Key Stats for Western Digital Stock

- 52-Week Range: $36 to $366

- Current Price: $365

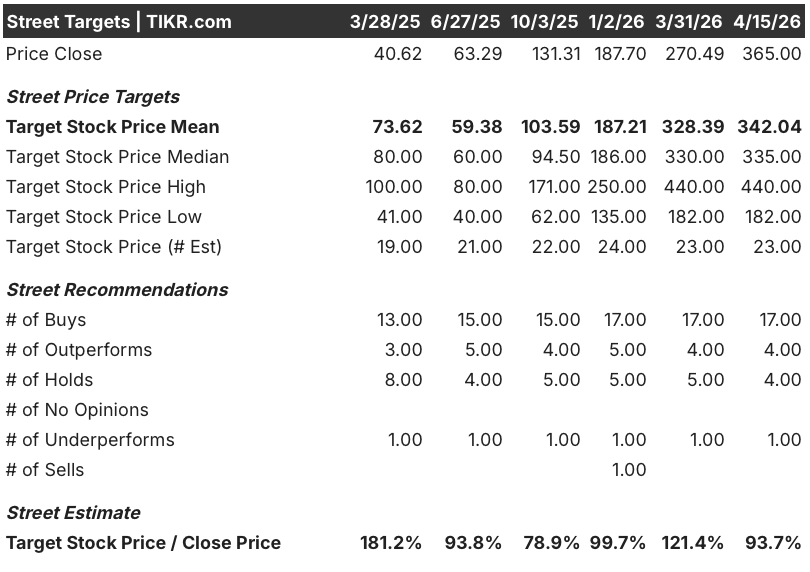

- Street Mean Target: $342

- Street High Target: $440

- TIKR Model Target (Dec. 2030): $797

What Happened?

Western Digital stock (WDC), issued by one of only two major producers of enterprise hard disk drives for hyperscale data centers, has run from $35.51 to $365 in the past year as the business transforms from a cyclical storage supplier into an AI infrastructure compounder.

The January 30 Q2 FY26 earnings report confirmed the inflection: revenue reached $3.02 billion, up 25% year over year, and non-GAAP EPS of $2.13 came in 78% above the year-ago period, beating the high end of the company’s own guidance.

Gross margin hit 46.1% in Q2, up 770 basis points year over year, driven by a shift toward higher-capacity nearline drives and rapid adoption of UltraSMR, a software-defined capacity technology that delivers 20% more storage density per drive without adding hardware cost.

Kris Sennesael, Chief Financial Officer, stated on the Q2 2026 earnings call that “both revenue and EPS were above the high end of the guidance range,” and guided Q3 FY26 revenue of approximately $3.2 billion at around 40% year-over-year growth, with gross margin expanding to 47% to 48%.

At its February 3 Innovation Day in New York, WD unveiled a roadmap spanning 40TB ePMR drives already in customer qualification, two HAMR drive qualifications started in Q1 of this year, and a path to 100TB drives by 2029, alongside long-term financial targets of greater than $20 EPS, greater than 50% gross margins, and greater than 40% operating margins.

The board authorized an additional $4 billion in share repurchases on February 3, while the company simultaneously sold its $3.17 billion Sandisk stake to retire debt and move toward a net-positive cash position, completing a balance sheet transformation that began with the SanDisk spinoff.

Wall Street’s Take on WDC Stock

The Q2 beat and Q3 guidance reset the forward earnings trajectory, but the more durable shift is the structural change in how hyperscalers now contract with WDC: the company holds firm purchase orders with its top seven customers through calendar 2026 and long-term agreements with three of its top five customers extending through 2027 and 2028.

WDC’s normalized EPS is expected to reach approximately $9 in FY26, up roughly 81% from $5 in FY25, and compound further to $13.82 in FY27, as the pure-play HDD business model delivers per-share growth at a rate the market has not yet fully priced into the multiple.

That earnings acceleration is margin-driven, not volume-driven: EBITDA is expected to expand from 29% margins in FY25 to roughly 43% in FY27, powered by UltraSMR mix gains now above 50% of nearline exabytes and the roughly 10% annual cost-per-terabyte reduction Sennesael confirmed is running through the model.

The Q2 beat and Q3 guidance reset the forward earnings trajectory, but the more durable shift is the structural change in how hyperscalers now contract with WDC: the company holds firm purchase orders with its top seven customers through calendar 2026 and long-term agreements with three of its top five customers extending through 2027 and 2028.

WDC’s EBITDA is expected to reach approximately $4.67 billion in FY26 at around 37% margins, expanding to approximately $6.73 billion in FY27 at roughly 43% margins, as the mix shift toward higher-capacity drives and UltraSMR adoption removes cost per terabyte faster than revenue growth adds it.

Of 26 analysts covering WDC, 21 rate it a buy or outperform, 4 hold, and 1 underperforms, with a mean price target of $342 and the Street high at $440, suggesting analysts are broadly waiting for the HAMR ramp and 40TB volume qualification to confirm the margin expansion trajectory holds into FY27.

The spread between the $182 Street low target and the $440 Street high reflects a genuine debate: bears model a softer HDD pricing environment in 2027 to 2028 as areal density improvements add supply without requiring new unit capacity, while bulls price in a structural demand floor anchored by multi-year hyperscaler LTAs and inference-driven data storage growth.

Priced at roughly 41x trailing normalized EPS against a FY26 consensus estimate of approximately $8.93 per share, Western Digital stock appears undervalued relative to the earnings inflection already in progress, with EPS expected to compound at roughly 55% in FY27 as structural margin expansion makes the P/E compression case compelling for a business the market is still treating as cyclical.

Bernstein’s upgrade to “outperform” in early April, citing demand and pricing tracking better than expected for AI storage, reinforced the view that the Google TurboQuant algorithm selloff was a sector mismatch rather than a genuine demand risk for HDDs.

A meaningful supply-side response to the current HDD shortage, whether from WDC itself or Seagate, would test the stable pricing environment management has guided beyond CY26.

The binary near-term event is the Q3 FY26 earnings report on April 30: investors should watch whether gross margin prints at the high end of the 47% to 48% guide, which would confirm UltraSMR mix is tracking above plan ahead of the HAMR ramp.

Western Digital Stock Financials

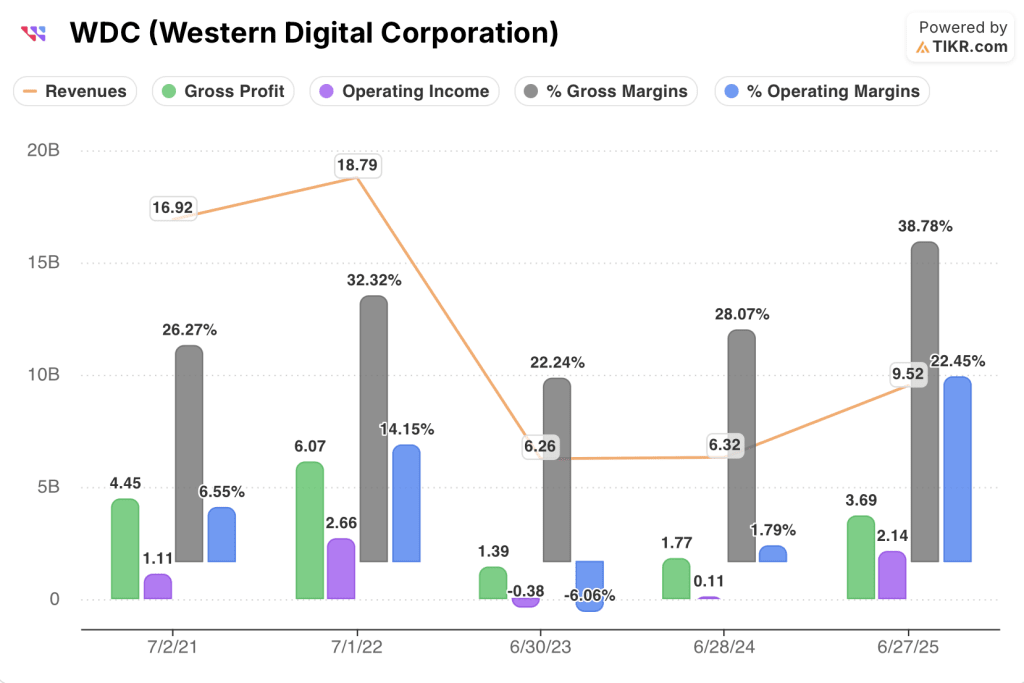

Western Digital’s revenue recovered to $9.52 billion in fiscal 2025, up 50.7% year over year, reversing a collapse from $18.79 billion in fiscal 2022 to $6.26 billion in fiscal 2023 as the post-pandemic storage downcycle ran its course.

The more significant development is margin structure: gross profit jumped 108% in fiscal 2025, lifting gross margins from 28% to 39%, as the exit from the flash business eliminated the segment drag that suppressed consolidated margins through the downcycle.

Operating income reached $2.14 billion in fiscal 2025 at a 22.4% operating margin, compared to just $110 million and a 1.8% margin in fiscal 2024, a recovery the LTM figures extend further with operating income at $3.01 billion and operating margins at 28%.

The cost structure has reset well below prior peak: total operating expenses fell from $3.41 billion in fiscal 2022 to $1.56 billion in fiscal 2025 as the SanDisk separation removed flash R&D and SG&A, creating operating leverage that now amplifies each incremental revenue dollar directly into the margin line.

What Does the Valuation Model Say?

The TIKR mid-case model targets around $797 per share by mid-2030, built on a revenue CAGR of approximately 16% and net income margins expanding toward 34%, reflecting the operating leverage of a pure-play HDD business where incremental gross margins are running at roughly 75%, as CFO Kris Sennesael confirmed on the Q2 earnings call.

Against $365 today, that mid-case path represents roughly 119% upside at an 18% annual return, and with the high case pointing toward around $2,023, Western Digital stock is undervalued: consensus already prices in approximately $8.93 in FY26 EPS compounding to approximately $13.82 in FY27, on a business now insulated by multi-year hyperscaler purchase agreements the market has not yet fully re-rated.

The entire argument hinges on one question: whether WDC’s pricing discipline and technology execution hold simultaneously through the HAMR transition and the 40TB ePMR ramp over the next 18 months.

What Has to Go Right

- HAMR qualification with two hyperscale customers, started in Q1 CY26, must ramp to volume production in H1 CY27 at neutral to accretive gross margins, as management has explicitly guided

- UltraSMR mix must continue expanding past the current greater-than-50% share of nearline exabytes, sustaining the roughly 10% annual cost-per-terabyte reduction that is the engine of margin expansion

- 40TB ePMR drives currently in qualification at two hyperscalers must reach volume shipment in H2 CY26, unlocking a 75% exabyte uplift versus the 23TB average capacity shipped in Q2 FY26

- ASP per terabyte must deliver mid- to high-single-digit annual increases across all four quarters of CY26, supported by LTA pricing terms already contracted with the top five customers

- Reaching greater than $20 EPS requires the business to achieve greater than 50% gross margins and greater than 40% operating margins by FY28 to FY29 on the current technology trajectory

What Could Go Wrong

- A faster-than-expected areal density ramp industry-wide could add HDD supply ahead of demand, pressuring the stable pricing environment WDC has guided for beyond CY26 from a higher base

- The $1.6 billion convertible note, callable in November 2026 and maturing in 2028, introduces execution risk in the equity-for-equity monetization of the remaining 1.7 million Sandisk shares

- Inference workloads currently backed by HDD object stores could migrate toward QLC NAND if NAND pricing collapses and the SAE interface throughput bottleneck is resolved at the software layer

- Google’s TurboQuant compression algorithm signals that hyperscalers are actively engineering around storage requirements at the model architecture level, a structural overhang Bernstein dismissed but the market has not fully priced

Should You Invest in Western Digital Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WDC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Western Digital Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WDC stock on TIKR for Free →