Key Stats for Thermo Fisher Stock

- Current Price: $468.04

- Street Target (Mean): ~$621

- TIKR Mid-Case Target: ~$707

- Potential Total Return (Mid): ~51%

- Annualized IRR (Mid): ~9% / year

- Max Drawdown: -27.38% (March 13, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Thermo Fisher Scientific (TMO) is sitting roughly 27% below its 52-week high of $643.99, and even a quarter that beat on both revenue and adjusted EPS wasn’t enough to stop the bleeding on April 23. Shares fell more than 7.5% intraday as investors weighed stronger-than-expected quarterly profit against muted underlying growth before recovering to close up 0.64%.

The tension is straightforward. Bulls see one of the world’s most durable life sciences franchises at a meaningful discount to its own history, with biopharma tailwinds accelerating and a reshoring wave not yet in the numbers. Bears point to 1% organic revenue growth, $43.2 billion in total debt after the $8.875 billion Clario acquisition, and a second-half ramp that still needs to be proven.

The question the market is focused on: is the organic growth weakness structural, or is Q1 a setup for recovery?

Much of the Q1 top-line growth was driven by acquisitions, contributing 3 percentage points, while organic growth remained modest at just 1%. That landed below even the muted 1.2% consensus estimate, and the stock sold off despite management raising full-year revenue guidance to $47.3 billion to $48.1 billion from $46.3 billion to $47.2 billion.

Management had a clear explanation. On the call, Marc Casper, Chairman and Chief Executive Officer, noted that Q1 organic growth was dragged by one fewer selling day versus the prior year and by revenue timing in the pharma services business, each costing roughly 1 percentage point. Strip those out, and Q1 was tracking at approximately 3% organic growth, exactly where management guided for Q2. The optics were worse than the underlying business.

Then on April 27, Thermo Fisher announced it had agreed to divest its microbiology division to Astorg for approximately $1.075 billion. The microbiology unit reported revenues of $645 million in 2025 and provides solutions for antimicrobial susceptibility testing and culture media for clinical, pharmaceutical, and food safety testing.

The sale, expected to close in the second half of 2026, will dilute adjusted EPS by $0.15 in the first full year. This is portfolio sharpening: shedding a lower-margin diagnostics unit to concentrate resources on higher-growth biopharma services and clinical research.

See historical and forward estimates for Thermo Fisher stock (It’s free!) >>>

Is Thermo Fisher Undervalued Today?

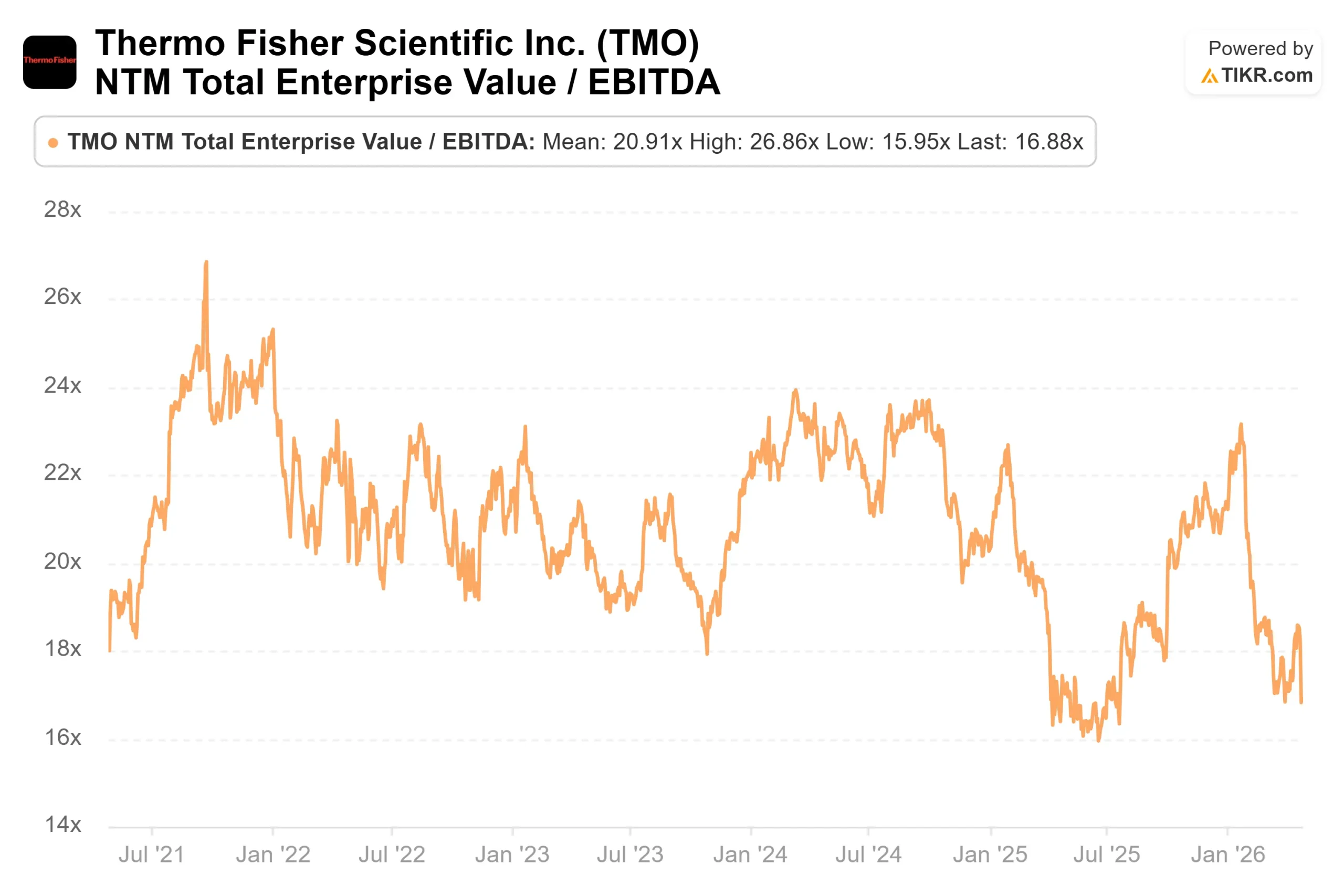

At $468.04, TMO trades at 16.88x NTM EV/EBITDA, well below the 18x to 22x range it commanded from 2021 through early 2024. The Street’s mean price target sits at around $621, implying roughly 33% upside. Analysts who trimmed targets after Q1, including Stifel (to $600) and Robert W. Baird (to $639), held their buy ratings. The consensus is adjusting the timeline, not the thesis.

The free cash flow picture supports that view. Full-year 2026 FCF is guided at $6.9 billion to $7.4 billion, and LTM FCF already sits at around $5.5 billion. A business generating that level of cash has a significant structural floor, regardless of near-term organic growth fluctuations.

What the market seems to be discounting is how much is building below the headline numbers. Bioproduction, which supplies the raw materials and equipment for manufacturing protein-based drugs and cell therapies, delivered strong organic growth for the second straight quarter. Clinical research, operating under the PPD brand, grew both revenue and authorizations year-over-year.

Casper said the clinical research business showed “nice step-up in organic growth” sequentially, with revenue and authorizations both moving in the right direction, supported by a growing pipeline of uncommitted opportunities.

Clario adds depth to this advantage. Clario captures digital endpoint data from patients during clinical trials, allowing pharma customers to run more efficient drug development studies. The acquisition contributed $30 million in Q1 revenue and $0.32 of adjusted EPS accretion net of financing costs for the full year. Based on the original acquisition announcement, management expects approximately $175 million in adjusted operating income from synergies by year five.

Reshoring is the longer-dated catalyst. Multiple pharma customers have already signed contracts for Thermo Fisher’s U.S. drug product manufacturing facilities. Casper stated that reshoring revenue is “largely a ’27 and ’28 activity,” but contracts are already in place, giving unusually clear visibility on growth two years out.

The risks matter too. Leverage sits at 3.5x net debt-to-EBITDA with $43.2 billion in total debt. The academic and government end market remains soft in both the U.S. and China, which together constrained the Analytical Instruments segment, where organic revenue fell 2% and margins compressed 250 basis points in Q1. Management also inserted a placeholder into guidance for potential supply chain inflation it cannot yet fully quantify.

For context on valuation multiples, Waters Corporation (WAT) trades at around 15x NTM EV/EBITDA and Mettler-Toledo (MTD) at around 21x. Thermo Fisher’s 16.88x sits in the middle despite having a significantly larger scale and a faster-growing biopharma services business than either. The discount to MTD looks difficult to justify on fundamentals, suggesting the market is pricing in near-term execution risk rather than long-term business quality.

See how Thermo Fisher performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $468.04

- TIKR Mid-Case Target: ~$707

- Potential Total Return (Mid): ~51%

- Annualized IRR (Mid): ~9% / year

See analysts’ growth forecasts and price targets for Thermo Fisher stock (It’s free!) >>>

The TIKR mid-case model targets around $707 per share by December 31, 2030, using a mid-case revenue CAGR of around 5% and a net income margin expanding toward around 21%. The two revenue drivers are bioproduction volume growth and clinical research contracts converting to revenue through 2027 and 2028. The margin driver is operating leverage through the PPI Business System, combined with Clario synergies, building over time.

The upside case reaches around $1,051 by 12/31/30, implying roughly 124% total return, if revenue growth holds near 5% and margins expand toward around 22%. The downside case still lands at around $693, implying roughly 48% total return even with revenue growth of around 4% and margins near 20%. The key risk to the model is a slower organic recovery than management’s guidance implies, particularly if supply chain inflation proves harder to mitigate and academic and government demand stays depressed.

Conclusion

Watch organic revenue growth at the Q2 2026 call, expected in late July. Management guided for approximately 3% organic growth. If that number lands at or above 3%, the Q1 weakness was calendar noise, the recovery thesis holds, and the current NTM EV/EBITDA discount becomes increasingly difficult to justify. The May 20 Analyst Day is the next near-term event to watch.

Thermo Fisher is a market-leading life sciences platform trading at a cyclical discount, with biopharma tailwinds building and reshoring revenue not yet reflected in the price.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Thermo Fisher?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Thermo Fisher, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Thermo Fisher alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Thermo Fisher on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!