Key Stats for Costco Stock

- 52-Week Range: $844 to $1,067

- Current Price: $1,011

- Street Mean Target: $1,072

- Street High Target: $1,315

- Analyst Consensus: 19 Buys, 3 Outperforms, 12 Holds, 1 Underperform, 2 Sells

- TIKR Model Target (Aug. 2030): $1,416

What Happened?

Costco Wholesale Corporation (COST) is the world’s third-largest retailer, operating a members-only warehouse model that sells bulk quantities of groceries, consumables, electronics, and premium goods at prices engineered to keep members renewing year after year.

The headline number from fiscal Q2 2026: net sales of $68.24 billion, up 9.1% year over year, with comparable sales rising 7.4% overall and 6.7% after stripping out gasoline price deflation and foreign exchange impacts.

Costco stock continued pressing higher into the quarter, building on a 13.9% year-to-date gain heading into the print, as investors treated the membership-driven model as a reliable defensive anchor through a volatile macro backdrop.

The membership engine itself held firm: 82.1 million total paid members at quarter end, up 4.8% year over year, with executive memberships growing 9.5% to 40.4 million, reflecting members actively upgrading rather than just renewing.

Net income for Q2 came in at $2.035 billion, up nearly 14% from $1.788 billion a year earlier, with diluted EPS of $4.58 versus $4.02 in Q2 2025.

CEO Ron Vachris told analysts on the Q2 2026 earnings call: “At Costco, we always want to be the first to lower prices and the last to raise them,” signaling that the company’s pricing discipline is a strategic commitment, not a reactive response to tariff turbulence.

The tariff picture added a specific catalyst layer: Costco is among more than 2,000 companies that sued the U.S. government to preserve refund rights after the Supreme Court struck down emergency IEEPA tariffs, and Vachris confirmed that if refunds materialize, the company will channel them into lower prices for members rather than absorbing them on the balance sheet.

March net sales followed through at $28.41 billion for the five-week period ending April 5, up 11.3% year over year, with total comparable sales rising 9.4%, including digitally enabled comps up 23.3%.

Costco also raised its quarterly dividend on April 15 from $1.30 to $1.47 per share, bringing the annualized payout to $5.88, a 13% increase that signals management’s confidence in the durability of free cash flow generation.

The company operates 924 warehouses worldwide and has guided for 28 net new openings in fiscal 2026, with a stated target of 30-plus per year over the coming years, including a push into urban markets via creative real estate structures such as parking decks and mixed-use developments.

Wall Street’s Take on COST Stock

The Q2 beat confirmed what the most disciplined Costco bulls have argued for years: the membership flywheel does not stall, and the unit growth pipeline adds a second compounding engine that most mature retailers simply do not have.

COST’s normalized EPS of $18.21 in fiscal 2025 is tracking toward around $20 in fiscal 2026 and around $22 in fiscal 2027, a compounding pace of roughly 13% that remains consistent with the company’s 10-year EPS CAGR of 13%.

Of 37 analysts covering Costco stock, 19 rate it a Buy and 3 an Outperform, giving the stock a combined positive conviction rating from roughly 59% of the coverage universe, while 12 hold and only 3 sit at Underperform or Sell.

The mean price target of $1,072 implies just 6% upside from current levels, with the target range spanning $650 on the low end to $1,315 at the high, a spread that reflects genuine disagreement about whether a near-50x forward P/E multiple is the right long-term anchor or a valuation that requires flawless execution to justify.

Vachris’s explicit commitment that IEEPA tariff refunds will flow to members through lower prices rather than to the income statement is a signal worth weighing: it confirms that Costco’s pricing authority is structural, not opportunistic, and reinforces why the U.S. renewal rate has held at 92.1%.

The one number that would challenge the bull case is the pace of EPS growth deceleration: consensus shows the compounding rate moderating to around 10% by fiscal 2028 and around 7% by fiscal 2029 as the law of large numbers catches up, which compresses the multiple justification if the pipeline does not deliver incremental upside.

The catalyst to watch is the fiscal Q3 2026 earnings report, where investors will look for whether the 30-warehouse-per-year expansion target is tracking on schedule and whether digital comparable sales, currently running at 23.3%, sustain above 20%.

Financials

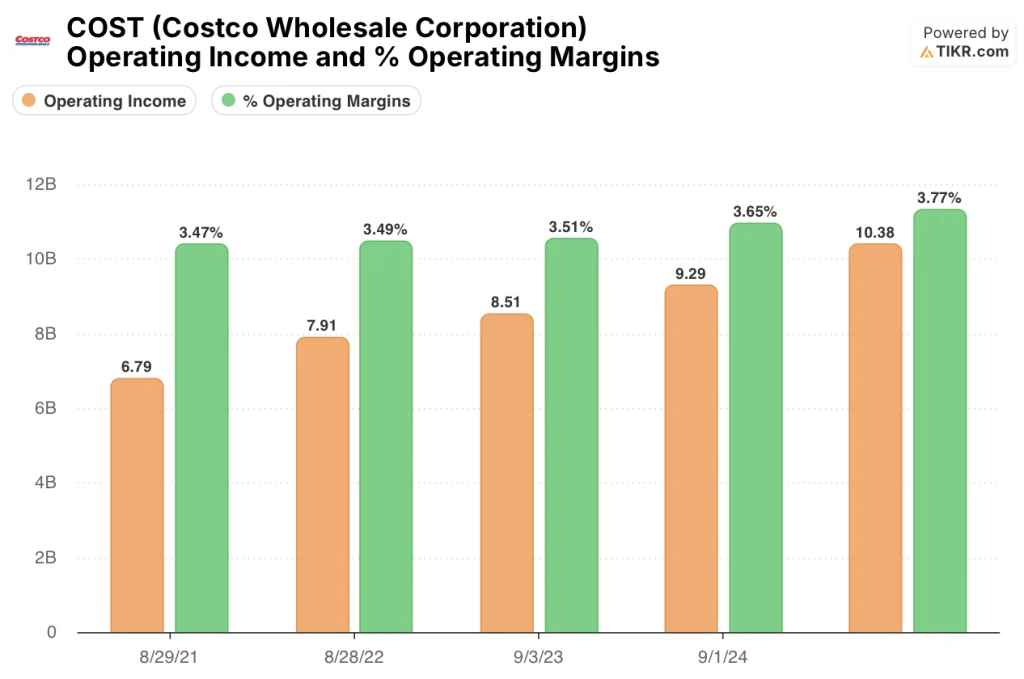

Costco’s operating income reached $10.38 billion in fiscal 2025, up 11.8% year over year, extending a recovery in operating leverage that has pushed operating margins from 3.5% in fiscal 2021 to 3.8% by fiscal 2025.

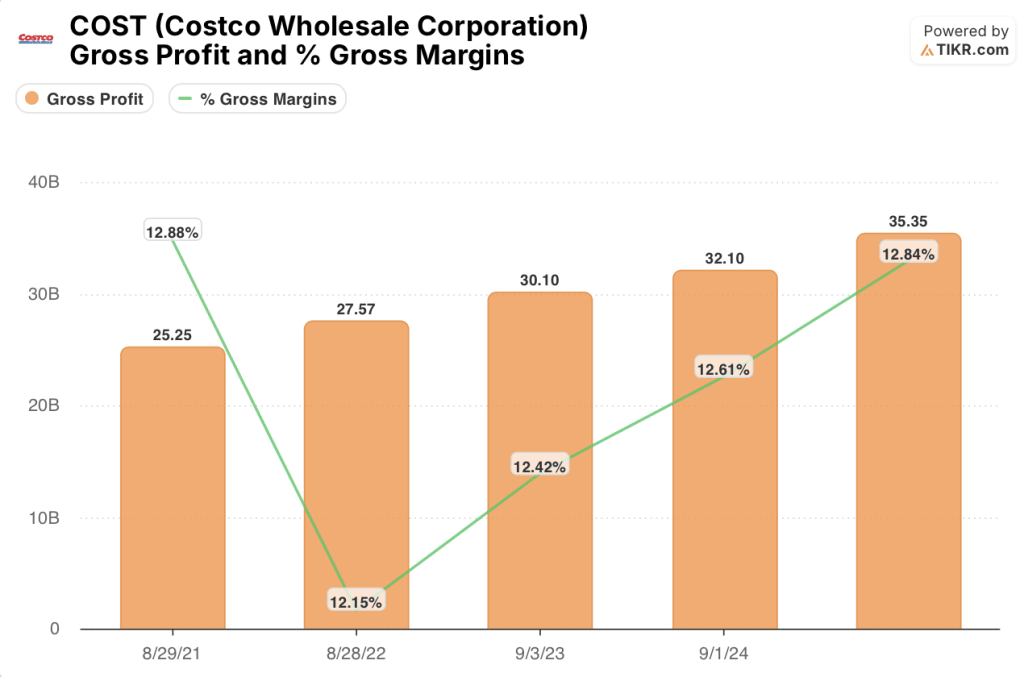

The trajectory is being driven by gross profit growth outpacing cost expansion: gross profit rose 10.1% in fiscal 2025 to $35.35 billion, with gross margins improving to 12.8% from 12.6% the prior year, reflecting a combination of Kirkland Signature penetration, disciplined pricing on commodity deflation, and growing ancillary revenue from pharmacy and food court.

The fiscal 2025 column shows the trend extending further, with operating income at $10.38 billion, operating margins at 3.77%, confirming that the margin expansion from 3.47% in fiscal 2021 has been steady and broad-based rather than driven by any single quarter’s accounting adjustment.

The compression risk to watch is SG&A: total operating expenses grew from $18.45 billion in fiscal 2021 to $26.06 billion in the LTM period, a 41% increase over four years, and CFO Gary Millerchip flagged a Q2 headwind from a reserve increase to cover higher expected costs on prior-year general liability claims, a line item that does not scale with revenue and could create margin drag if it recurs.

What Does the Valuation Model Say?

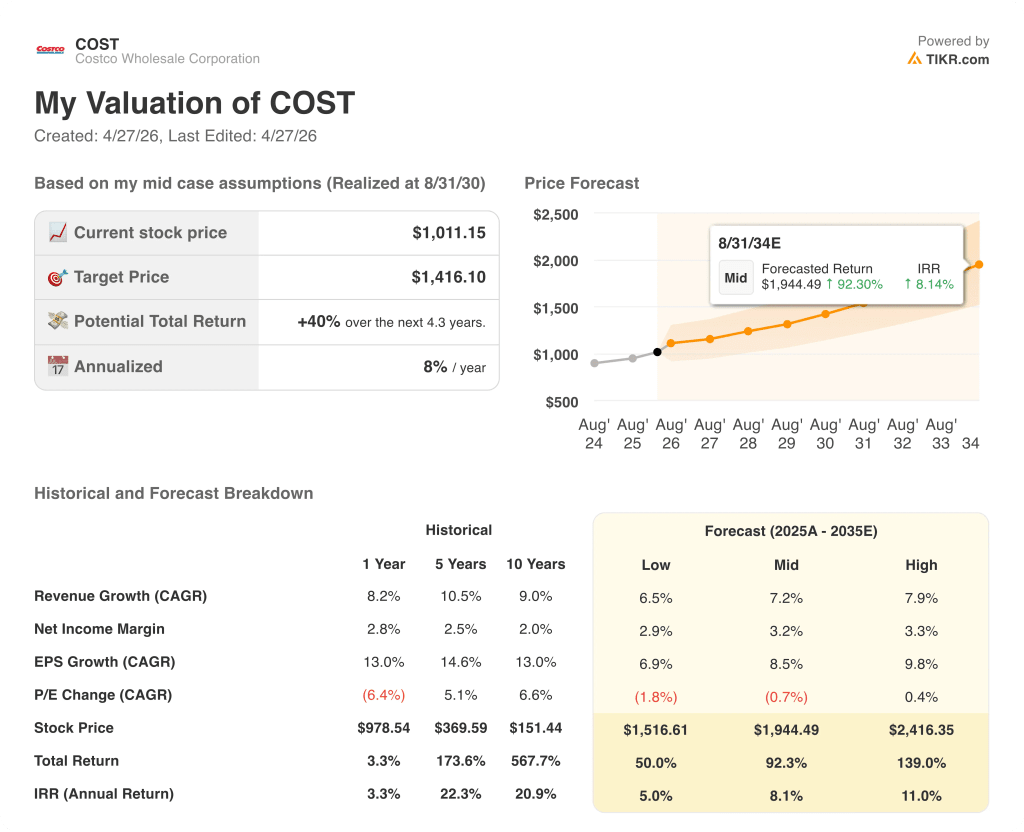

The TIKR model prices COST at $1,416 per share under the mid-case scenario, built on a revenue CAGR of around 7% through fiscal 2030 and net income margin expansion from 2.9% toward around 3.2%, assumptions that are broadly consistent with the pace Costco has already demonstrated over the trailing five years.

At $1,011 against a $1,416 mid-case target, a 40% potential return over ~4 years at an annualized IRR of around 8%, Costco stock is fairly valued: the return profile is reasonable for a business of this quality.

The central tension for Costco stock investors is whether the 30-warehouse-per-year expansion target can sustain double-digit EPS growth long enough to grow into a multiple the market has already assigned at full confidence.

What Has to Go Right

- The 30-warehouse-per-year pipeline executes on schedule, including urban infill openings via parking deck and mixed-use structures in high-density markets like Los Angeles and New York, adding membership spikes that historically accompany new-market entry.

- Digital comparable sales, which ran at 23.3% in March 2026, sustain above 20% as personalization upgrades scale: Q2 already saw $470 million in e-commerce sales attributed to personalized recommendation carousels, and the road map for further rollout is in place.

- EPS compounds at around 13% annually through fiscal 2027, consistent with the 10-year historical CAGR, supported by core-on-core margin improvements of 20-plus basis points per year, a trajectory Q2 demonstrated is achievable even while prices are being lowered for members.

- IEEPA tariff refunds, if they materialize, are channeled into lower prices as Vachris committed, reinforcing the value proposition and supporting membership growth back toward the 5% annualized pace.

What Could Go Wrong

- A forward P/E of roughly 49x leaves almost no room for earnings deceleration: consensus already projects EPS growth moderating to around 10% by fiscal 2028 and around 7% by fiscal 2029, and any quarter that prints below those thresholds could compress the multiple quickly.

- Membership renewal rate erosion continues: the U.S. rate was down 10 basis points in Q2 to 92.1%, driven by online sign-ups renewing at a lower rate than warehouse sign-ups, and a further 20 to 30 basis point decline over the next two to three quarters would signal structural friction in the flywheel that the premium multiple cannot absorb.

- SG&A creep, specifically the general liability reserve increase that added 6 basis points of headwind in Q2, could recur in a higher-cost claims environment, pressuring the operating margin improvement story at the exact moment the valuation requires continued delivery.

- The urban warehouse push into parking deck and mixed-use formats is a model change rather than a replication: Costco has not yet proven at U.S. scale that these structures deliver the same AUV trajectory and membership density as traditional greenfield sites.

Should You Invest in Costco Wholesale Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up COST stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Costco Wholesale Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze COST stock on TIKR for Free →