Key Stats for GE Aerospace Stock

- 52-Week Range: $176 to $348

- Current Price: $298

- Street Mean Target: $351

- Street High Target: $425

- TIKR Model Target (Dec. 2030): $537

What Happened?

GE Aerospace (GE), the world’s largest jet engine maker by installed base, beat fourth-quarter earnings estimates by 10% and raised its 2026 profit outlook by $1 billion, even as the broader industrials sector sold off on Middle East conflict concerns.

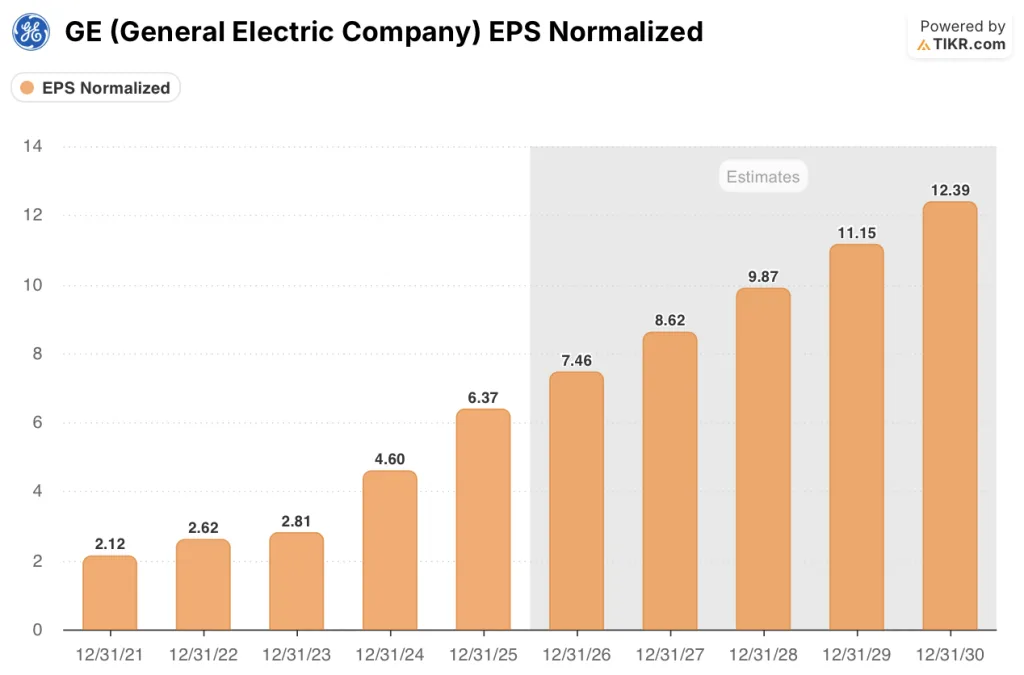

The Q4 beat was not a one-quarter event: adjusted EPS came in at $1.57 against the $1.43 estimate, and full-year 2025 EPS reached $6.37, a 38.5% jump from the prior year.

GE’s $190 billion backlog, which grew nearly $20 billion over the past year, provides multi-year revenue visibility that few industrials companies can match, with commercial services orders alone up 27% in 2025.

Larry Culp, Chairman and CEO, stated on the Q4 2025 earnings call that “we expect operating profit of $9.85 billion to $10.25 billion, up $1 billion at the midpoint,” then added that the company expects to generate more than $20 billion of cash between 2024 and 2026 to reinvest in the business.

The LEAP engine program, which powers Boeing 737 and Airbus A320neo narrowbody jets and is central to GE’s aftermarket services growth, saw shop visit volume rise 27% in 2025, with its installed base expected to roughly triple between 2024 and 2030.

GE also committed $1 billion to U.S. manufacturing investments in 2026, adding 5,000 jobs and expanding defense engine capacity by over $275 million, positioning the company to benefit from the Pentagon’s push to expand the defense industrial base.

Wall Street’s Take on GE Stock

The Q4 beat and raised 2026 guidance reframe GE Aerospace as a compounding earnings machine, not a cyclical play subject to aviation traffic variability: the $190 billion backlog and LEAP aftermarket ramp make the forward trajectory structurally visible.

GE’s normalized EPS reached $6.37 in 2025 and consensus projects it growing to around $7 in 2026, with the LEAP program’s growing external service channel and CFM56 retirements tracking below the company’s own prior estimates, both extending the aftermarket tailwind further into the decade.

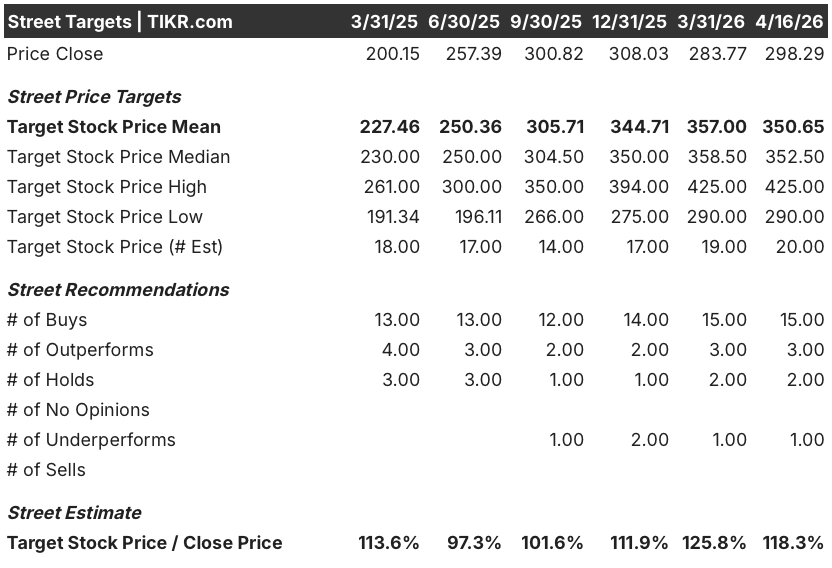

Fifteen analysts rate GE a buy or better, three rate it outperform, two hold, and one each underperform and sell, with the mean price target sitting at around $351 against a current price of $298, implying around 18% upside; the Street is waiting specifically for 2026 LEAP shop visit volumes to confirm the mid-teens services growth guidance is tracking on schedule.

The spread between the $290 low target and the $425 high target reflects a real debate: bears see limited re-rating potential in a macro environment where airlines face jet fuel cost pressure from the Middle East conflict, while bulls anchor to the services backlog and the LEAP installed base expected to roughly triple by 2030.

Priced at around 40x 2026 consensus EPS against a business growing normalized earnings at 17% per year with a $190 billion backlog and over 100% free cash flow conversion, GE Aerospace stock appears undervalued relative to its own recent trading range and the quality of its earnings visibility.

GE’s Palantir partnership for AI-driven military aircraft sustainment, paired with the Indian Air Force F404 depot contract signed in April, signals that the defense aftermarket is building recurring revenue streams the commercial services story tends to overshadow.

If Middle East-driven fuel cost pressures force airlines to defer engine shop visits or cut capacity, the commercial services revenue trajectory underpinning the 2026 outlook could fall short of the mid-teens guidance.

The Q1 2026 earnings call is the first real test: LEAP internal shop visit volume and spare parts delinquency rates will either confirm or challenge the services growth ramp, with CFM56 retirements in the 2% range being the key metric to watch.

GE Aerospace Financials

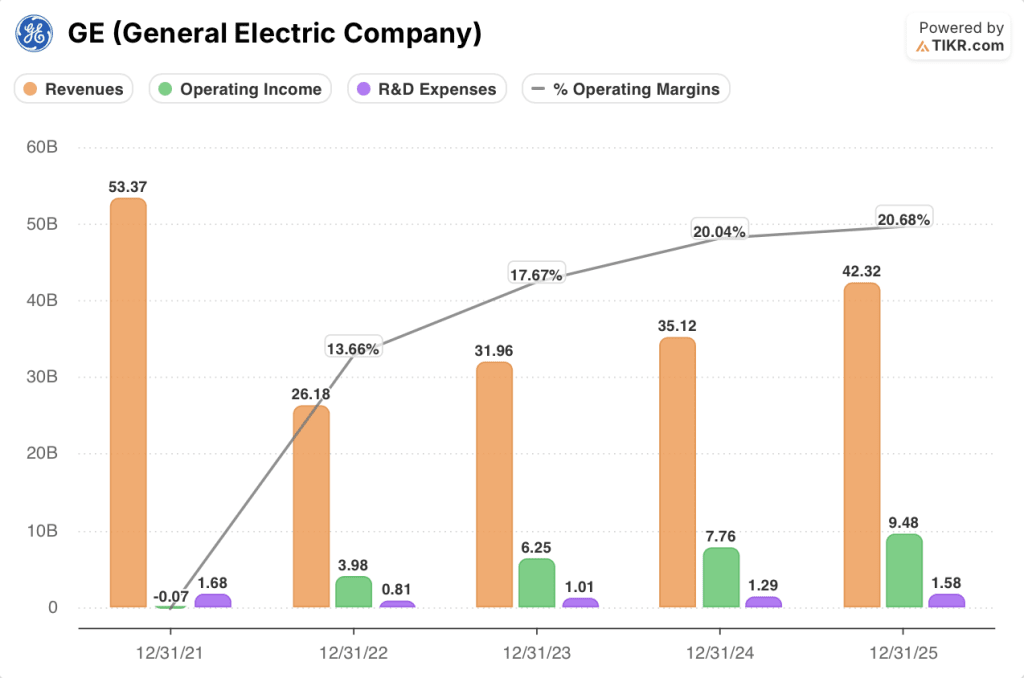

GE Aerospace grew total revenues from $35.12 billion in 2024 to $42.32 billion in 2025, an 18.5% increase that reflects the simultaneous ramp in both commercial engine deliveries and aftermarket services volume.

The operating leverage story is equally compelling: operating income expanded from $7.76 billion to $9.48 billion over the same period, a 22.3% gain that outpaced revenue growth and pushed operating margins from 20% to 20.7%.

Gross margins tell the same directional story, expanding from 31% in 2024 to 31.5% in 2025, as the higher-margin services mix, driven by LEAP shop visit growth and CFM56 aftermarket strength, continued to offset the dilutive effect of new engine deliveries.

The one tension in the income statement is R&D, which grew from $1.29 billion in 2024 to $1.58 billion in 2025: a deliberate investment in the CFM RISE open-fan program and next-generation defense engines, but a cost line that will keep rising even as GE targets $10 billion in operating profit in 2026.

What Does the Valuation Model Say?

The TIKR mid-case model projects GE Aerospace reaching a price of around $751 by the end of 2030, anchored to an around 8% revenue CAGR and net income margins expanding toward around 18%, both assumptions directly supported by the company’s own $190 billion backlog and accelerating LEAP aftermarket capacity build-out.

With normalized EPS compounding at 17% per year and free cash flow conversion running above 100%, the current forward multiple of around 40x underprices what is effectively a durable services franchise, leaving GE Aerospace stock appearing undervalued against the mid-case target that implies an around 80% total return from today’s price.

The central tension for GE Aerospace stock is whether the LEAP ramp will actually close the gap between what airlines need and what the supply chain can deliver in 2026.

What Has to Go Right

- LEAP internal shop visit volume grows 25% in 2026 as guided, confirming the mid-teens services revenue trajectory and validating the $9.85 to $10.25 billion operating profit range

- CFM56 retirements remain in the 2% range through 2028, sustaining 2,300 to 2,400 annual shop visits and extending the narrowbody aftermarket tailwind further than the Street currently models

- The $1 billion U.S. manufacturing investment and Palantir AI partnership accelerate defense engine delivery timelines, adding a second durable growth engine beyond commercial services

- GE9X losses double in 2026 as guided but prove manageable, with LEAP OE reaching profitability on schedule as production scales toward 2,500 annual units

What Could Go Wrong

- Prolonged Middle East conflict keeps jet fuel prices elevated, reducing airline capacity utilization and deferring engine shop visits below the 2026 guidance assumptions

- Rare earth supply constraints, specifically yttrium shortages already affecting North American aerospace coating suppliers, interrupt GE’s engine coating supply chain and slow delivery timelines

- The $275 million-plus defense investment runs into the same supply chain friction that limited commercial output in 2024 and 2025, delaying the DPT segment’s path toward its $1.55 to $1.65 billion 2026 profit target

- R&D expense continuing to increase toward $3 billion annually compresses margins even as revenue grows, limiting operating leverage that the TIKR model assumes will materialize

Should You Invest in GE Aerospace?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE Aerospace alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GE stock on TIKR for Free →