Key Stats for Chipotle Stock

- 52-Week Range: $30 to $58

- Current Price: $35

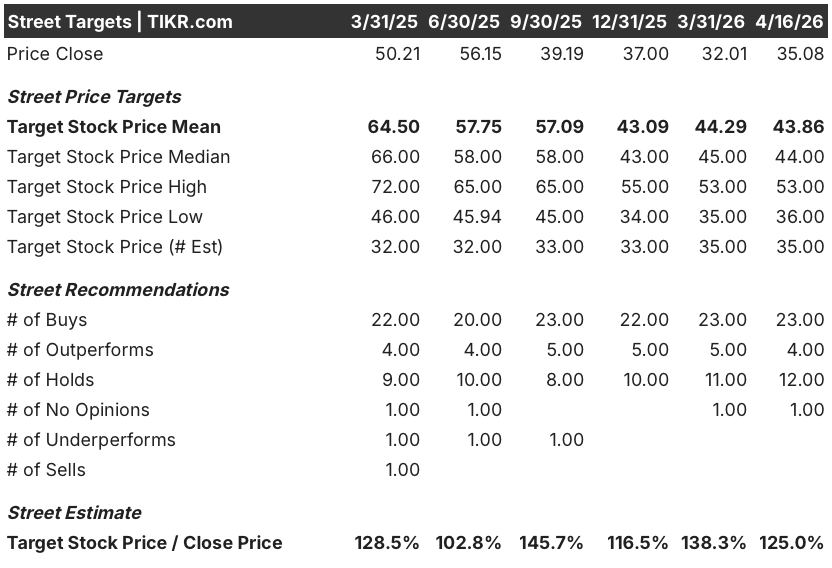

- Street Mean Target: $44

- Street High Target: $53

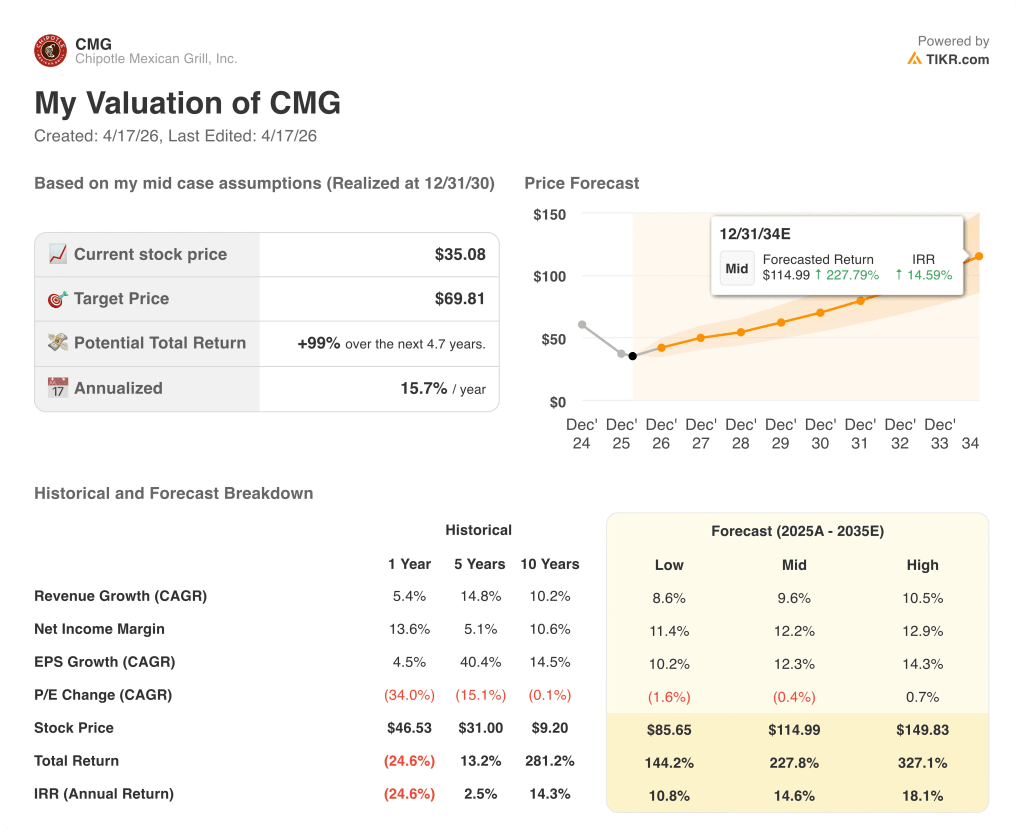

- TIKR Model Target (Dec. 2030): $70

What Happened?

Chipotle Mexican Grill (CMG), the fast-casual restaurant chain that serves customizable burritos, bowls, tacos and salads made from fresh ingredients at roughly 4,000 company-owned locations across North America, Europe and the Middle East, is trading near multi-year lows while its new leadership executes a recovery playbook built around equipment, menu innovation and loyalty.

The company reported Q4 2025 revenue of $2.98 billion, up 4.9% year over year, beating the analyst estimate of $2,964 million, while adjusted diluted EPS of $0.25 matched expectations, capping a full year in which revenue grew 5.4% to $11.93 billion but comparable restaurant sales declined 1.7%.

Management guided for 2026 comparable sales to be roughly flat, citing a consumer environment where younger, lower-income guests have pulled back on higher-priced meals, a dynamic that has pressured comps since mid-2024 and triggered what analysts call “slop-bowl fatigue” — a weariness among cost-conscious diners toward premium grain bowl formats.

The more important number is inside the restaurant base: 350 locations already running the high-efficiency kitchen equipment package — which reduces prep time by 2 to 3 hours and delivers juicier, more consistent proteins — are showing hundreds of basis points of comp improvement over the chain average, and management expects roughly 2,000 locations to have the full package by year-end.

Scott Boatwright, Chief Executive Officer, stated on the Q4 2025 earnings call that “we still have confidence in the long-term algorithm of getting to $4 million AUVs and approaching 30% margins,” anchoring the recovery thesis to average unit volumes (the revenue a single restaurant generates annually) and the operating leverage that flows from higher-throughput locations.

The high-protein menu launched in late December 2025, which includes a single taco at $3.5 and a protein cup around $4 targeting GLP-1 users and younger calorie-conscious diners, delivered a record digital sales day and drove extra protein incidence up 35%, providing the first concrete evidence that the relaunch strategy is landing before Chicken al Pastor, the brand’s most-requested limited time offer, returned to menus in February.

Chipotle Mexican Grill stock has shed roughly 40% from its 52-week high of $58, weighed down by the comp decline narrative and the exits of major holders including Pershing Square Capital Management and Viking Global, which each dissolved their CMG positions in Q4 2025.

Wall Street’s Take on CMG Stock

The flat comp guide is not the story — the 2,000-restaurant equipment rollout is, because the stores already running it are recovering at a rate the current stock price does not reflect.

Chipotle Mexican Grill’s normalized EPS consensus sits at roughly $1.14 for 2026, down around 3%, with revenue growing around 9% to $12.95 billion, a deceptively weak headline driven by the pricing-below-inflation decision management made deliberately to protect value perception while the equipment and menu initiatives build momentum.

Coverage is 27 buy-equivalent ratings (23 buys, 4 outperforms) out of 40 analysts on Chipotle Mexican Grill stock, with a mean price target of ~$44, implying around 25% upside from current levels, a consensus that has compressed sharply from the ~$65 mean target a year ago as the comp disappointment repriced expectations toward a recovery scenario rather than a growth premium.

The target range from $36 to $53 captures the genuine debate: the low end is held by analysts who believe flat-to-negative comps persist if the macro weakens further and the equipment rollout fails to accelerate traffic at the system level, while the high end prices in the equipment-driven comp re-acceleration alongside four annual LTOs and the spring loyalty relaunch driving digital penetration from 30% toward 40% of sales.

Trading at roughly 30.8x fiscal 2026 normalized EPS, at a multiple that represents less than half its 2021-2024 average forward P/E of approximately 55-60x, against a 10-year EPS CAGR of 14.5% and a clear operational catalyst in the equipment rollout, Chipotle Mexican Grill stock appears undervalued relative to the earnings power the algorithm implies once unit volumes recover toward the $4 million target.

The signal that changes the market’s narrative is already in the data: restaurants with the high-efficiency equipment package are delivering hundreds of basis points of comp improvement above the chain average in a flat-to-negative same-store sales environment, meaning the 2026 flat guidance already embeds a significant rollout tailwind that management has explicitly characterized as conservative.

If beef and avocado cost inflation remains in the mid-single-digit range through the second half of 2026 while Chipotle prices at only 1% to 2%, the 150 basis points of planned pricing-versus-inflation dislocation widens further and restaurant-level margins compress below the 23% range, breaking the margin recovery thesis before the equipment benefit fully flows through.

Q1 2026 is the key checkpoint: the underlying comp trend (guided to -1% to -2% before the winter storm impact) and restaurant-level margin progression will reveal whether the high-protein launch and Chicken al Pastor are generating the traffic inflection that management needs to sustain confidence in the full year flat guide.

What Does the Valuation Model Say?

The TIKR mid-case model projects a target price of $70 over the next 5 years, implying around 99% total return, built on a revenue CAGR of around 10% and net income margin recovery to roughly 12%, both grounded in the 350-to-2,000-restaurant equipment rollout that management has already flagged as delivering hundreds of basis points of comp outperformance at equipped locations.

With a low-case reaching roughly $86, a mid-case of roughly $115 and a high case of roughly $150 by fiscal 2030, all three scenarios produce meaningful returns from today’s price — and against a 30.8x forward multiple on a business with a 14% 10-year EPS CAGR and a proven path to $4 million AUVs and approaching 30% restaurant margins, Chipotle Mexican Grill stock is undervalued at a multiple the market has not assigned to this brand since before its last major recovery cycle.

The entire investment case hinges on one question: does the high-efficiency equipment rollout translate system-wide comp improvement in the second half of 2026, or does it remain a restaurant-level phenomenon that cannot overcome macro headwinds at the portfolio level?

What Has to Go Right

- The 2,000-restaurant equipment target is hit by year-end and the comp differential seen in the 350 equipped stores (hundreds of basis points above chain average) holds at scale, accelerating 2026 comps from flat toward the low positive range

- Four annual LTOs, starting with Chicken al Pastor (the most-requested LTO in brand history by social media volume), drive new guest acquisition and frequency increases among the core 60%-plus over-$100,000-income customer base

- The spring rewards relaunch widens in-restaurant loyalty penetration from its current 20% toward the 90% rate already seen in app transactions, deepening the personalization and targeted re-engagement capabilities management built during 2025

- International markets gain momentum: the Middle East footprint nearly doubles in 2026 with Alshaya Group, and the first restaurants open in Mexico, Singapore and South Korea, diversifying the revenue base beyond the U.S. comp cycle

What Could Go Wrong

- Beef and avocado inflation stays elevated in the second half of 2026, keeping cost of sales above mid-30% and preventing the pricing-versus-inflation gap (guided at 150bps for the full year) from narrowing, capping restaurant-level margin recovery below 24%

- The consumer backdrop deteriorates further, with the under-$100,000 income cohort — already pulling back on $15-plus bowls — reducing frequency even as the higher-income cohort holds, keeping system comps negative through Q3 and eroding confidence in the flat full-year guide

- Pershing Square and Viking Global’s simultaneous exit signals that institutional holders who drove the prior valuation premium are not returning at these multiples until two to three quarters of positive comps are confirmed, extending the multiple compression

- The CMO search introduced execution risk: Chipotle is going into its highest-spend marketing year (LTOs, rewards relaunch, protein campaign) without a permanent Chief Marketing Officer, and the new Chief Digital Officer role has not yet been filled

Should You Invest in Chipotle Mexican Grill, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CMG stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Chipotle Mexican Grill, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CMG stock on TIKR for Free →