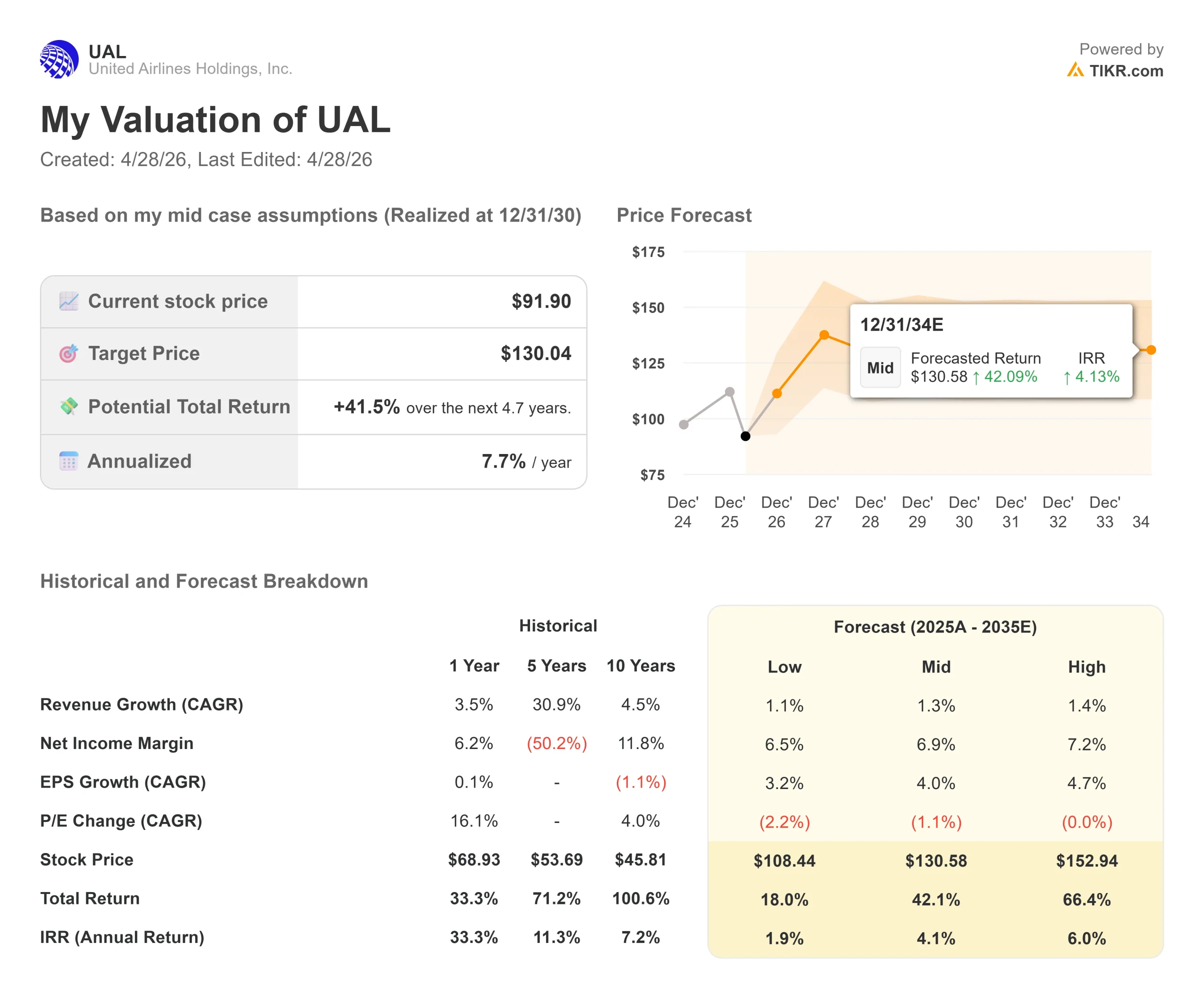

Key Stats for United Airlines Stock

- Current Price: $91.90

- Target Price (Mid): ~$130

- Street Target: ~$130

- Potential Total Return: ~42%

- Annualized IRR: ~8% / year

- Earnings Reaction: -5.58% (April 21, 2026)

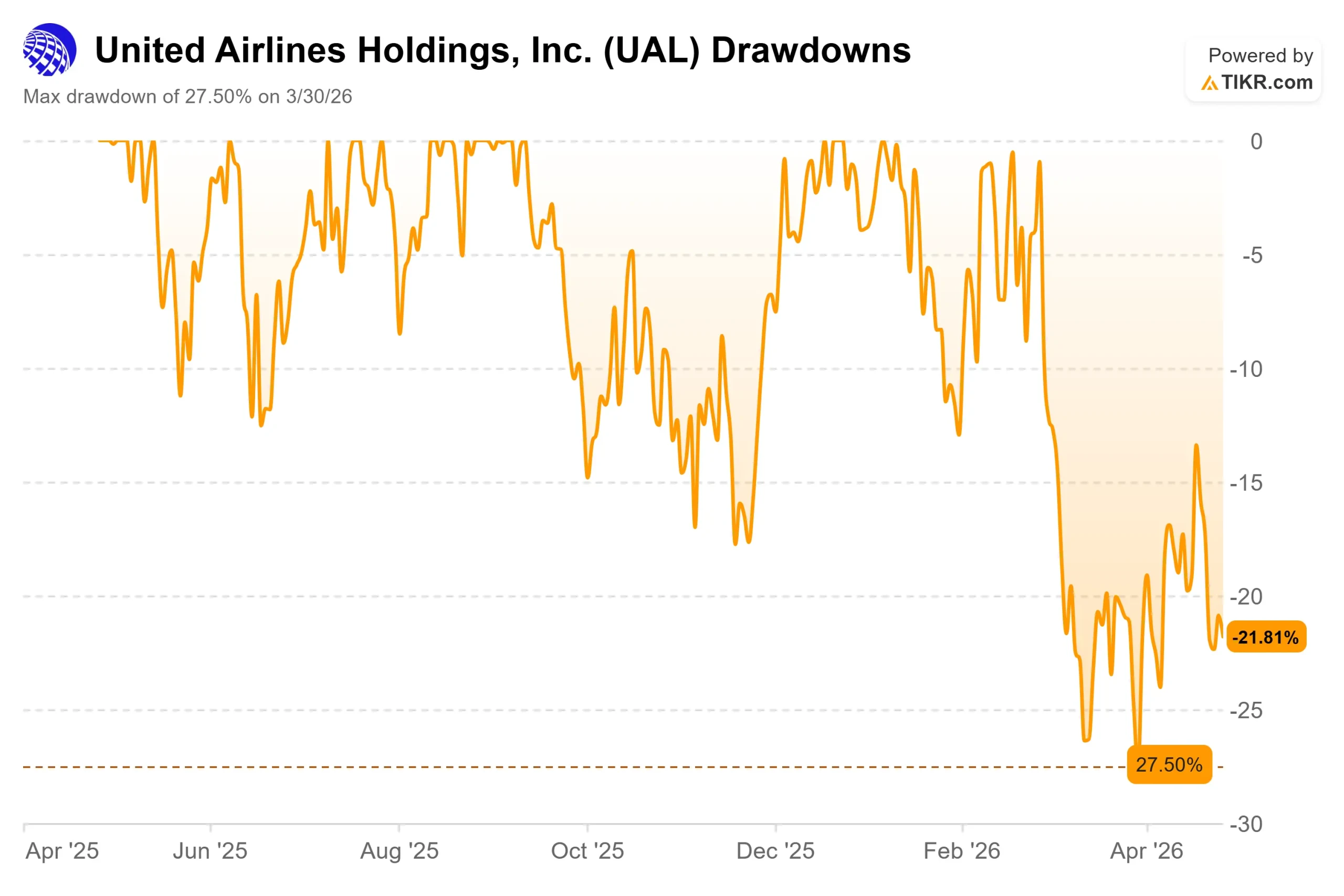

- Max Drawdown: -27.50% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

United Airlines (UAL) stock has had a brutal two weeks, and investors are being pulled in opposite directions. The stock fell 5.58% on April 21 after a Q1 earnings beat came attached to a full-year EPS guidance cut from $12–$14 to $7–$11, driven by jet fuel prices that roughly doubled following the Iran conflict.

Then on April 27, CEO Scott Kirby publicly confirmed he had approached American Airlines about a merger, American had rejected him, and the pursuit was over. The stock dipped another ~1.5%.

Bears see an airline managing a fuel crisis by slashing capacity and widening guidance ranges. Bulls see record revenue, accelerating yields, and three years of deliberate balance sheet work paying off. The unresolved question is whether the fuel shock is temporary cost pressure on a structurally stronger airline, or the beginning of a longer reset.

The merger episode is worth understanding in that context. Kirby stated publicly: “I approached American about exploring a combination because I thought we could do something incredible for customers together,” adding that without a willing partner, “something this big simply can’t get done.” American formally rejected the proposal, with CEO Robert Isom calling it “anticompetitive” and publicly closing the door.

This was not a defensive move. On the Q1 call, Kirby noted United had won roughly 20 points of market share at each of its major hubs and 38 points of market share with business travelers in Chicago. An airline that confident in its domestic standing is not making a distress acquisition. That ambition is the lens through which the valuation question needs to be answered.

See historical and forward estimates for United Airlines stock (It’s free!) >>>

Is United Airlines Undervalued Today?

The fuel shock is real, but the Q1 numbers show a business that is absorbing it without demand cracking. Total revenue hit $14.6 billion, up 10.6% year-over-year and a Q1 record. Premium revenue grew 13.6% on only 4.4% more capacity. Business travel revenue rose 14%. Loyalty revenue grew 13%.

CCO Andrew Nocella confirmed on the call that selling yields reached up 20% year-over-year in the most recent week of April, with business revenue running up 25% in the last two weeks alone.

The $7–$11 full-year EPS guidance range is wide, and that uncertainty is what the market is pricing. But management laid out a specific recovery trajectory: 40–50% of elevated fuel costs recaptured in Q2, 70–80% in Q3, and 85–100% by Q4. That is a testable thesis, not a vague promise. CFO Mike Leskinen guided for a double-digit RASM (revenue per available seat mile) increase in Q2, which will either confirm or challenge the pass-through case when results arrive.

The balance sheet gives United the runway to execute. In Q1, the company paid down more than $3.1 billion in debt and raised $2 billion in unsecured bonds, its first unsecured issuance since 2019, with the 3-year tranche pricing at 4.87%. Leskinen described this as evidence that bond markets see the United States as knocking on the door of investment grade, a credit quality shift that lowers refinancing risk and the cost of capital over time.

At $91.90, the stock trades at 10.19x NTM P/E and 6.12x NTM EV/EBITDA. Those multiples have risen modestly from year-end 2025 levels, not because the stock went up, but because forward earnings estimates fell faster than the share price.

That is a market repricing risk, not awarding a premium. UBS raised its price target to $139 from $135 with a Buy rating on April 24. BMO Capital maintained Outperform and raised its target to $130 from $110 on April 23.

Beyond the near-term fuel recovery, seven commercial initiatives announced in Q1 add a structural revenue layer the current multiple does not reflect. Nocella described the redesigned digital merchandising system called nested selling as worth “hundreds of millions of dollars per year” in incremental upsell revenue per management’s own assessment.

Fifty new A321 Coastliner aircraft with lay-flat Polaris beds are planned for transcontinental routes. MileagePlus program changes are already driving record credit card penetration among elite members. Taken together, Nocella said the goal is not just double-digit margins but “ultimately mid-teen margins.”

See how United Airlines performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $91.90

- Target Price (Mid): ~$130

- Potential Total Return: ~42%

- Annualized IRR: ~8% / year

See analysts’ growth forecasts and price targets for United Airlines stock (It’s free!) >>>

The TIKR mid-case model targets around $130 by 12/31/30. The two revenue drivers are a revenue CAGR of around 1%, reflecting conservative expectations for a mature network carrier, and around 4% annual EPS growth from margin recovery and debt reduction. The net income margin assumption of around 7% reflects the ongoing premium and loyalty revenue mix shift Nocella described on the call. The ~8% annualized IRR is amplified by share count reduction through buybacks over the forecast period.

The upside: fuel normalizes, United delivers 85–100% cost recovery by Q4, and 2027 pretax margins hit the double-digit target. The stock re-rates toward the Street high near $139. The downside: fuel stays near $4.30 per gallon into 2027, demand destruction materializes, and EPS settles near the $7 floor.

Conclusion

The Q2 result, expected around July 15, is the next real test. Watch RASM. Management guided for a double-digit increase. If actual RASM meets or beats that with premium demand intact, the pass-through thesis is confirmed. If RASM disappoints, the $7 EPS floor becomes the working assumption and the valuation reset deepens.

The failed merger is a footnote. United is trading at 10x forward earnings after posting record Q1 revenue, actively passing fuel costs through to customers with yields up 20% year-over-year, and holding its highest credit rating in nearly three decades. The market wants proof that the fuel recovery holds. Q2 will provide it or not.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in United Airlines?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up United Airlines, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track United Airlines alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze United Airlines on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!