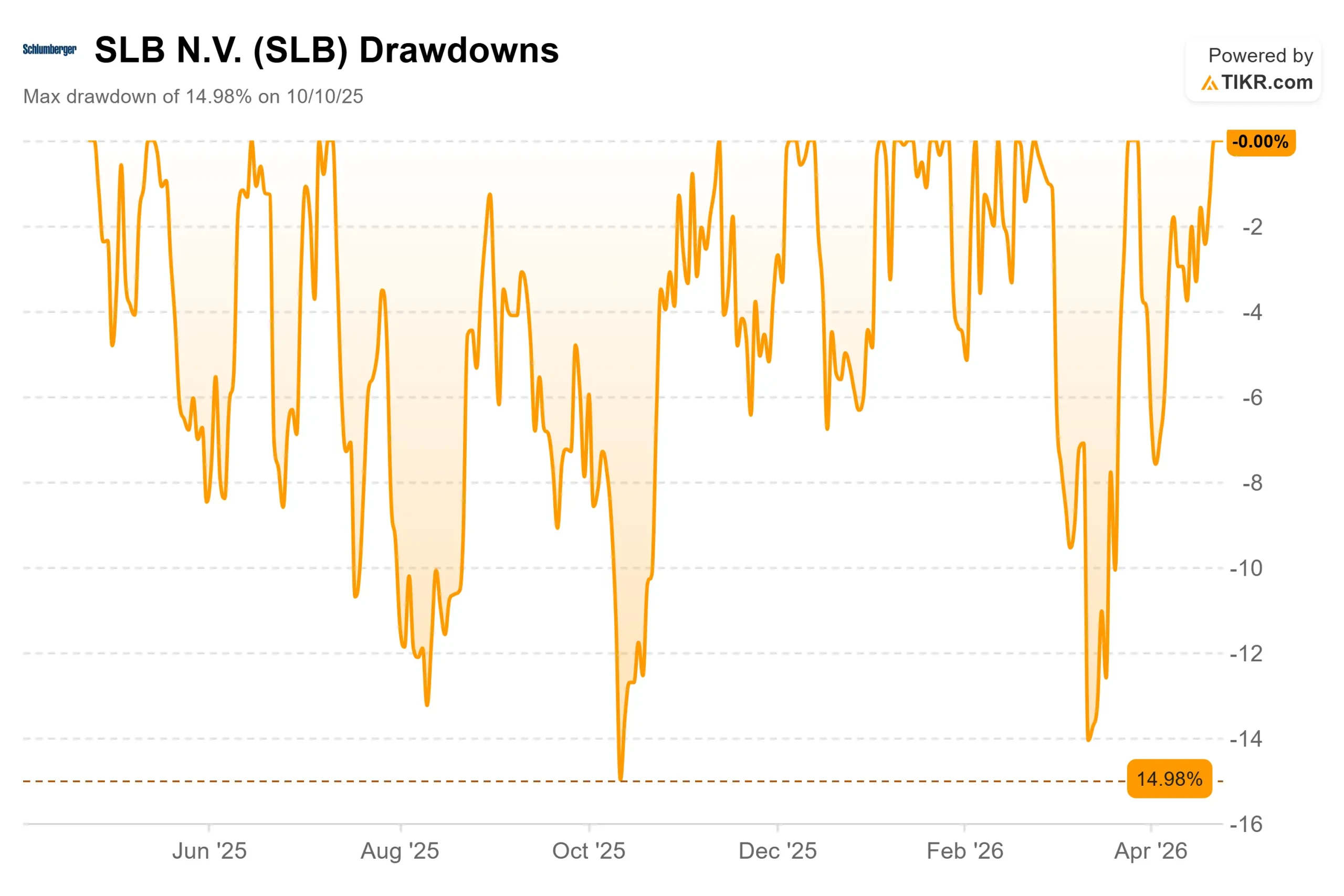

- Max Drawdown: (14.98%) on 10/10/25

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

SLB (SLB) stock opened on April 24 down more than 3% after reporting its weakest quarter in years. By the close, it had fully reversed and finished up 2.6%. That intraday swing tells you what the market decided: the damage was real, but contained.

Bulls argued that the Middle East conflict, which began disrupting SLB’s operations in late February 2026, was a temporary shock rather than a structural break. Bears countered that a company with roughly a third of its revenue tied to the region faced a long recovery, with margins compressing and free cash flow turning negative. The central question heading into earnings was whether Q1 marked the ceiling on the pain.

Q1 2026 revenue of $8.72 billion grew 3% year-on-year, edging past Wall Street’s $8.63 billion estimate. Adjusted EPS of $0.52 edged past the $0.51 consensus, though it fell from $0.72 in Q1 2025. Free cash flow came in at ($23 million), hit by delayed Middle East collections and the first-quarter seasonal working capital build. EBITDA margin compressed to 20.3%, down 346 basis points year-on-year.

“It was a challenging start to the year,” said Olivier Le Peuch, Chief Executive Officer, in the Q1 2026 earnings press release. “Widespread disruptions in the Middle East impacted our business, particularly in Well Construction and Reservoir Performance, where we demobilized operations in several countries to safeguard personnel and assets. Yet we still delivered revenue growth supported by ChampionX and our digital and data center solutions.”

The day after earnings, Jefferies raised its price target on SLB to $65 from $58, keeping a Buy rating, citing a constructive outlook for upstream investment and supply diversification.

See historical and forward estimates for SLB stock (It’s free!) >>>

Is SLB Undervalued Today?

Not at the base case. The TIKR model puts the mid-case target at roughly $56 by 12/31/30, almost exactly where the stock trades today, implying a slightly negative total return at current prices. For the investment to work, the recovery SLB’s management is describing has to materialize.

That recovery case rests on a simple but significant macro shift. Le Peuch told analysts the Middle East conflict has taken more than 500 million barrels of oil production offline since late February, drawn down global inventories, and forced governments to treat energy security as a strategic priority. In his view, oil prices will settle structurally above pre-conflict levels.

“The fragility of the global energy complex we are witnessing today demonstrates the strategic importance and long-term value of oil and gas,” he said on the call.

The most direct beneficiary of SLB is offshore deepwater. OneSubsea (SLB’s joint venture that provides integrated subsea systems and processing equipment for offshore oil fields) grew its backlog 5% year-on-year in Q1. Management expects full-year bookings to visibly exceed last year. Third-party reports cited on the call put the 2026 FID (final investment decision) pipeline more than $100 billion above the prior two-year average, with another step-up expected in 2027.

SLB has already announced subsea awards in Malaysia, the South China Sea, Suriname, and Norway in the weeks surrounding earnings.

SLB is also building two revenue streams that run independently of the oil cycle. Data Center Solutions grew 45% year-on-year in Q1, and management is targeting a $1 billion annual run rate by year-end. On April 23, NVIDIA selected SLB as a modular design partner for its DSX AI factory platform, putting SLB’s manufacturing and supply chain capabilities to work on large-scale AI infrastructure.

That same day, SLB announced it was acquiring S&P Global Energy’s upstream petrotechnical software portfolio and agreed to build joint AI models using SLB’s Lumi platform and Tela agentic AI framework (AI agents that take actions autonomously within industry workflows) applied to S&P’s global upstream datasets.

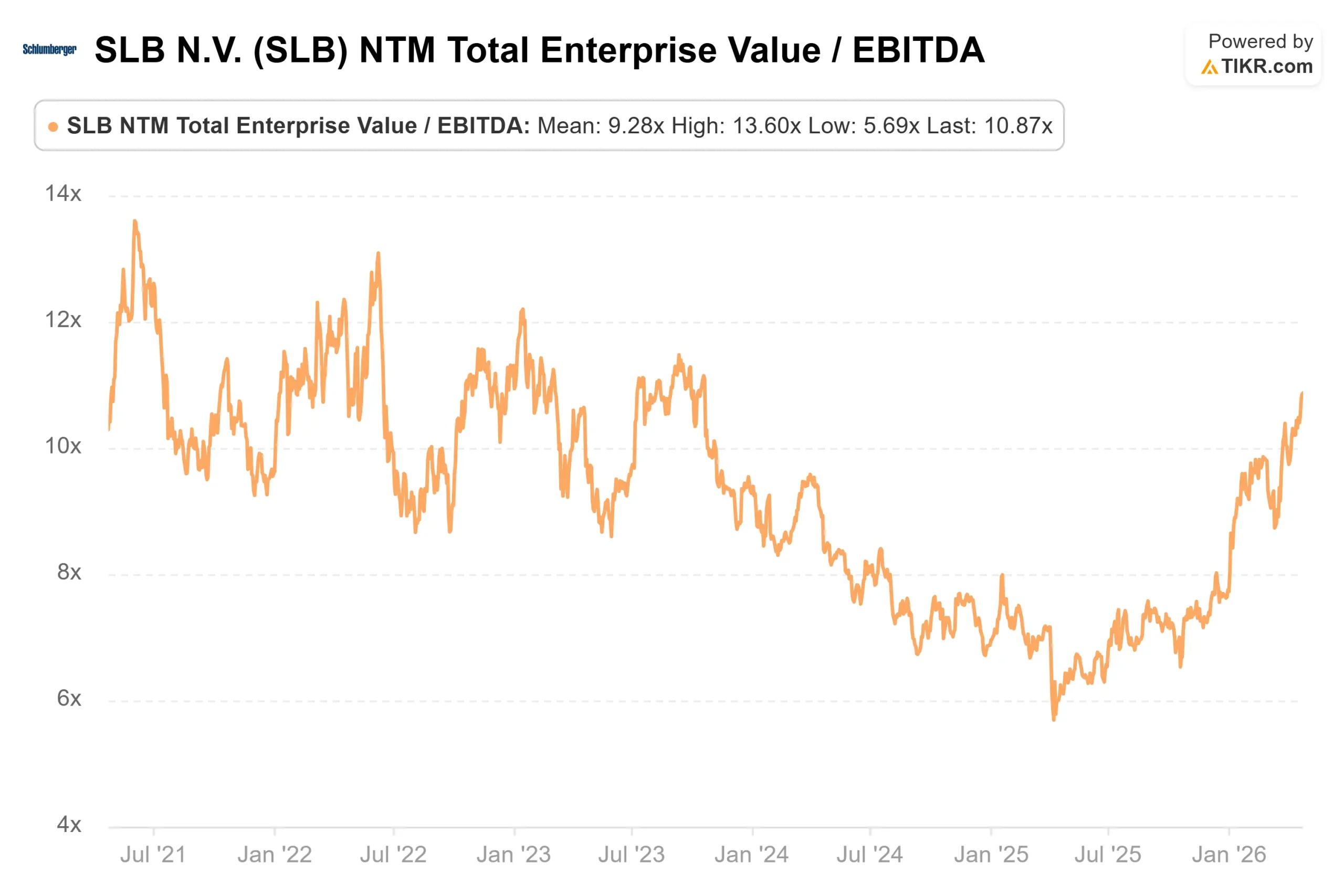

On valuation multiples, SLB trades at 10.77x NTM EV/EBITDA versus Baker Hughes (BKR) at 13.86x, despite SLB’s larger digital and subsea portfolio. The sector median across the TIKR Competitors page is 7.24x, so SLB does carry a premium — but it has narrowed from late-2025 levels, offering a better entry than investors had six months ago.

The risk to this thesis is timing. Free cash flow was negative in Q1. EBITDA margins are at multi-year lows. CFO Stephane Biguet confirmed on the call that even under the middle scenario, where disruptions ease around mid-Q2, the incremental EPS hit in Q2 versus Q1 would be $0.06 to $0.08. Investors who want a clean cash flow picture before buying will find Q2 earnings in mid-July a more comfortable checkpoint.

See how SLB performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $56.15

- Target Price (High Case): ~$74

- Potential Total Return: ~32%

- Annualized IRR: ~3% / year

See analysts’ growth forecasts and price targets for SLB stock (It’s free!) >>>

The TIKR mid case, around 2% annual revenue CAGR and roughly 13% net income margin, targets approximately $56 by 12/31/30, essentially flat from today with a slight negative total return. At current prices, the stock has already priced in the base-case recovery.

The high case, which assumes similar revenue growth but a modest P/E expansion as the mix shifts toward capital-light Digital and Data Center revenue, targets approximately $74 by 12/31/34, roughly 32% total return with an annualized IRR of around 3%. SLB’s $1.20 per share annual dividend adds to that return on top of what the model captures.

Two drivers underpin the high case: offshore deepwater recovery as FIDs accelerate into 2027 and 2028, and Data Center Solutions scaling from a $1 billion run rate to something materially larger in 2027. The margin driver is a return toward the 24-25% EBITDA range SLB delivered in 2023-2024, supported by Middle East recovery, compounding ChampionX synergies, and Digital margins management has committed to holding at or above 35% for the full year.

The primary risk is a conflict that extends deep into the second half of 2026. That would strain the full-year consensus revenue estimate of approximately $36.5 billion, delay the margin recovery, and push the high-case timeline further out.

Conclusion

The metric to watch at Q2 2026 earnings (expected mid-July) is adjusted EBITDA margin. A reading above 21% with early recovery signals in Well Construction or Reservoir Performance would confirm the high-case trajectory. Flat or lower margins mean the thesis needs more time.

SLB kept $451 million in buybacks running through its worst operational quarter in years, announced an NVIDIA partnership and a software acquisition the day before earnings, and still grew revenue 3% year-on-year with one of its largest markets dark. The recovery is not guaranteed. The foundation, however, has not changed.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in SLB?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SLB, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SLB alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!