Key Stats for Rambus Stock

- Current Price: $141.31

- Target Price (Mid): ~$258

- Street Target: ~$122

- Potential Total Return: ~83%

- Annualized IRR: ~14% / year

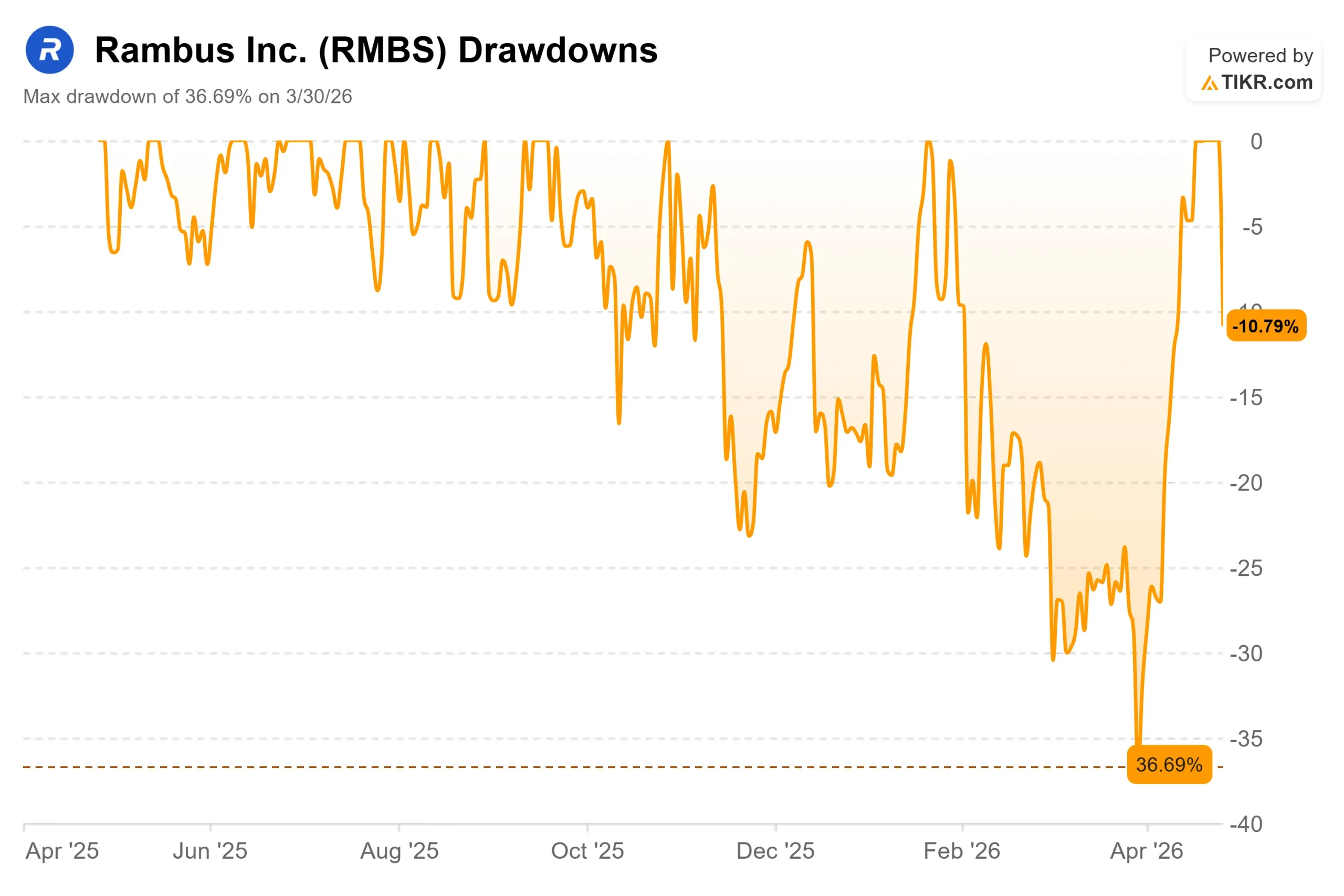

- Earnings Reaction: -10.79% (April 27, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Rambus (RMBS) nearly doubled from a closing low of $79.73 on March 30 to a peak of $158.40 on April 24, driven by AI momentum and the launch of a new server memory chipset. Then Q1 2026 earnings landed on April 27, and the stock fell 10.79% on the day despite results that came in line with guidance.

That reaction captures the central tension in RMBS right now. Bulls point to a business positioned across the entire AI memory stack, with three revenue streams, a $786 million cash balance, and a product roadmap that keeps expanding. Bears argue the stock ran far ahead of both fundamentals and Street consensus, and results that merely meet guidance can no longer justify the valuation.

“The growth of AI inference and agentic workloads in the data center continues to drive demand for higher memory bandwidth, efficient data movement, and scalable connectivity,” said Luc Seraphin, President and CEO of Rambus, in the company’s official earnings release.

That framing maps directly to why, even after a 10% drop, the structural AI case for RMBS has not changed.

See historical and forward estimates for Rambus stock (It’s free!) >>>

Is Rambus Undervalued Today?

Q1 numbers were stronger than the post-earnings reaction implied. Revenue came in at $180.2 million, up 8.1% year-over-year. Product revenue hit $88 million, up 15% year-over-year, driven by DDR5 RCDs (registering clock drivers, which manage signal integrity in high-speed memory modules). Free cash flow for the quarter was $66.3 million. Management guided Q2 revenue to $192–$198 million, with product revenue of $95–$101 million, an 11% sequential increase at the midpoint.

The valuation is where the debate lives. RMBS trades at around 35x NTM EV/EBITDA per the TIKR Competitors page, which sits at a meaningful premium even within AI semiconductors. Broadcom trades at around 25x on the same basis, NVIDIA at around 21x, and Marvell Technology at around 36x. Rambus commands a premium over most of its peers, which requires the growth story to stay intact.

Seraphin pointed to agentic AI, meaning persistent, multistep reasoning that runs continuously rather than in short bursts, as a direct driver for standard DDR memory demand. That matters because it expands Rambus’s market beyond the GPU-centric narrative. He also noted the ratio of CPUs to GPUs in AI servers is shifting toward CPUs as inference workloads scale, which directly increases demand for DDR5 RCDs.

“The move to AI inference and the move to agentic AI will change the ratio in favor of CPUs,” Seraphin said on the call, “and that’s good for us.” Rambus exited 2025 with a mid-40% market share in DDR5 RCDs, with no signs of erosion heading into 2026.

The risk is timing. Back-end semiconductor assembly capacity remains tight, a constraint Seraphin said is expected to persist into 2027. More importantly, the MRDIMM opportunity (multiplexed registered DIMMs, a higher-capacity, higher-bandwidth upgrade to standard DDR5) carries a roughly $600 million addressable market. Still, the ramp depends on Intel and AMD platform launch timing. Seraphin was explicit: the bulk of that revenue arrives in 2027, not 2026.

See how Rambus performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $141.31

- Target Price (Mid): ~$258

- Potential Total Return: ~83%

- Annualized IRR: ~14% / year

See analysts’ growth forecasts and price targets for Rambus stock (It’s free!) >>>

The TIKR mid-case model targets ~$258 by 12/31/30, implying a total return of roughly 83% and a revenue CAGR of around 14% per year. The two primary revenue drivers are DDR5 product volume growth through the Gen 3 platform transition and the eventual MRDIMM ramp, and silicon IP expansion, which management projects at 10–15% annually as hyperscalers design custom AI chips that require Rambus’s interconnect and security IP. The model’s mid-case assumes net income margins of around 40%, consistent with the business mix trending toward higher-margin IP revenue over the forecast period.

The primary risk is the timing of platform launches at Intel and AMD, which Rambus does not control. A delay in next-generation CPU platforms pushes the MRDIMM ramp later and compresses near-term product revenue growth.

Street analysts carry a mean target of ~$122, below where RMBS trades today. That gap reflects a time-horizon difference: Street targets are typically 12-month estimates, while the TIKR model runs through 12/31/30. Investors holding for the MRDIMM ramp are being asked to look past a near-term valuation premium for a payoff the model places several years out.

Conclusion

The metric to watch at Q2 2026 earnings (expected late July) is product revenue. If it clears $100 million, the sequential growth story and back-end supply normalization are both on track. If it falls short, the valuation premium becomes difficult to defend.

Rambus is a structurally sound business at the center of every major AI memory trend. The Q1 selloff was the market pricing out hype, not pricing out the thesis.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Rambus?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Rambus, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Rambus alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!