Key Stats for PayPal Stock

- 52-Week Range: $38 to $80

- Current Price: $50

- Street Mean Target: $53

- Street High Target: $147

- TIKR Model Target (Dec. 2030): $94

What Happened?

PayPal Holdings (PYPL) is one of the world’s largest digital payments companies, operating a two-sided network connecting more than 400 million consumers to tens of millions of merchants across branded checkout, Venmo peer-to-peer payments, buy now pay later, and enterprise payment processing.

The stock collapsed 20.3% on February 3, falling from $52 to $42 after the company reported Q4 2025 adjusted EPS of $1.23, missing the consensus estimate of $1.28, alongside net revenue of $8.68 billion against an estimate of $8.80 billion.

The miss itself was secondary to what management said on the call: branded checkout total payment volume grew just 1% on a currency-neutral basis in Q4, down from 5% in Q3, driven by U.S. retail weakness among lower- and middle-income consumers, international headwinds in Germany, and a deceleration in high-growth verticals including travel, ticketing, crypto, and gaming.

CFO Jamie Miller put it plainly: “While challenges in the macro environment are real, we haven’t executed as well as we need to.”

Branded checkout generates over half of PayPal’s profit dollars, which is what made the simultaneous withdrawal of the company’s 2027 financial targets so damaging — targets set just 12 months earlier at Investor Day that had included 8% to 10% Branded Checkout TPV growth.

The board responded by replacing CEO Alex Chriss with Enrique Lores, formerly of HP, effective March 1, with the stated rationale focused on execution discipline rather than strategic pivot.

Lores walked into a business with genuine bright spots alongside the branded checkout problem: Venmo revenue reached $1.7 billion in 2025, growing approximately 20% year-over-year, with monthly active accounts at 67 million; buy now pay later delivered over $40 billion in TPV, up more than 20% year-over-year; and the Enterprise Payments business returned to double-digit volume growth in Q4 after seven consecutive quarters of profitable expansion.

The new CEO has since hosted a flagship enterprise customer event in San Francisco outlining a strategy centered on AI-driven commerce infrastructure, operational efficiency, and deeper merchant partnerships.

PayPal also signed a multi-year deal in April making it the official peer-to-peer payments partner of the NFL, positioning the PayPal app as the platform for fans to send, split, and pool money across the NFL’s domestic and international ecosystem, with access extended to over 100 million Venmo users in the U.S.

The branded checkout recovery timeline remains uncertain: Miller said at the Wolfe FinTech Forum in March that branded volume was running slightly better than Q4’s 1% in January and February, but declined to call an inflection point, noting the full deployment of the experience, biometrics, presentment, and loyalty flywheel is a “next couple of years” story.

Wall Street’s Take on PYPL Stock

The February collapse forced a reset: what matters now is whether the $400 million in growth investments PayPal is deploying in 2026 across branded checkout, BNPL upstream presentment, and Venmo loyalty represents a temporary EPS drag or a permanent structural cost.

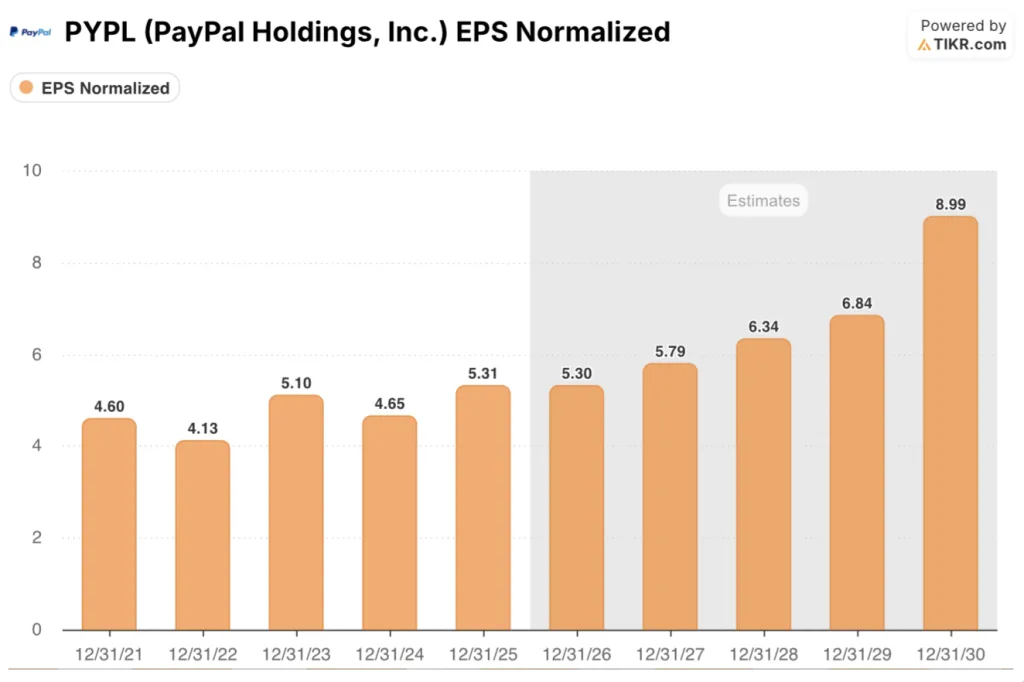

PayPal’s normalized EPS reached $5.31 in 2025, up 14% year-over-year, with consensus estimates pointing to roughly flat growth in 2026 at around $5.30 before recovering to around $5.79 in 2027 and around $6.34 in 2028, as the merchant experience, biometrics, and loyalty flywheel investments begin compounding.

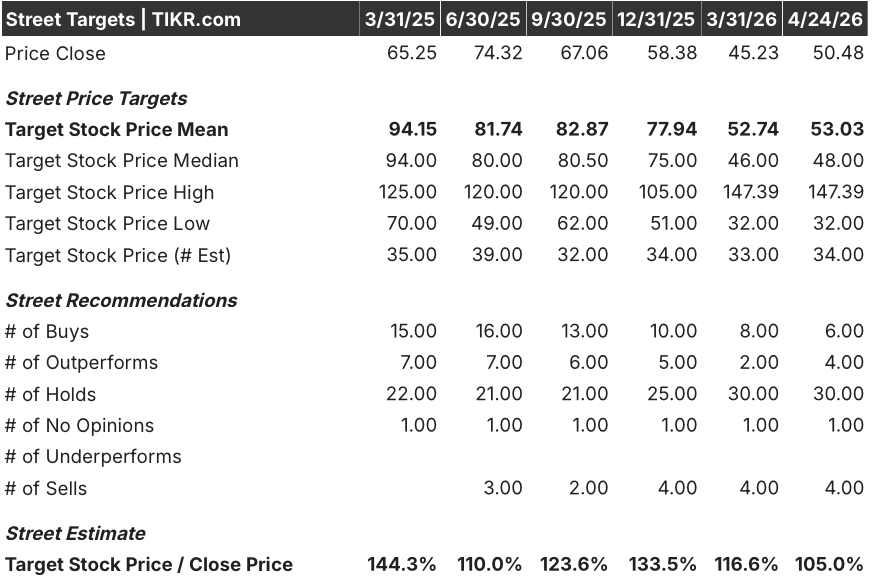

Thirty-four analysts currently cover PYPL: 6 rate it Buy, 4 Outperform, and 30 Hold, with 4 Sell ratings and a mean price target of $53.03, implying barely 5% upside from the current price of $50.48 — a consensus that reflects genuine skepticism about execution rather than a conviction call in either direction.

The target spread captures the real debate: bulls at $147.39 are pricing in a full branded checkout recovery plus accelerating Venmo monetization, while the $32.00 low reflects a view that branded checkout is losing structural share permanently.

Trading at roughly 9.5x forward 2026 consensus EPS of around $5.30, PayPal stock appears undervalued against a company that delivered mid-teens EPS growth in a challenged branded environment and holds $14.8 billion in cash with $6 billion-plus in annual free cash flow supporting ongoing buybacks and a freshly initiated dividend.

Miller’s comment at the Wolfe Forum that branded checkout was running slightly better than Q4’s 1% in January and February is a signal worth tracking: it suggests the worst of the deceleration is behind the business even before the loyalty and presentment investments reach scale.

The core risk is straightforward: if branded checkout volume fails to accelerate through 2026 as the investment spend deploys, the 2027 EPS recovery thesis collapses and the multiple contracts further.

The catalyst to watch is the Q1 2026 earnings call, where management needs to show branded checkout TPV growth trending toward low-single digits and provide evidence that merchant experience upgrades and biometric enrollment are tracking the stated timelines.

What Does the Valuation Model Say?

The TIKR model’s mid-case assumption projects a $94 price target on PayPal stock, representing 85% total return over the next ~5 years at a 14% annualized IRR, driven by approximately 7% revenue CAGR through 2035 and net income margins recovering from 15% in 2025 as the $400 million investment cycle normalizes.

At roughly 9.5x forward 2026 consensus EPS, with over $6 billion in annual free cash flow and Venmo and BNPL growing above 20% even in a challenged year, PYPL stock is undervalued relative to what the underlying business is demonstrating outside of branded checkout.

The question the data cannot yet answer is whether Lores can compress the branded checkout recovery from a “next couple of years” story into something measurable by year-end 2026, because the model’s target price requires the investment cycle to produce compounding EPS growth from 2027 onward.

What Has to Go Right / What Could Go Wrong

PayPal stock is priced near its 52-week floor at roughly 9.5x forward earnings, but the multiple stays at a discount until branded checkout TPV growth demonstrates a durable inflection — the entire argument hinges on whether the execution changes under Lores arrive fast enough to prevent further consensus estimate cuts.

What Has to Go Right

- Branded checkout TPV must reaccelerate from Q4’s 1% toward low-single digits through 2026, with the dedicated merchant teams formed in January targeting the 25% of branded volume at strategic merchants as the first wave

- PayPal Plus, launching in the U.S. and Europe mid-2026, replicates the U.K. early cohort result that showed branded TPV growing mid-single digits year-over-year among enrolled users before marketing was even activated

- Venmo monthly active accounts, already at 67 million and growing 7% year-over-year, convert faster to debit card and Pay with Venmo revenue, pushing Venmo toward $2 billion in revenue ahead of the stated 2026 plan

- BNPL upstream presentment, visible to less than 15% of traffic today, reaches the threshold where the demonstrated 10%-plus branded checkout volume lift begins moving the aggregate number

What Could Go Wrong

- The $400 million investment cycle produces no measurable in-year branded TPV acceleration, forcing a third consecutive year of depressed EPS and erasing the 2027 recovery thesis the current valuation embeds

- Investor lawsuits tied to the withdrawal of 2027 targets, with lead plaintiff deadline set for April 20, create headline overhang and management distraction precisely when execution focus is most critical

- Germany, PayPal’s largest international market, sees branded growth stay negative as local alternative payment methods gain structural share, removing the international recovery leg the model assumes

- Lores, new to the seat as of March 1, requires more time than expected to impose the prioritization discipline the board cited, extending the decision-making lag the CFO acknowledged throughout the earnings call

Should You Invest in PayPal Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PYPL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PayPal Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PYPL stock on TIKR for Free →