Key Stats for Union Pacific Stock

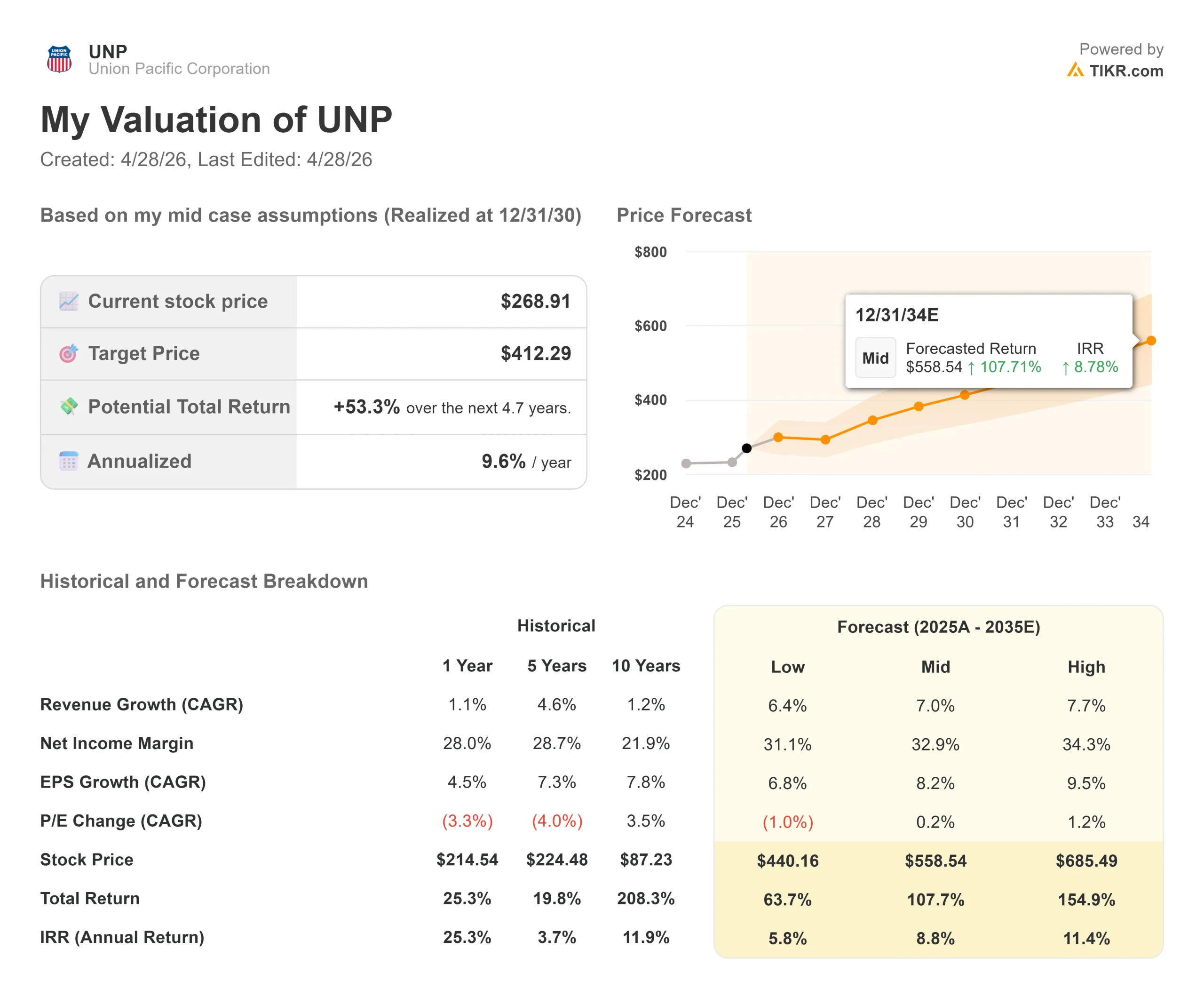

- Current Price: $268.91

- Street Target (Mean): ~$289

- TIKR Model Target (Mid): ~$412

- Potential Total Return: ~53%

- Annualized IRR: ~10% / year

- Q1 2026 Earnings Reaction: -0.94% (April 23, 2026)

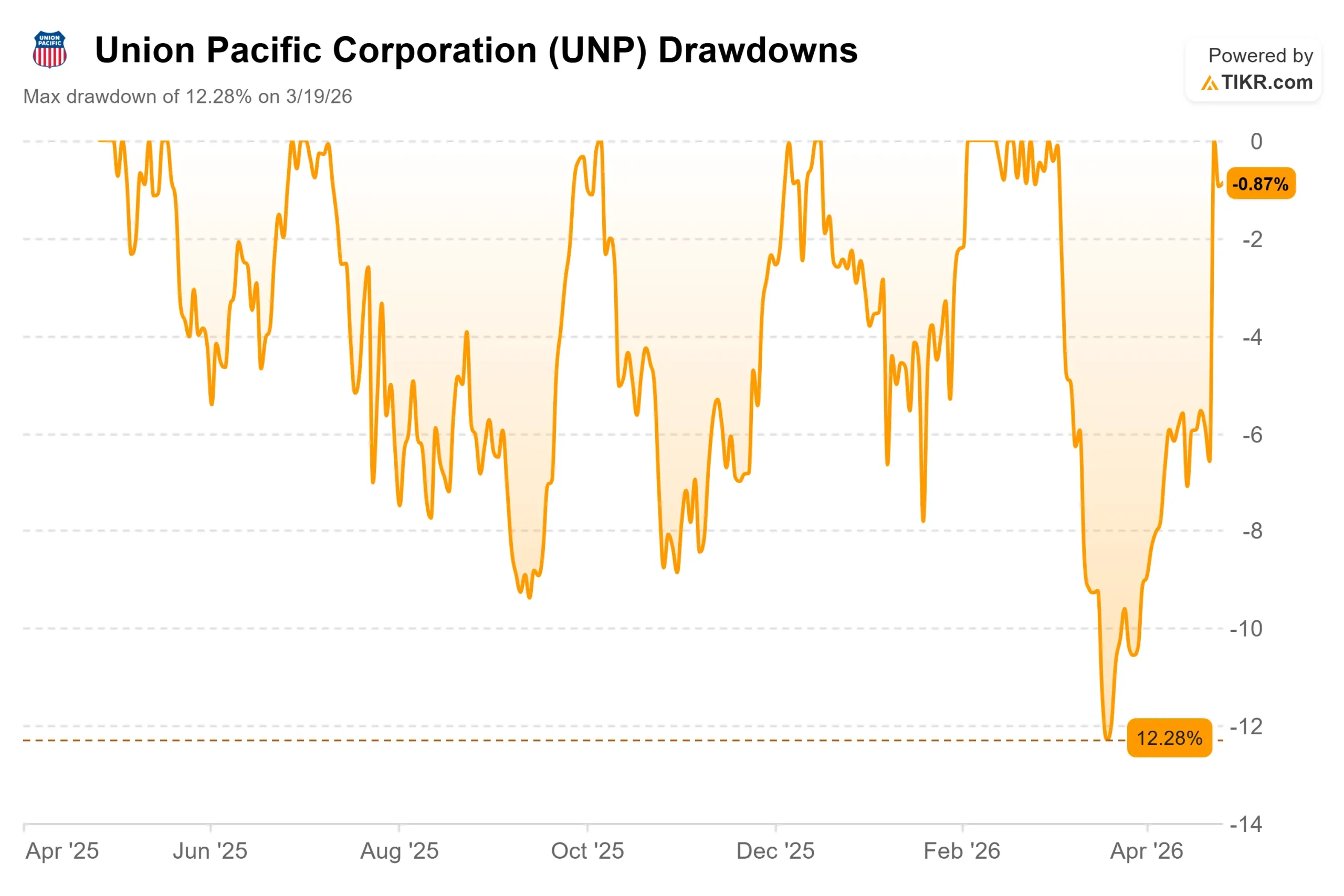

- Max Drawdown: 12.28% (March 19, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Union Pacific (UNP) reported record first-quarter results on April 23, and the stock barely moved. Adjusted EPS of $2.93 beat consensus by around 2%, management reaffirmed full-year guidance, and operational records were set across six key metrics. The muted reaction tells you what the market is actually focused on: not execution, but whether the proposed merger with Norfolk Southern will survive regulatory review.

That question gets its biggest data point yet on April 30, when Union Pacific files its revised merger application with the Surface Transportation Board (the STB, the federal agency that regulates railroad combinations).

The STB rejected the original application in January 2026 as procedurally incomplete. Wednesday’s refiling restarts the regulatory clock toward a Q2 2027 approval target that management has publicly committed to.

CEO Jim Vena addressed the stakes directly on the earnings call. “We are more convicted now than we ever have been when you take a look at what’s in the merger application and all the detail that we’re putting forward,” he said.

That conviction is being backed by action: in early April, Union Pacific reached an agreement with the American Train Dispatchers Association guaranteeing union jobs for life after the merger closes, removing one of the main opposition arguments ahead of the filing.

The overhang has a specific dollar value. If the STB rejects the deal outright, Union Pacific owes Norfolk Southern a $2.5 billion reverse termination fee, per the terms of the merger agreement.

See historical and forward estimates for Union Pacific stock (It’s free!) >>>

Is Union Pacific Undervalued Today?

The standalone railroad is already performing at record levels. In Q1 2026, Union Pacific grew freight revenue 4%, improved its adjusted operating ratio (the portion of each revenue dollar going to costs) by 80 basis points to 59.9%, and grew cash from operations 10% to $2.4 billion.

CFO Jennifer Hamann confirmed that pricing dollars exceeded inflation dollars in the quarter, which is the core of the efficiency story: the railroad is generating real pricing power even as volume growth stays modest.

The TIKR data support further improvement ahead. Consensus has revenue growing from $24.5 billion in 2025 to around $26 billion in 2026 and $27 billion in 2027, with a forward two-year EPS CAGR of around 8%. At roughly 21x next twelve months earnings, the stock reflects a quality compounder but prices in almost none of the merger upside.

The merger upside is structural. The proposed combination with Norfolk Southern would eliminate the Mississippi River interchange, the point where freight currently transfers between eastern and western carriers, adding time and cost to every cross-country shipment. A single-line coast-to-coast route removes those friction points entirely.

Management has cited approximately $2.75 billion in targeted annual synergies from the combined network, based on the merger application filed with the STB. EVP Kenny Rocker noted on the earnings call that 520 customers, 700 commercial partners, and 2,000 stakeholders have signed letters of support, representing the commercial pipeline already waiting for that product.

The risks are real. Fuel costs are running above $4 per gallon in April, up from management’s original $2.35 estimate, which Hamann said will pressure Q2 margins. International intermodal volumes fell 28% in Q1 on West Coast import shifts.

The STB is also evaluating this deal under its 2001 merger rules, which require a combination to actively enhance competition rather than merely maintain it, a standard never applied to a transaction of this scale. The spread between the analyst’s mean target of around $289 and the TIKR mid-case of around $412 maps directly onto that uncertainty.

See how Union Pacific performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $268.91

- TIKR Model Target (Mid): ~$412

- Potential Total Return: ~53%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Union Pacific stock (It’s free!) >>>

The mid-case uses a revenue CAGR of around 7% through 2030. Two drivers from the Q1 transcript support that assumption. First, EVP Kenny Rocker closed 20 new construction projects in Q1 alone, with a strong pipeline heading into Q2 tied to LNG terminal and data center construction. Second, domestic intermodal posted its third consecutive record quarter, built on truck-to-rail conversions where rail pricing remains well below trucking rates, keeping that conversion opportunity wide open.

The net income margin expansion toward around 33% is driven by operating leverage. As Vena explained on the call, Union Pacific is moving higher volumes today than in 2019 while running 24% fewer trains. Additional revenue flows to the bottom line with minimal incremental cost because the network’s fixed-cost structure is largely already in place.

If the STB approves the merger on schedule in Q2 2027, synergies add meaningfully to these projections. If the deal fails, Union Pacific absorbs the $2.5 billion termination fee and resumes buybacks, with a standalone business projected to generate over $6 billion in annual free cash flow by 2026, according to estimates. Either way, the core railroad is not broken. The April 30 filing determines whether the merger call option is worth pricing in.

Conclusion

Watch for STB acceptance of the April 30 application. If the Board accepts it as complete, the formal review clock starts, and Q2 2027 approval becomes a live target. If it is rejected again, the timeline extends, and merger risk rises materially. Union Pacific’s standalone railroad is running at record efficiency regardless of how that plays out. The real question for investors is whether the gap between the Street’s ~$289 target and the TIKR mid-case of ~$412 represents a discount the April 30 filing begins to close.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Union Pacific?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Union Pacific, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Union Pacific alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Union Pacific on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!