Key Stats for Lowe’s Stock

- 52-Week Range: $210 to $293

- Current Price: $275

- Street Mean Target: $286

- Street High Target: $325

- TIKR Model Target (Jan. 2031): $372

What Happened?

Lowe’s Companies, Inc. (LOW), the second-largest home improvement retailer in the United States with roughly 1,759 stores and $86 billion in annual sales, reported its best comparable-sales quarter since 2022 while Lowe’s stock sits near the lower half of its 52-week range.

Q4 comparable sales rose 1.3%, beating analyst expectations of 0.4% growth, with strength in Pro (professional contractor) sales, online, and home services more than offsetting ongoing softness in big-ticket DIY discretionary projects like kitchen remodels and flooring installations.

Two major acquisitions completed in 2025, Foundation Building Materials (FBM), a wholesale distributor of drywall, ceilings, and insulation, and Artisan Design Group (ADG), an interior flooring and installation services company, add roughly $8 billion in combined 2026 sales and position Lowe’s to capture a larger share of homebuilder spending when housing construction recovers.

The company’s structural share-gain story is gaining measurable traction: Marvin Ellison, Chairman and CEO, stated on the Q4 2025 earnings call that “whatever the macro environment provides, we will outperform the macro,” citing three consecutive quarters of positive comps, 30 million MyLowe’s Rewards members, and a Pro business that is outperforming in planned spend and backlog stability.

Lowe’s generated $7.7 billion in free cash flow in fiscal 2025 and returned $2.6 billion to shareholders through dividends, while simultaneously absorbing nearly $10 billion in acquisition spending, demonstrating the cash generation capacity of the business even in a soft housing environment.

The setup for 2026 and beyond is anchored to a structural thesis: U.S. homes average 44 years old, home equity is at record levels, and analysts estimate roughly 16 million new homes will be needed over the next decade, with any sustained move in mortgage rates below 6% serving as a demand catalyst management describes as both a psychological and financial unlock.

Wall Street’s Take on LOW Stock

The Q4 comp beat and three consecutive quarters of positive comparable sales confirm that Lowe’s is taking market share from a still-frozen housing market, setting the stage for operating leverage the moment consumer discretionary spending on big-ticket projects returns.

Lowe’s stock’s normalized EPS came in at $12.28 for fiscal 2025, up 2.4%, and is expected to reach around $13 in 2027 and around $14 in 2028 as the FBM and ADG acquisitions absorb their integration drag and housing activity gradually unfreezes, adding roughly $1 billion in annual productivity savings to the equation.

Twenty-two analysts rate Lowe’s stock a buy or outperform against 13 holds and 1 sell, with a median 12-month price target of $290 implying roughly 20% upside from current levels, as Wall Street waits for mortgage rates to drop sustainably below 6% before calling a full thesis re-rating.

The spread between the $228 low-end target and $325 high-end target reflects a genuine fork around the housing recovery timeline: the lower end embeds continued deferral of big-ticket DIY projects and tariff pressure, while the upper end assumes mortgage rates ease materially in the second half of 2026, triggering a HELOC-driven remodel wave that benefits Lowe’s disproportionately given its DIY customer base.

At roughly 20x forward normalized EPS against a business generating around $1 billion annually in productivity savings and carrying $7.7 billion in free cash flow, Lowe’s stock appears undervalued relative to its own 5-year average forward multiple of 22x to 25x, with the compression entirely explained by housing macro uncertainty rather than any deterioration in the company’s competitive position or cash generation.

Comparable transactions declined 2.3% in Q4, meaning the average ticket is growing but foot traffic is still shrinking; if tariff pressure accelerates and consumers further defer discretionary projects, revenue could miss the low end of the $92 to $94 billion guided range.

Q1 2026 results, expected May 20, will be the first test of whether the 0% to 2% full-year comparable sales guide is tracking or at risk, with the specific number to watch being the gap between average ticket growth (driven by tariff price increases wrapping) and transaction trends (which management expects to improve in the second half).

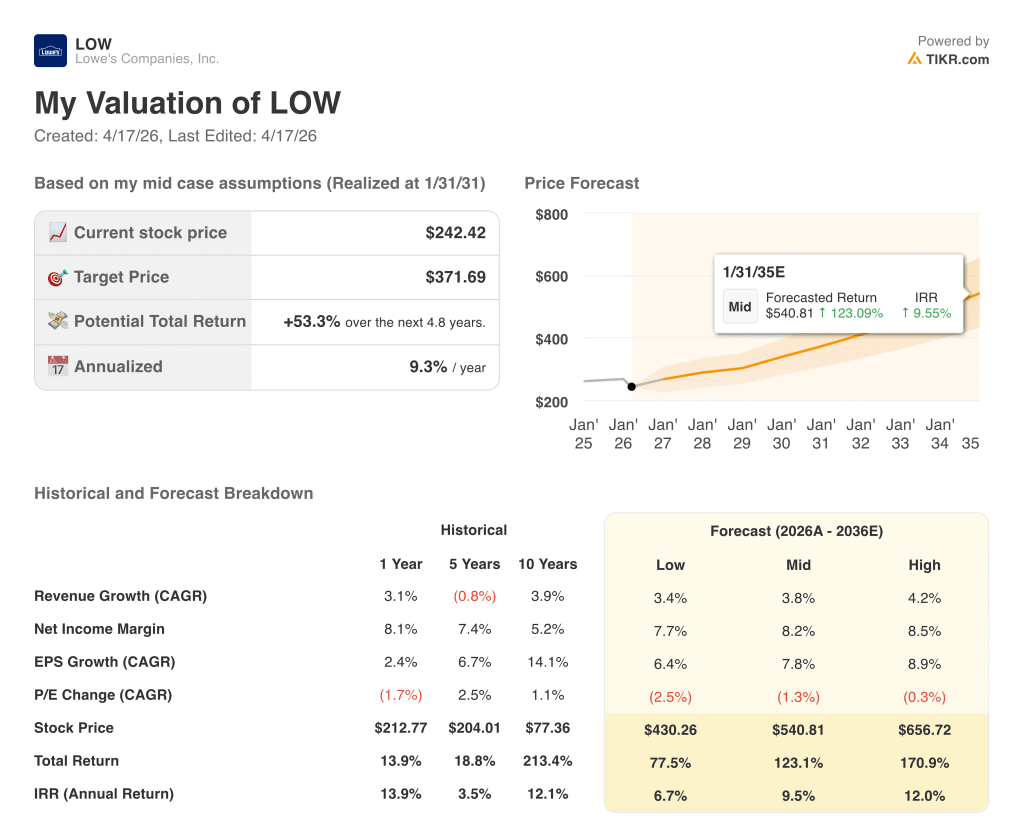

What Does the Valuation Model Say?

The TIKR mid-case assigns a target of around $372 to Lowe’s stock by January 2031, implying a 53% total return over roughly 4.8 years at an annualized rate of around 9%, built on a revenue CAGR of around 4% and EPS compounding at around 8% annually, both well within what the business has demonstrated at comparable points in prior housing cycles.

With EPS Normalized projected to grow from $12.28 in fiscal 2026 toward $15 by 2029, and Lowe’s stock currently trading near 20x forward earnings versus its historical 22x to 25x range, the discount is undervalued and entirely a function of housing cycle timing rather than structural impairment.

The investment case hinges on one variable: the duration of the housing market freeze, and whether Lowe’s can hold margins and continue gaining share while waiting for mortgage rates and housing turnover to normalize.

The Opportunity

- Mortgage rates briefly dipped below 6% in February, and management identified this threshold as the psychological unlock for discretionary DIY remodels; each 50-basis-point cut consensus expects in 2026 moves the housing unlock closer, and any HELOC reactivation flows directly to Lowe’s big-ticket categories

- FBM and ADG are on track to contribute around $8 billion in combined 2026 sales, are already accretive to adjusted EPS, and carry a commercial business (roughly half of FBM revenue) anchored to data center construction that is not dependent on the residential housing cycle

- The Pro Extended Aisle, a direct digital interface to supplier catalogs for planned professional spend, is exceeding all internal expectations and adds a source of revenue growth that is independent of same-store traffic trends

- Lowe’s delivered $1 billion in productivity savings in fiscal 2025 and is targeting the same in 2026 across gross margin improvements from the Lowe’s Media Network and SG&A efficiencies; this cost engine protects earnings even on a flat comparable sales year

The Risk

- Adjusted debt to EBITDA stood at 3.31x at year-end after the FBM acquisition financing, leaving less financial flexibility than Lowe’s carried pre-acquisition; if revenue underperforms the low end of the guided range and interest expense holds near the guided $1.6 billion for 2026, EPS could fall below the $12.25 floor of the adjusted guidance range

- Tariff policy remains fluid by management’s own admission; Lowe’s imports a meaningful portion of its product assortment, and any tariff escalation beyond what is currently embedded in guidance could compress gross margin further on top of the 75-basis-point guided decline in 2026

- Comparable transactions declined 2.3% in Q4 2025, a trend running for multiple years now; if consumer sentiment deteriorates further and big-ticket deferral extends into a fourth year, the housing recovery thesis is not wrong but the wait grows longer and the cost of waiting (lower-multiple compression) grows with it

- Home Depot’s sharper focus on professional contractors and its $18 billion SRS Distribution acquisition give it a structural advantage in the highest-margin segment of the professional market; if Lowe’s Pro Extended Aisle cannot close that gap, share gain estimates in the professional segment may prove optimistic

Should You Invest in Lowe’s Companies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LOW stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lowe’s Companies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LOW stock on TIKR for Free →