Key Stats for Booking Holdings Stock

- 52-Week Range: $151 to $234

- Current Price: $186

- Street Mean Target: $233

- Street High Target: $310

- TIKR Model Target (Dec. 2030): $379

What Happened?

Booking Holdings (BKNG), the world’s largest online travel platform operating Booking.com, Agoda, Kayak, and OpenTable across more than 200 countries, has shed roughly 20% year to date even as the underlying business delivered some of the strongest results in its history.

The Q4 2025 earnings beat was comprehensive: adjusted EPS of $48.80 on a pre-split basis topped the $48.47 analyst consensus, room nights grew 9% year over year to 285 million, and revenue of $6.35 billion cleared the $6.13 billion estimate.

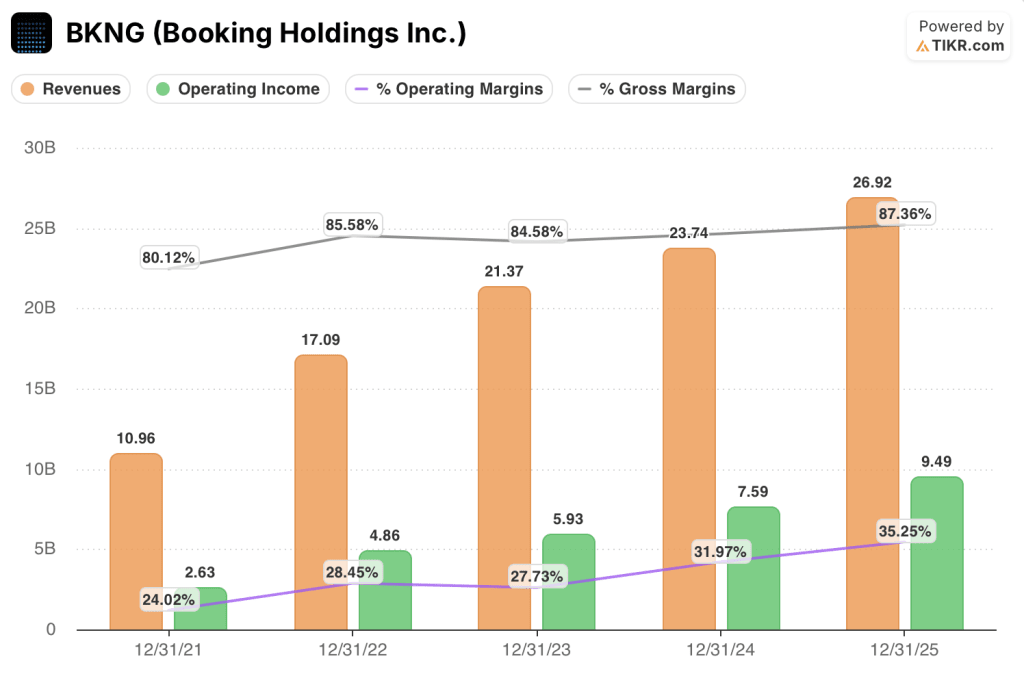

For the full year, Booking Holdings generated $26.92 billion in revenue (up 13%), $9.9 billion in adjusted EBITDA (up 20%), and $9.1 billion in free cash flow (up 15%), lifting EBITDA margins to 36.9%, a level that makes Booking Holdings one of the most profitable large-cap internet companies in the world.

Ewout Steenbergen, CFO and EVP, stated on the Q4 2025 earnings call that “our absolute number in terms of customer service costs are down and our bookings are up approximately 10%,” pointing to generative AI already producing measurable efficiency gains visible in a specific income statement line, not a future promise.

The disconnect between results and stock price traces almost entirely to investor anxiety over AI disintermediation: the fear that large language models like ChatGPT will eventually bypass OTAs (online travel agencies) and book travel directly with hotels, cutting Booking Holdings out of the transaction entirely.

Management’s rebuttal has been direct and data-grounded: at the Morgan Stanley TMT Conference on March 3, Steenbergen demonstrated live that asking a major LLM to process a flight cancellation produced the response that the platform was “not an airline agent” and could not issue refunds, illustrating that payments complexity, multilingual customer service, and 4.4 million supplier relationships create barriers that language models are structurally unlikely to replicate.

The company’s strategic flywheel kept compounding throughout the uncertainty: Connected Trip transactions (bookings where a customer books multiple travel verticals together) grew in the high-20% range in 2025, airline tickets reached 68 million (up 37%), and Genius loyalty program Level 2 and 3 travelers now represent a high-50% share of room nights.

With $21.8 billion in remaining share buyback authorization, a 9.4% dividend increase to $10.50 per share, and 2026 guidance for around 9% constant-currency top-line growth (about 100 basis points above the company’s long-term target), the capital return and growth profile has strengthened while Booking Holdings stock has moved sharply in the other direction.

Wall Street’s Take on BKNG Stock

The AI-disruption narrative has done something unusual to Booking Holdings stock: it has compressed the forward earnings multiple for a structurally advantaged, capital-light compounder to levels that price in the worst outcome as near-certain.

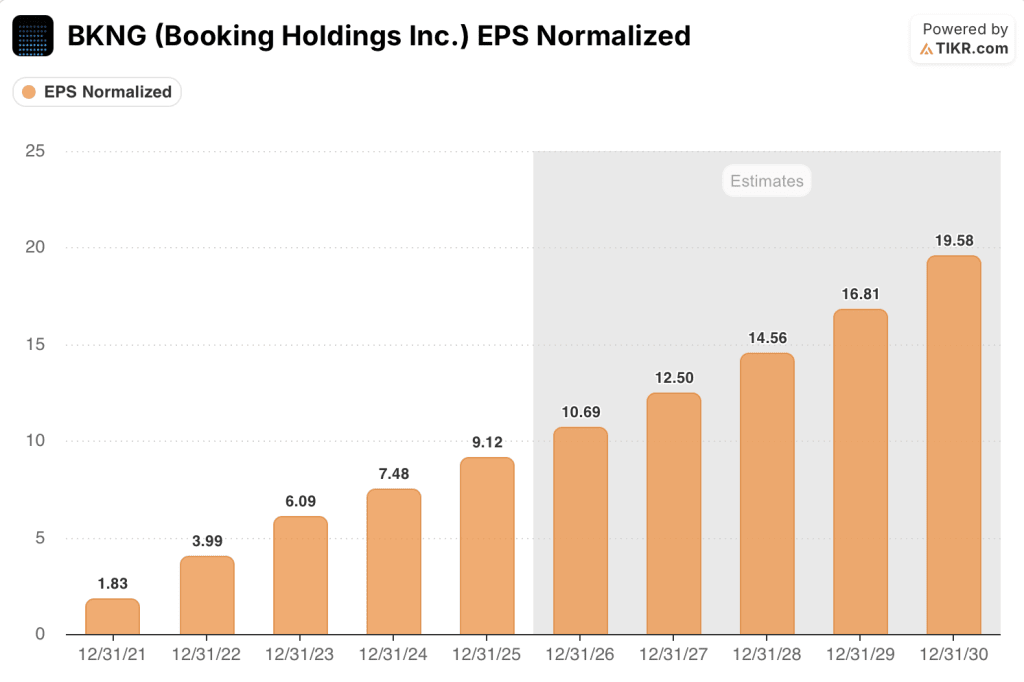

BKNG’s normalized EPS grew 21.9% in 2025 to $9.12 on a post-split basis, and consensus estimates project growth of around 17% in both 2026 (to roughly $11) and 2027 (to roughly $13), growth supported by the Transformation Program’s $500-550 million in expected in-year 2026 savings and the $700 million reinvestment program already deployed into GenAI, Asia expansion, Connected Trip development, and U.S. market share capture.

Twenty-five analysts rate Booking Holdings stock a buy, six rate it outperform, and eight rate it hold, with a mean price target of $232.65 implying around 25% upside from the current price; Wall Street is focused on April 28, when Q1 2026 earnings will confirm whether the company’s early-year momentum is tracking the guided 14-16% gross bookings growth.

The spread between the $310 high target and $180 low target captures a live debate: bulls price in BKNG as an AI beneficiary that monetizes top-of-funnel LLM traffic while protecting its direct booking channel, while bears price in margin pressure from elevated performance marketing spend and a slower-than-expected U.S. consumer environment.

Priced at roughly 17x 2026 consensus EPS against a normalized earnings growth rate of around 17% and a historical forward P/E that averaged well above 25x over the prior five years, Booking Holdings stock appears undervalued at a time when the business is generating more free cash flow, more room nights, and more direct bookings than at any point in its history.

If AI platforms succeed in capturing travel booking intent and converting it without returning traffic to the OTA layer, the direct booking mix that management has spent years building could plateau, and the case for multiple re-expansion weakens materially.

The April 28 Q1 2026 earnings release is the next inflection point: room night growth (guided at 5-7%) hitting the high end of the range, and continued improvement in the U.S. direct channel, are the two numbers that confirm whether the AI risk is priced correctly or not.

Booking Holdings Stock Financials

Booking Holdings generated $26.92 billion in revenue in 2025, a 13.4% year-over-year increase and the fourth consecutive year of double-digit revenue growth since the post-pandemic recovery began from a base of $10.96 billion in 2021.

Operating income reached $9.49 billion in 2025, up 25.0% year over year, driven by the Transformation Program’s cost restructuring and the generative AI efficiencies in customer service that Steenbergen cited on the earnings call as producing roughly 10% lower cost per booking.

The operating leverage trajectory in Booking Holdings’ income statement is structurally clean: operating margins expanded from 24.0% in 2021 to 28.4% in 2022, then 27.7% in 2023, 32.0% in 2024, and 35.2% in 2025, a more than 1,100-basis-point expansion over four years as the platform scaled faster than its cost base.

Gross margins reached 87.4% in 2025 from 80.1% in 2021, reflecting the shift toward higher-margin merchant payment transactions and the scale benefits of a platform that processed $186 billion in annual gross bookings last year.

What Does the Valuation Model Say?

TIKR’s mid-case model assigns a price target of around $379 per share to BKNG, implying around 104% upside from the current $185.69 and a 16% annualized return to the end of 2030, anchored by a revenue CAGR of around 8% and a net income margin rising toward around 32% as Transformation Program savings compound and the $700 million reinvestment program generates its guided $400 million in incremental revenue.

Running at roughly 17x 2026 consensus EPS against normalized EPS growth of around 17% and a historical forward multiple well above 25x, the evidence points clearly: Booking Holdings stock is undervalued by a margin that reflects narrative-driven fear rather than a deterioration in the business model.

The AI disintermediation debate is the entire swing factor in this investment case.

What Has to Go Right

- Q1 2026 room night growth hits the high end of the 5-7% guidance range, confirming global travel demand has absorbed the Middle East conflict without lasting damage to BKNG’s international mix

- U.S. direct channel growth, which accelerated from mid-2025 onward, continues to improve, validating that Genius loyalty program investment and brand spend are building durable, non-paid customer relationships at meaningful scale

- Connected Trip transaction growth sustains its high-20% pace in 2026, expanding revenue per customer and reducing structural dependence on any single acquisition channel, including traditional paid search

- The Transformation Program delivers $500-550 million in 2026 in-year savings on schedule, funding the $700 million reinvestment program and still expanding EBITDA margins by the guided approximately 50 basis points

What Could Go Wrong

- A major LLM platform builds sufficient fulfillment capability (payments processing, cancellation workflows, multilingual customer service) to convert meaningful travel bookings without handing traffic back to Booking Holdings, reducing the roughly two-thirds direct B2C booking mix that anchors the bull case

- The Middle East ceasefire announced in early April breaks down, suppressing international travel volumes in BKNG’s highest-margin routes and forcing a guidance cut on April 28 that resets the earnings growth trajectory

- Marketing deleverage accelerates beyond the opportunistic spend management described, particularly if U.S. customer acquisition costs rise faster than direct channel growth can offset, compressing EBITDA margins and removing the case for multiple expansion

- Top-line revenue growth decelerates toward the low end of the 2027-2028 consensus range (around 8%) as post-pandemic travel normalization fully plays out, making the current 17x forward P/E feel less discounted if the growth premium disappears

Should You Invest in Booking Holdings Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BKNG stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Booking Holdings Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BKNG stock on TIKR for Free →