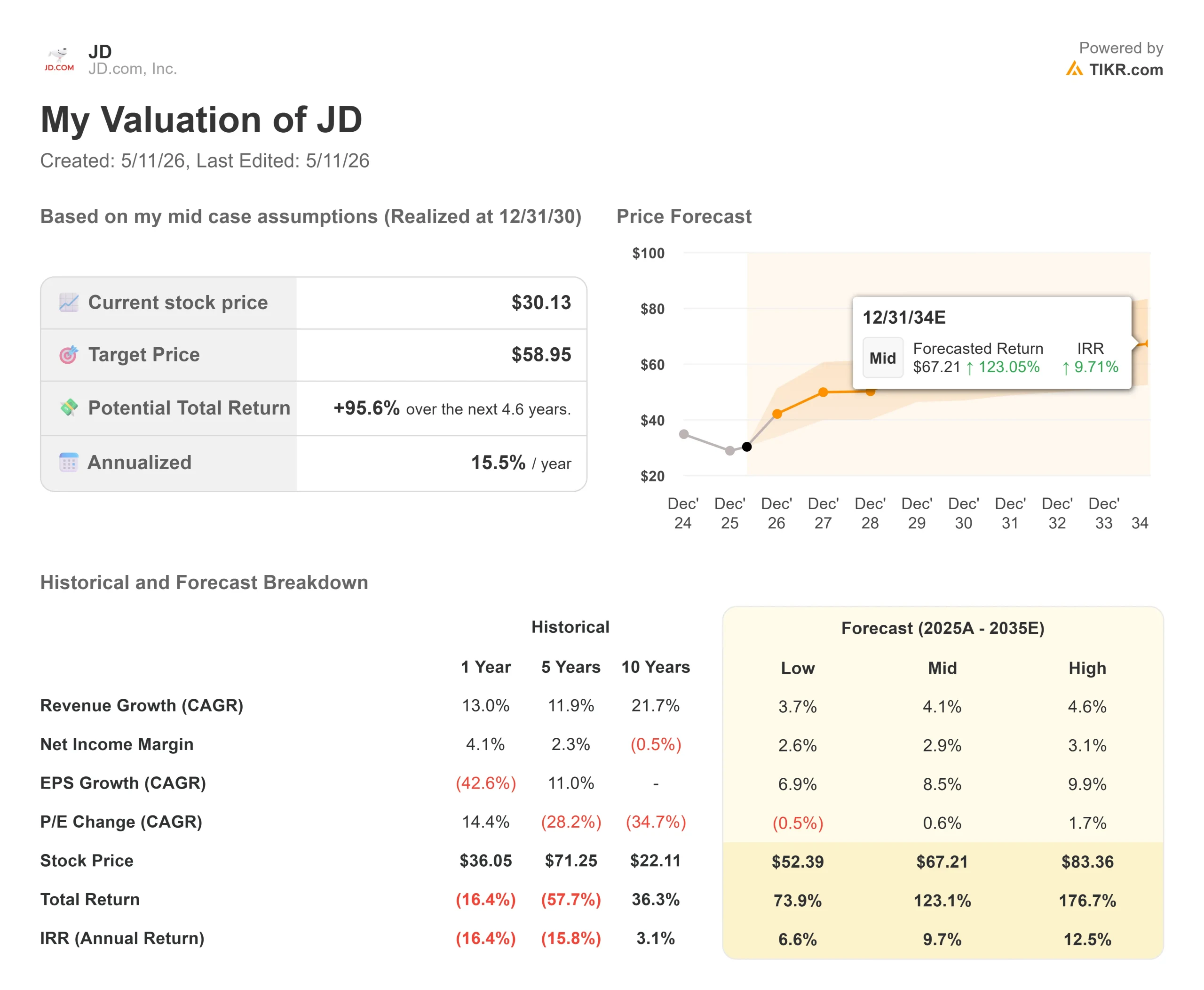

Key Stats for JD.com Stock

- Current Price: $30.13

- Target Price (Mid): ~$59

- Street Target: ~$40

- Potential Total Return: ~96%

- Annualized IRR: ~16% / year

- Earnings Reaction (Q4 2025, reported 3/5/26): +6.12%

- Max Drawdown: 31.81% (3/4/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

JD.com (JD) has fallen 27% from its 52-week high of $38.08, hitting a max drawdown of 31.81% on March 4, 2026, even as its core retail business keeps growing and its margins keep expanding. Thirty-six of 40 analysts covering the stock lean bullish, yet the share price sits at $30.13. Q1 2026 earnings land tomorrow, May 12, making this a critical inflection point. Bulls argue food delivery losses have peaked and JD’s supply chain moat is structurally undervalued. Bears say the subsidy war with Alibaba and Meituan has no clear end, and free cash flow tells a story the income statement is hiding.

What the Market Is Missing

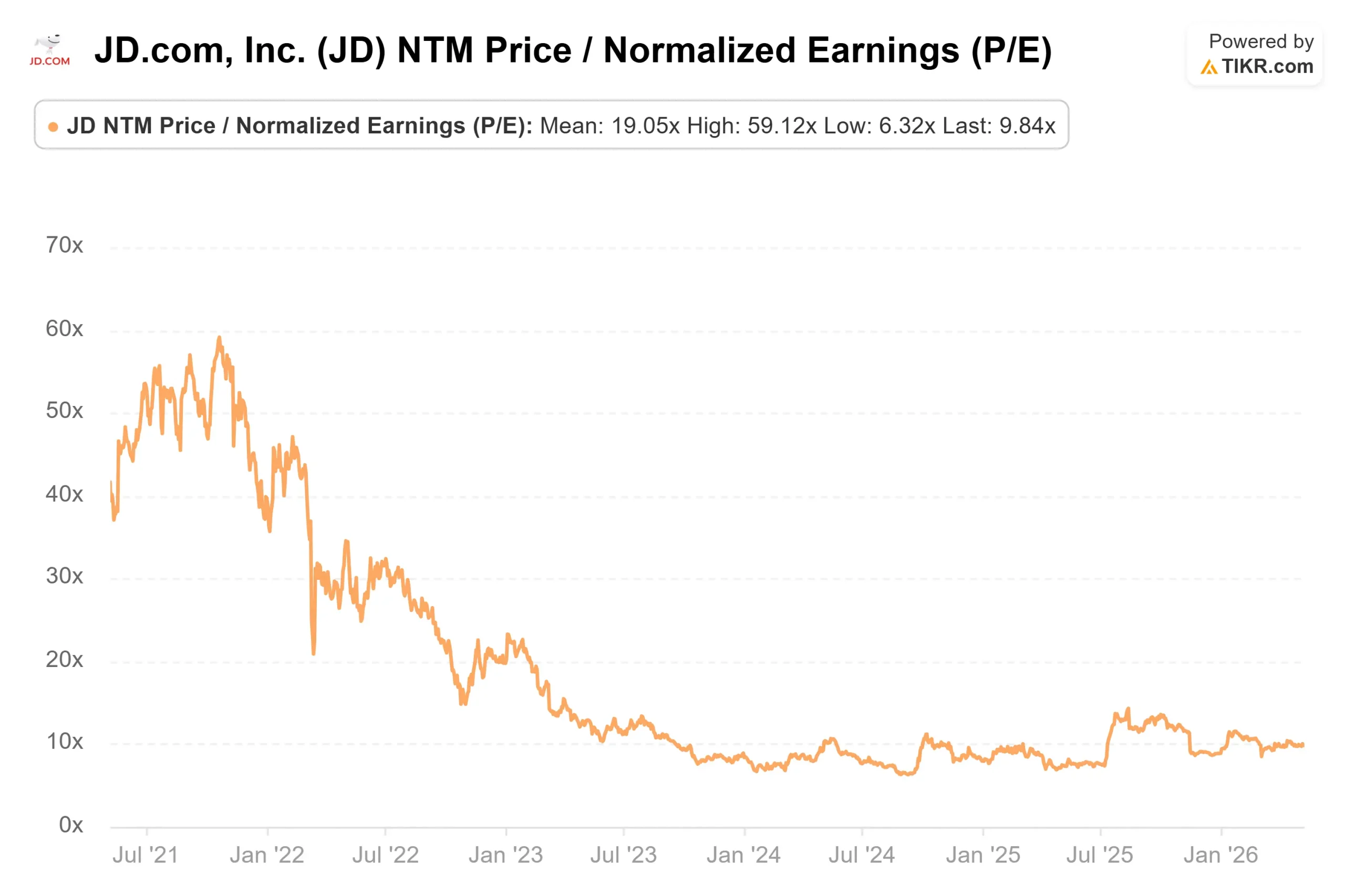

At $30.13, JD trades at an NTM P/E of 9.84x and an NTM EV/EBITDA of 7.69x, per TIKR. Revenue grew 13% in 2025 to RMB 1.309 trillion. JD Retail, the core product e-commerce segment, expanded its operating margin for the sixth consecutive year, reaching 4.6% in 2025, up from 2.7% in 2019. CFO Ian Su Shan said on the Q4 2025 earnings call that JD Retail’s non-GAAP operating income grew 25% year-on-year in 2025, and that “JD’s high single-digit long-term margin target remains unchanged.”

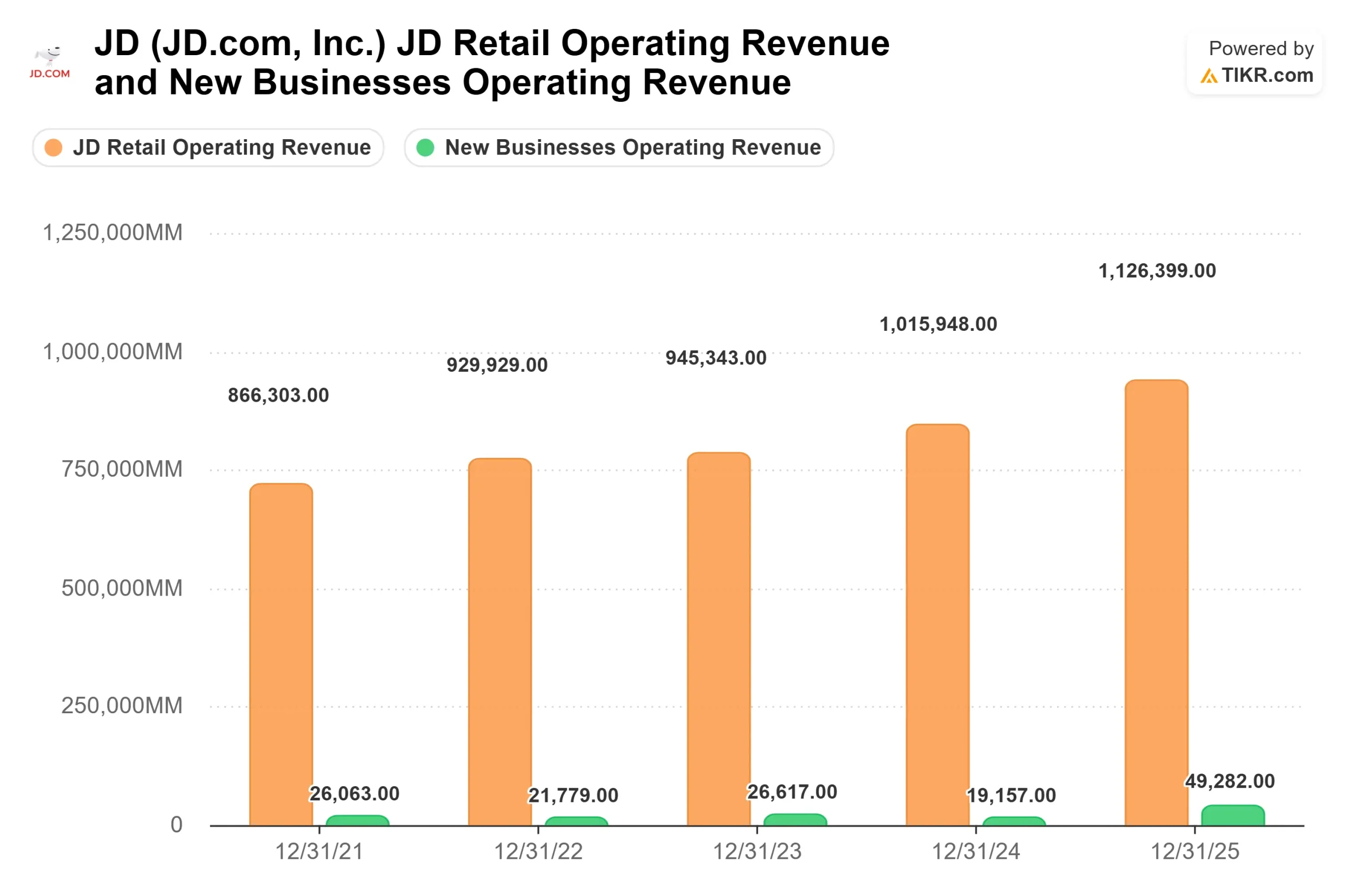

The discount exists because of what sits below the retail line. The New Businesses segment, which houses food delivery, posted a RMB 46.6 billion operating loss in 2025, per TIKR segment data. That dragged group-level free cash flow from RMB 43.9 billion in 2024 to RMB 6.3 billion in 2025, per TIKR actuals. The market is applying a compressed multiple to the entire business because of a single segment that management says has already passed its investment peak.

See historical and forward estimates for JD.com stock (It’s free!) >>>

What the Q4 Call Said

CEO Sandy Xu confirmed on the Q4 2025 earnings call that quarterly active customers grew 30% year-on-year in Q4, with annual active customers exceeding 700 million by year-end. User shopping frequency surged over 40% for the full year across all user groups. These engagement gains feed directly into the advertising flywheel: marketplace and marketing revenues grew 15% in Q4 and 18.9% for the full year, with food delivery contributing an incremental 2% to 3% to advertising revenue in Q4 alone.

On food delivery, Xu said total investment was cut “by nearly 20% quarter-on-quarter” in Q4, with the loss rate over GMV narrowing significantly from Q3. Total active food delivery merchants grew over 270% since launch. Ian Shan added that the company believes “investment in food delivery has peaked in 2025 and will trend downward this year if market competition trends towards becoming more rational.” That qualifier carries real weight. Whether Alibaba and Meituan rationalize their own food delivery spending is not within JD’s control.

General merchandise, which grew 15% for the full year per the Q4 call, is the cleaner growth story. Supermarket, fashion, and healthcare all posted strong results and are expected to sustain momentum in 2026. These categories carry better margins than electronics and are not dependent on government trade-in subsidies.

The Ceconomy Overhang

JD’s proposed $2.5 billion acquisition of Ceconomy, the German parent of MediaMarkt and Saturn, with over 1,000 stores across Europe, is currently under EU Foreign Subsidies Regulation review. According to a European Commission filing reported by Reuters, the EU has set a May 28 deadline to determine whether to open a full investigation into whether the deal involves Chinese state subsidies. Austria is separately reviewing it under foreign direct investment rules. Italy approved the deal with strict data protection conditions.

If it closes, JD gains a physical European retail network that complements Joybuy, its online marketplace launched in March 2026 in the UK, Germany, France, and the Netherlands. If the deal stalls, JD absorbs deal costs with no strategic return. The regulatory outcome is a genuine binary that investors cannot yet price with confidence.

See how JD.com performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $30.13

- Target Price (Mid): ~$59

- Potential Total Return: ~96%

- Annualized IRR: ~16% / year

See analysts’ growth forecasts and price targets for JD.com stock (It’s free!) >>>

The TIKR mid-case model targets approximately $59 per share by 12/31/30, representing roughly 96% total return and a ~16% annualized IRR. The model uses a mid-case revenue CAGR of around 4%, conservative relative to JD’s 13% growth in 2025, reflecting the law of large numbers on a RMB 1.3 trillion revenue base. Net income margin is forecast to expand to around 3% at the mid-case, up from 2.1% in 2025 per TIKR actuals.

The two growth drivers doing the work are advertising and marketplace revenues, which grew 19% in 2025 and benefit directly from JD’s accelerating user engagement, and general merchandise, where category expansion in supermarket, fashion, and healthcare continues to outpace the core electronics business.

The key margin driver is food delivery losses normalizing. TIKR consensus estimates show free cash flow recovering to around RMB 44 billion in 2026 from RMB 6.3 billion in 2025, which would represent a near-full restoration of the pre-food-delivery FCF profile.

The primary risk is straightforward: if the food delivery war persists at current intensity, JD’s investment timeline extends, FCF recovery is delayed, and the market continues applying a depressed multiple to the whole business. JD closed 2025 with RMB 225 billion in total liquidity, including cash, restricted cash, and short-term investments, per Ian Shan on the Q4 call, providing a meaningful buffer against a prolonged investment cycle. The company also paid $1 per ADS in dividends and repurchased $3 billion in shares in 2025, canceling 6.3% of outstanding shares, per the Q4 earnings call.

Conclusion

Watch tomorrow’s New Businesses’ operating loss figure on May 12. If food delivery losses narrow quarter-on-quarter and JD Retail sustains double-digit revenue growth as electronics comps normalize into the second half of 2026, the investment thesis firms up. If losses hold or management softens its language on the investment peak, the discount persists regardless of how core retail performs.

JD.com trades at under 10x forward earnings because the market is paying for today’s food delivery losses rather than tomorrow’s margin recovery. That gap closes when the losses do.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in JD.com?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up JD.com, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track JD.com alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!