Key Stats for Idexx Stock

- 52-Week Range: $356.1 to $770

- Current Price: $577.4

- Street High Target: $823

What Happened?

IDEXX Laboratories (IDXX), the global leader in veterinary diagnostics and practice software, is building a recurring revenue flywheel that delivered 10.4% revenue growth and 31.6% operating margins in fiscal 2025, even as U.S. clinic visits declined 1.9% for the year.

The January announcement of incoming CEO Michael Erickson, a 15-year IDEXX insider who has run the company’s Global Point of Care Diagnostics and Telemedicine divisions, signals continuity over disruption as the company enters a product cycle richly stocked with new platforms.

That product cycle is already showing up in the numbers: IDEXX placed 6,400 inVue Dx analyzers in 2025, a point-of-care cytology platform that processes slides automatically without manual preparation, beating the company’s original 4,500-unit target and contributing approximately 200 basis points to full-year revenue growth.

Jay Mazelsky, President and CEO, stated on the Q4 2025 earnings call that “2025 was a defining year for our company,” pointing to the successful commercialization of the IDEXX Cancer Dx canine lymphoma test, which now reaches nearly 6,000 reference lab customers including 18% who are new to the IDEXX network.

IDXX stock, trading at $577.44 against a 52-week high of $769.98, enters 2026 anchored by a $45 billion-plus total addressable market, a 5,500-unit inVue Dx placement target, a mid-2026 launch of mast cell tumor detection on its Cancer Dx panel, and management’s long-term EPS growth potential of 15%-plus backed by consistent share buybacks.

Wall Street’s Take on IDXX Stock

IDXX’s ability to grow recurring diagnostic revenue 8% to 10% organically in 2026, despite a sector backdrop that includes a projected 2% decline in U.S. same-store clinical visits, reframes this as a volume-and-utilization story rather than a visit-volume story.

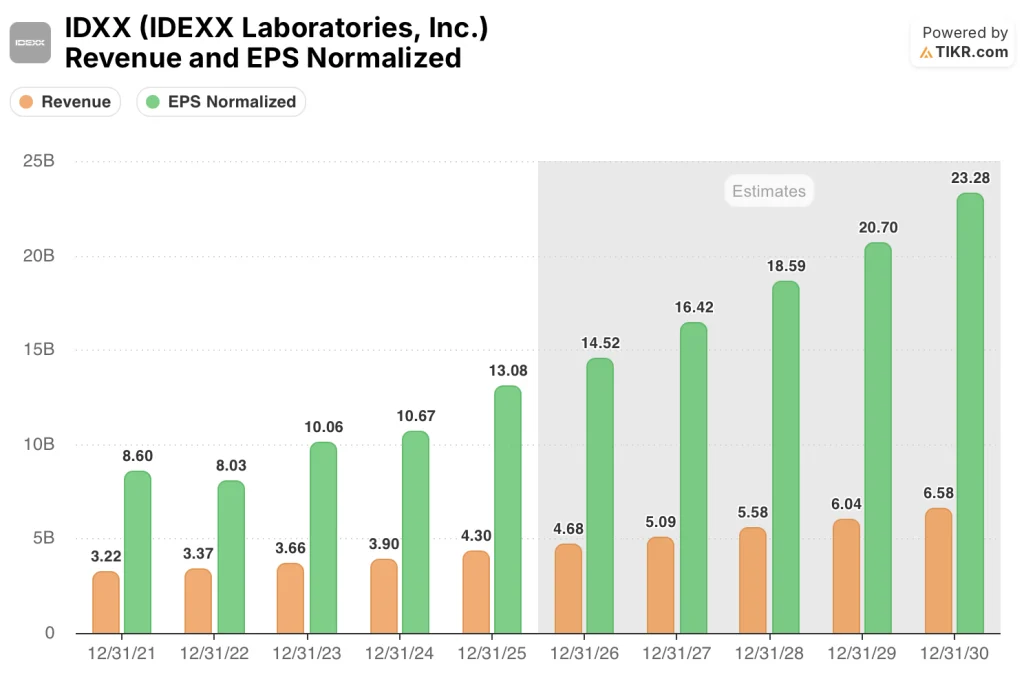

Consensus sees IDXX revenue reaching $4.7 billion in 2026 and $5.1 billion in 2027, while normalized EPS is expected to climb from $13.08 in 2025 to $14.52 in 2026 and $16.42 in 2027, each figure anchored to the expanding installed base of premium instruments now totaling more than 78,000 Catalyst analyzers and 6,400 inVue Dx units globally.

Nine of 15 analysts covering IDXX carry a buy or outperform rating, with five holds and one sell, and a mean price target of $742.54, implying 28.6% upside from the April 6 close of $577.44, while the bull case target sits at $823, reflecting Wall Street’s debate over whether accelerating diagnostic frequency can fully offset macroeconomic pressure on wellness visits.

The spread between $470 and $823 is genuinely instructive: the low end prices in a prolonged consumer spending downturn that keeps wellness visit declines above 2%, while the $823 target underwrites IDXX executing on inVue FNA expansion, the Cancer Dx mast cell launch, and continued 12%-plus international CAG Diagnostics recurring growth through 2027.

Trading at roughly 40x forward earnings against a 5-year average closer to 55x, with normalized EPS growing at an 11% consensus CAGR through 2027 and operating margins expanding 30 to 80 basis points in 2026, IDXX stock appears undervalued given the combination of durable recurring revenue, accelerating diagnostic frequency, and a $1.1 billion long-term Cancer Dx revenue opportunity that is not yet priced in.

At the Raymond James Institutional Investor Conference on March 2, Mazelsky committed to a Cancer Dx panel detecting 50%-plus of common canine cancers by end of 2028, directly expanding the panel’s addressable opportunity and extending the premium instrument installed base’s monetization runway.

A deterioration in non-wellness visit volumes, which account for roughly 70% to 75% of IDXX’s diagnostic revenue despite representing only 60% of total visits, is the single development that would break the model’s core volume assumption.

Q2 2026 guidance, which will confirm whether inVue FNA consumables are ramping and whether the international commercial expansion in Germany, the U.K., and Australia is driving incremental CAG Diagnostics recurring revenue, is the next hard checkpoint for the thesis.

IDEXX Laboratories Financial Performance

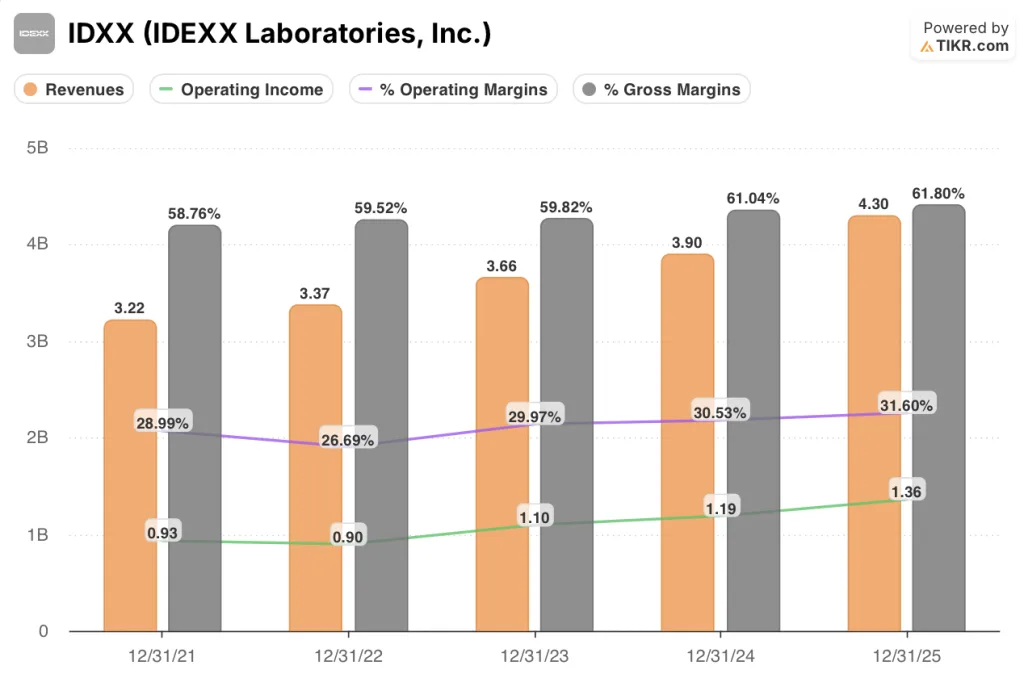

IDXX revenue expanded from $3.9 billion in fiscal 2024 to $4.3 billion in fiscal 2025, a 10.4% year-over-year gain that accelerated meaningfully from the 6.5% growth posted the prior year.

Gross profit rose 11.8% to $2.7 billion in fiscal 2025, with gross margins expanding to 61.8% from 61.0% the prior year, reflecting the strong consumable pull-through from inVue Dx placements and above-average gross margins in the company’s cloud-based reference laboratory business.

The margin recovery that began after operating margins troughed at 26.7% in fiscal 2022 has now compounded for three consecutive years, reaching 31.6% in fiscal 2025 from 30.5% in 2024 and 30.0% in 2023, demonstrating structural operating leverage as IDXX’s recurring revenue base scales faster than its cost structure.

What Does the Valuation Model Say?

The TIKR model’s mid-case price target of $946.36, built on 8.8% revenue CAGR through December 2030 and a net income margin expanding to 26.0%, implies 63.9% total return from current levels, a figure that looks striking against the $577.44 price until you map the assumptions to what IDEXX has already delivered: 10.4% revenue growth and 24.6% net income margins in fiscal 2025 alone.

IDXX appears undervalued at current levels, trading at approximately 40x forward earnings while the model underwrites only 8.8% revenue growth, a target the company has already exceeded in its most recent fiscal year.

The question the TIKR model forces is whether IDXX deserves a premium for its platform optionality or whether the market is right to apply a compressed multiple while clinic visits remain under pressure.

What Has to Go Right

- inVue Dx consumable revenue per instrument must track to the $3,500 to $5,500 annual target as the FNA mast cell tumor launch, now in controlled rollout, scales through corporate accounts in the second half of 2026

- Cancer Dx must sustain above-50% inclusion in broader diagnostic panels, building toward the $1.1 billion total addressable opportunity management cited at the Q4 earnings call, with the mast cell expansion adding incremental panel value at no price increase

- International CAG Diagnostics recurring revenue must sustain double-digit growth as the 2025 commercial expansions in Germany, the U.K., and Australia move from onboarding to full productivity, consistent with the 12% international organic growth posted in Q4 2025

- Operating margins must continue expanding toward the 32.0% to 32.5% fiscal 2026 guide, driven by gross margin leverage on consumables growth and double-digit cloud-based software recurring revenue

What Could Go Wrong

- Non-wellness visit volumes, currently the source of 70% to 75% of IDXX’s diagnostic revenue, could deteriorate beyond the 2% U.S. same-store decline baked into 2026 guidance if consumer spending pressure intensifies across middle and lower income household cohorts

- inVue Dx consumable ramp could miss targets if corporate account placement cycles, noted as “a little bit longer” by management, push meaningful pull-through revenue into fiscal 2027 rather than 2026

- CEO transition risk, with Michael Erickson assuming the role May 12, 2026, is minimal given his 15-year IDEXX tenure, but the concurrent EVP departure of Nimrata Hunt and $2.3 million separation package filed March 26 signals meaningful reorganization at the senior leadership level

- Foreign exchange, which provided a 60-basis-point tailwind to 2026 guidance at current rates, reverses to a headwind if the U.S. dollar strengthens significantly against the euro or Australian dollar

Should You Invest in IDEXX Laboratories, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up IDXX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track IDEXX Laboratories, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze IDXX stock on TIKR for Free →