Key Stats for Verizon Stock

- Current Price: $46.52

- Target Price (Mid): ~$73

- Street Target: ~$52

- Potential Total Return: ~57%

- Annualized IRR: ~10% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

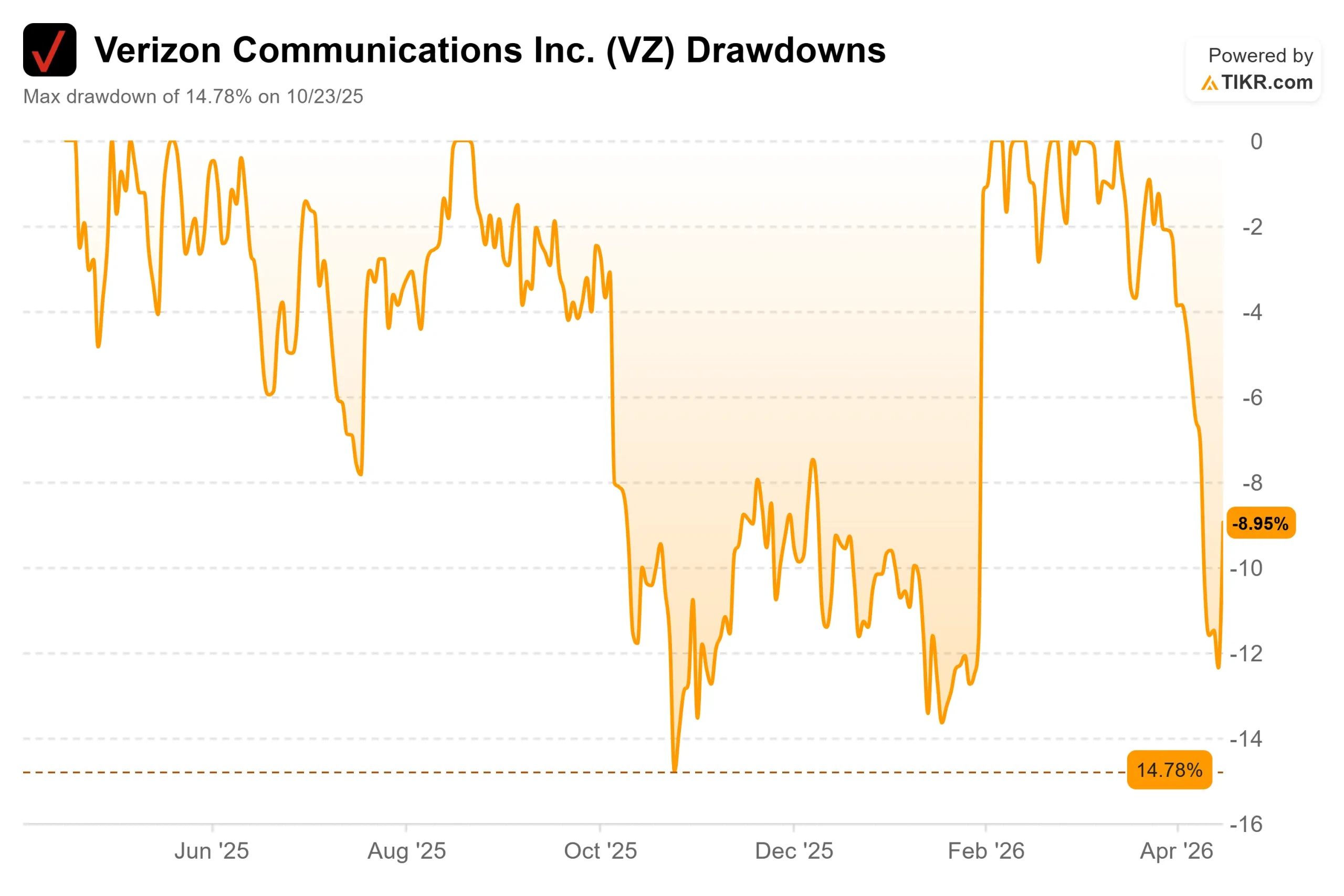

For most of the past five years, Verizon (VZ) was a stock investors held for the dividend and little else. That changed after Q4 2025 earnings on January 30, which pushed VZ toward a recent high near $50.

The stock has since retreated to $46.52, sitting nearly $5 below the Street’s mean analyst target of $51.58. With Q1 2026 earnings due April 27, investors are asking: Is this pullback a buying opportunity, or a sign the re-rating has run ahead of the fundamentals?

The Q4 results genuinely changed the story. Verizon posted 616,000 postpaid phone net additions, its best quarter since 2019, alongside 372,000 broadband net additions. The Frontier Communications acquisition closed January 20, giving Verizon a combined fiber footprint covering over 30 million homes and businesses.

CEO Dan Schulman was direct in Verizon’s earnings press release: “We are exiting 2025 with strong momentum. Our 2026 guidance reflects the beginning of our turnaround, and is a step function change from our past five-year historical average.”

Two weeks before that earnings call, though, Verizon suffered a significant setback. On January 14, 2026, a software issue in the company’s 5G Standalone core network caused a nationwide outage lasting over 10 hours and affecting more than 1.5 million customers.

Schulman acknowledged it on the call, saying Verizon “did not meet the standard of excellence our customers expect,” and the FCC’s Public Safety and Homeland Security Bureau launched an investigation into the outage’s effects on consumers and public safety entities.

For a turnaround built entirely on rebuilding customer trust and reducing churn, this was the worst possible timing. The key question on April 27 is whether Q1 churn moved higher because of it.

See historical and forward estimates for Verizon stock (It’s free!) >>>

Is Verizon Undervalued Today?

At $46.52, Verizon trades at roughly 9.5x forward earnings and 6.8x forward EV/EBITDA, with a 6.0% dividend yield. Those are the multiples of a utility, not a turnaround.

Peer context matters here. AT&T (T) trades at 7.2x forward EV/EBITDA against a current price of $26.40 and an analyst mean target near $30. Comcast (CMCSA) trades at 6.0x. Verizon’s small premium to AT&T reflects its scale, but both are running nearly identical convergence strategies, and neither has earned a growth multiple yet.

The bull case starts with Frontier. The acquisition gives Verizon over 30 million fiber passings, locations where fiber service can be sold, and management is targeting 40–50 million over the medium term. Schulman’s strategy is to bundle wireless and home fiber to reduce churn, the rate at which customers cancel service. CFO Anthony Skiadas called it “a pivotal opportunity in 2026” on the Q4 earnings call.

Management guided 750,000 to 1 million postpaid net additions in 2026, two to three times the 2025 total, driven by churn reduction rather than aggressive promotions. On top of that, the board authorized up to $25 billion in share repurchases over the next three years and declared Verizon’s 20th consecutive annual dividend increase. With management guiding free cash flow of at least $21.5 billion in 2026, the capital return program has real funding behind it.

The bear case is equally grounded. Postpaid phone churn rose to 0.95% in Q4 2025 per Verizon’s Q4 2025 earnings disclosure, up from 0.88% the prior year. LTM net debt stands at $165.8 billion, and the Frontier integration adds capital demands to an already leveraged balance sheet, with interest expense forecast near $7.5 billion annually through mid-decade. The January network outage and the ongoing FCC investigation are wildcards: the churn impact won’t be visible until April 27.

See how Verizon performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $46.52

- Target Price (Mid): ~$73

- Potential Total Return: ~57%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Verizon stock (It’s free!) >>>

The TIKR mid-case model targets a price of around $73 by 12/31/30, implying roughly 57% total return and a ~10% annualized return from today’s $46.52. The two revenue drivers are broadband subscriber growth on the Frontier fiber platform and wireless service revenue stabilization as churn improves. Net income margin expands toward around 16% in the mid case, supported by the $5 billion OpEx savings program and Frontier synergies.

The low case is instructive. At around 1.5% annual revenue growth and margins near 15%, the model produces a 2030 target near $76, with most of that gain coming from dividends rather than price appreciation, and an annualized return of roughly 6%. That is thin compensation for investors carrying $165.8 billion in net debt and a turnaround that has yet to fully prove itself. The primary risks are slower-than-expected churn recovery, elevated interest expense near $7.5 billion annually, and Frontier integration costs running ahead of estimates.

Conclusion

The number to watch on April 27 is postpaid phone churn. If Q1 churn rose following the January outage, the turnaround timeline extends and the re-rating stalls. If it holds flat or improves, Schulman’s thesis earns its first real proof point.

At $46.52, Verizon offers a 6% dividend, a $25 billion buyback, 30 million fiber passings, and a TIKR mid-case pointing to around $73 by 12/31/30. The risk-reward favors patient investors who can wait for execution to catch up with the thesis.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Verizon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Verizon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Verizon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Verizon on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!