Key Stats for Sanmina Stock

- Current Price: $188.08

- Street Target (Mean): ~$174

- TIKR Model Target (Mid: ~$249

- Potential Total Return: ~32%

- Annualized IRR: ~7% / year

- Max Drawdown: -32.69% (March 20, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Sanmina Corporation (SANM) entered its April 27 earnings call after rallying roughly 12% the prior week on pre-earnings optimism. What management delivered exceeded even those elevated expectations.

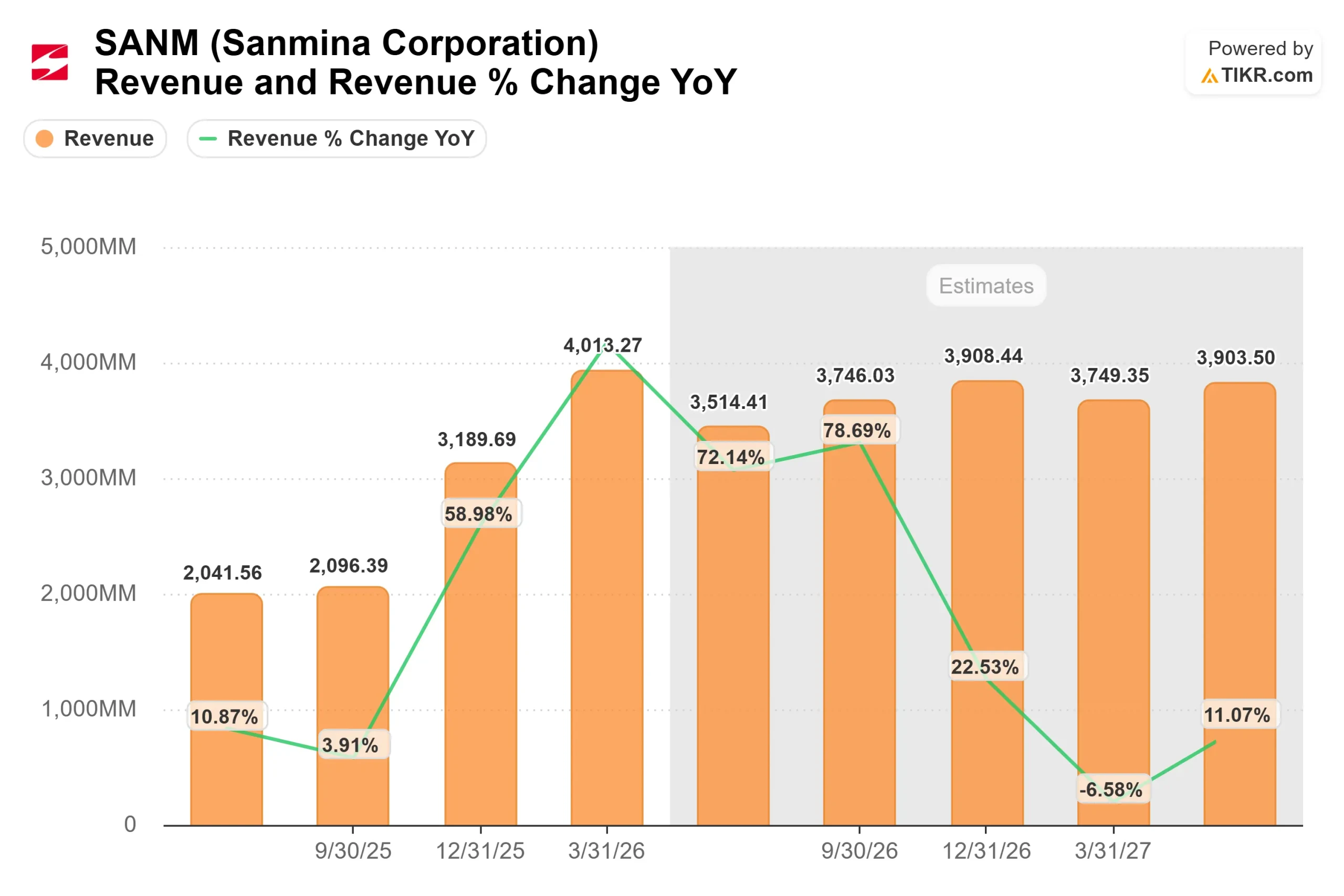

Revenue came in at $4.01 billion for Q2 fiscal 2026, 22.78% above consensus estimates, with non-GAAP diluted EPS of $3.16 representing a 31.80% beat. The stock surged roughly 11% in after-hours trading, according to press reports. The board simultaneously authorized a new $600 million share repurchase program with no expiration date.

The driver was ZT Systems, the data center manufacturing business Sanmina acquired from AMD in October 2025. A hyperscale customer pulled forward significant accelerated compute orders that had been scheduled for the second half of the fiscal year. CFO Jonathan Faust described it as driven by “strong execution and customer demand.”

That pull-forward is why Q2 was so strong and why Q3 revenue guidance of $3.2 billion to $3.5 billion came in below Street expectations. It is a timing shift, not a demand problem.

Chairman and CEO Jure Sola was direct: “Fiscal year ’26 is tracking better than our expectation at the start of the fiscal year.” He and Faust both stated the company is “increasingly confident” in achieving revenue of $16 billion or more in fiscal 2027, with new program wins already secured across multiple hyperscalers and OEM customers.

For context, Sanmina reported $8.1 billion in revenue just one fiscal year ago, per TIKR.

See historical and forward estimates for Sanmina stock (It’s free!) >>>

Is Sanmina Undervalued Today?

At roughly 11x NTM EV/EBITDA per TIKR, Sanmina trades at a meaningful discount to peers. Jabil (JBL) trades at around 14x and Celestica (CLS) at around 29x, the latter reflecting a premium for its higher-margin AI server mix. The gap is real, but so is the reason for it.

JPMorgan initiated coverage at Neutral with a $145 target, citing data center upside from ZT Systems while flagging AMD rack concentration risk. Susquehanna also started at Neutral with a $135 target, calling the risk-reward balanced at current prices. Both targets now sit well below where the stock trades.

The concern is legitimate. Every dollar of ZT Systems accelerated compute revenue in Q2 was tied to AMD-based platforms. Sola confirmed on the call that no NVIDIA product was shipped during the period. Management is actively addressing this: a new next-generation accelerated compute business has already been won with multiple hyperscalers and OEM customers, targeting production readiness around September 2026. Sola’s stated goal is to win every major hyperscaler within 12 to 18 months.

The core Sanmina business provides ballast that the AI narrative tends to obscure. The book-to-bill ratio exceeded 1.1 in Q2, meaning new orders are coming in faster than revenue is being recognized, per management. Communication networks revenue within core Sanmina grew 22% year-over-year, driven by IP switching, 400G and 800G optical pluggables, and early 1.6 terabit shipments. Defense, energy, and semiconductor capital equipment are recovering and expected to accelerate in fiscal 2027 and 2028.

One area to watch: the balance sheet carries around $940 million in net debt per TIKR, and trailing free cash flow is negative as working capital builds to support the ZT ramp. Q2 free cash flow was $342 million, benefiting from favorable timing on the pull-forward shipments. Management was clear that inventory would rebuild in Q3 and Q4 to prepare for next-generation compute platforms. The net debt/EBITDA ratio stands at 1.48x on a trailing basis per TIKR, within management’s stated 1.0x to 2.0x long-term target range.

What stands out positively: management reported a non-GAAP pretax return on invested capital of 34.7% in Q2, up from 23.0% a year ago. At the right scale and mix, the ZT economics are meaningfully better than the company’s thin-margin label suggests.

See how Sanmina performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $188.08

- Mid-Case Target: ~$249

- Potential Total Return: ~32%

- Annualized IRR: ~7% / year

See analysts’ growth forecasts and price targets for Sanmina stock (It’s free!) >>>

The TIKR mid-case model prices SANM at around $249 by 9/30/31, implying roughly 32% total return and an annualized IRR of around 7%. The model assumes a mid-case revenue CAGR of around 16%, with two main drivers: the ZT Systems ramp as hyperscaler production schedules crystallize in fiscal 2027 and 2028, and continued high-single-digit growth in core Sanmina segments. Net income margin is modeled at around 4% in the mid case, consistent with the FY2026 operating margin guidance of 6.3% to 6.6% from management.

The high case prices the stock at around $444, requiring approximately 17% annual revenue growth. That scenario is plausible if next-generation compute platforms launch on schedule and Sanmina captures more value through vertical integration, where profit margins are structurally better than pure system assembly. The low case, at around $251, reflects AMD concentration persisting and working capital requirements proving larger than anticipated, with revenue still growing around 14% annually. Notably, even the low case sits above the current price on the TIKR model.

Conclusion

Watch ZT Systems revenue at the Q3 fiscal 2026 earnings call in late July 2026. If the result lands at or above the guided midpoint of $1.1 billion, it confirms the Q2 pull-forward did not cannibalize demand and that next-generation platform schedules are on track. The result below would raise legitimate questions about whether Q2 was a timing event rather than a trend.

Sanmina is no longer just a contract manufacturer. It is now one of the largest system-integration partners for hyperscale accelerated compute in the world, with a recovering core franchise alongside it and the financial capacity to keep investing in both.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Sanmina?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Sanmina, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Sanmina alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Sanmina on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!