Key Stats for Ford Stock

- 52-Week Range: $10 to $15

- Current Price: $12

- Street Mean Target: $14

- Street High Target: $18

- Analyst Consensus: 3 Buys, 3 Outperforms, 15 Holds, 1 Sell

- TIKR Model Target (Dec. 2030): $21

What Happened?

Ford Motor Company (F) is the second-largest U.S. automaker, manufacturing trucks, SUVs, and commercial vehicles across its Ford Blue (gas and hybrid), Ford Pro (commercial fleet), and Ford Model e (electric) segments.

Ford stock has fallen roughly 13% year to date, even as the company’s underlying earnings trajectory points in the opposite direction.

The central headwind is Novelis: fires at the aluminum supplier’s Oswego plant wiped out roughly 100,000 units of F-Series production in 2025, creating a $2 billion drag on adjusted EBIT and forcing Ford to source premium-freight aluminum from South Korea and Europe at a 50% tariff penalty.

That damage is unwinding, but unevenly.

Ford COO Kumar Galhotra told analysts at the Bank of America Securities Auto Summit that the Novelis mill restart is expected between May and September, and that tier-two supply chain visibility has risen to 95%, cutting disruption response time from days to hours.

Q1 2026 U.S. sales fell 8.8% year over year to 457,315 vehicles, with F-Series down 16% as the Novelis recovery plan retimed commercial production into the back half of the year.

The EV story also took a decisive turn in April, when Ford established a new Product Creation and Industrialization organization, merging Doug Field’s advanced technology team with the global industrial team under COO Galhotra.

Field, a Tesla and Apple veteran who joined Ford in 2021, is leaving the company next month after many of his EV programs were canceled, including a $19.5 billion writedown of next-generation EV assets announced in December.

The new organization is designed to accelerate Ford’s product launch cadence: the company targets refreshing 80% of its North American lineup by volume by 2029, led by a mid-size electric pickup off a new Universal Electric Vehicle (UEV) platform arriving in 2027 at an approximately $30,000 price point.

CEO Jim Farley told investors on the Q4 2025 call: “The earnings power of our business is accelerating, and our Ford+ strategy distinguishes us from the competition in clear ways.”

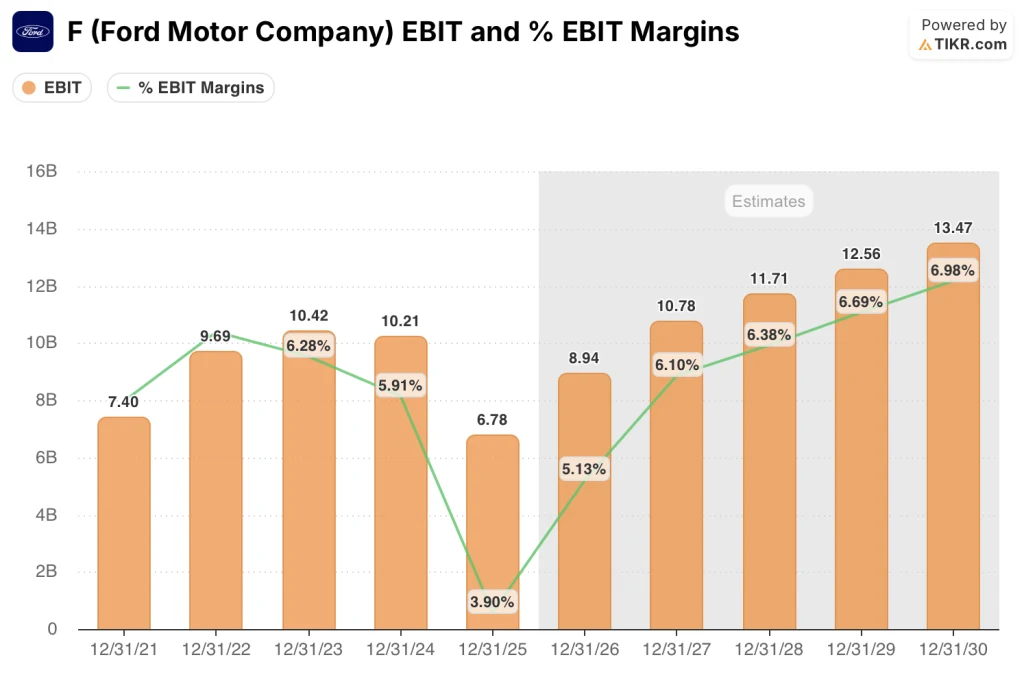

The 2026 guidance frames the recovery concretely: Ford targets full-year adjusted EBIT of $8 billion to $10 billion, up from $6.78 billion in 2025, with the Novelis hot mill restart expected to unlock volume recovery and eliminate roughly $1.5 billion to $2 billion in temporary aluminum sourcing costs in 2027.

Ford Pro, the commercial vehicle segment, is the profit anchor: it generated $6.8 billion of EBIT in 2025 at a double-digit margin, with Super Duty posting its best sales in over 20 years and Transit hitting record U.S. sales.

UBS upgraded Ford stock to “buy” in mid-April, with an analyst citing upside to 2026 and 2027 earnings, a lenient U.S. regulatory environment, and expectations that EBIT lands at the higher end of guidance, with UBS expecting an approximately $0.8 billion EBIT tailwind if the Supreme Court ruling on Trump tariff legality translates into realized savings for Ford

Wall Street’s Take on F Stock

The Novelis-driven volume recovery, concentrated in the second half of 2026, sets up Ford’s EBIT trajectory as a story that has barely started.

F’s adjusted EBIT collapsed 33.6% in 2025 to $6.78 billion as Novelis disruptions and a tariff credit timing issue erased over $3 billion in potential earnings, but consensus now projects around 32% EBIT growth in 2026 to around $8.94 billion, followed by another 21% to around $10.78 billion in 2027, with EBIT margins expanding from 3.9% in 2025 to over 6% by 2027, all before the UEV platform begins contributing volume.

Twenty analysts cover Ford stock currently, with 3 buys, 3 outperforms, 15 holds, and 1 sell, and a mean price target of $13.85, implying roughly 12% upside from current levels, with consensus waiting specifically for Q1 2026 results on April 29 to confirm that the Novelis recovery is tracking to the second-half-weighted plan.

The high-target analyst at $18 is pricing in full execution on the 8% EBIT margin roadmap and UEV platform profitability, while the low-target analyst at $10 assumes tariff escalation permanently impairs the F-Series economics that underpin roughly two-thirds of Ford Pro’s EBIT.

The real signal is not the UBS upgrade but the guidance structure itself: Farley framed the full-year outlook as “back half weighted,” meaning Q1 and Q2 will look depressed by design, and the actual earnings test comes in July.

If aluminum tariffs on imported hot band persist past the Novelis restart window, the $1.5 billion to $2 billion in temporary sourcing costs could extend into 2027, compressing the margin recovery timeline.

The Q1 2026 earnings call on April 29 is the first concrete checkpoint: watch whether adjusted EBIT guidance holds at $8 billion to $10 billion after a quarter that management itself described as “roughly flat sequentially.”

What Does the Valuation Model Say?

The TIKR model’s mid-case target of around $21 per share (66% total return, around 11% annualized) is built on a revenue CAGR of around 2% through 2030, net income margins recovering to around 5%, and EPS growing at around 9% annually, a conservative set of assumptions that does not require Ford to hit its 8% EBIT margin target or generate meaningful UEV platform revenue.

At $12 with the TIKR model flagging a mid-case target of around $21 and even the low-case scenario implying around 73% total return, Ford stock appears to be undervalued by a margin the current consensus (built around near-term Novelis noise) has materially understated.

The central tension in the Ford investment case is whether the industrial recovery is genuinely self-funding or whether it depends on a narrow window of regulatory and tariff conditions that the Trump administration could close.

What Has to Go Right

- The Novelis hot mill restarts between May and September as guided, eliminating $1.5 billion to $2 billion in temporary aluminum sourcing costs in 2027 and unlocking the 50,000 to 60,000 unit volume recovery baked into 2026 guidance

- Ford Pro sustains double-digit EBIT margins with Super Duty and Transit holding dominant positions; 2026 Pro EBIT guidance of $6.5 billion to $7.5 billion implies the segment remains larger than Ford Blue and Ford Model e combined

- The UEV platform, launching in 2027 at around $30,000 per unit, achieves breakeven economics without federal EV subsidies, validating Farley’s CATL-partnership cost model and the company’s $19.5 billion write-off decision as strategically correct in retrospect

- The approximately $0.8 billion tariff credit benefit UBS expects materializes — the ruling has been issued but the cash recovery timeline remains uncertain

What Could Go Wrong

- The Novelis restart slips past September or a third fire extends premium-freight aluminum cost into 2027, adding hundreds of millions in unplanned cost and pushing back the margin recovery timeline by a full year

- Tariff escalation on aluminum and auto parts, combined with continued denial of relief (the White House rebuffed earlier requests as of April 8), structurally impairs F-Series economics, the product family that accounts for the majority of Ford Blue’s EBIT

- Consumer affordability pressure deepens: Q1 2026 U.S. industry sales fell 5.3%, F-Series volume was down 16%, and Cox Automotive forecast a 6.5% full-year industry sales decline, all before April 29 earnings tests the guidance range

- Proxy advisor ISS recommended in April that shareholders vote against the re-election of Executive Chairman William Clay Ford Jr. and director William Kennard, adding governance headline risk ahead of the May 14 annual meeting

Should You Invest in Ford Motor Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up F stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ford Motor Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze F stock on TIKR for Free →