Key Stats for Palo Alto Stock

- 52-Week Range: $140 to $224

- Current Price: $164

- Street Mean Target: 206

- Street High Target: $265

- TIKR Model Target (Dec. 2030): $266

What Happened?

Palo Alto Networks (PANW), the cybersecurity platform provider racing to become the operating system for enterprise AI security, has dropped 17% year to date even as its revenue trajectory accelerated sharply upward.

The company reported fiscal Q2 revenue of $2.59 billion, up 15% year over year, and then raised its full-year revenue forecast to $11.28 billion to $11.31 billion, a $780 million jump above its prior midpoint guidance.

The stock’s decline is not a revenue story: it traces directly to the EPS guidance cut from $3.80 to $3.90 down to $3.65 to $3.70, driven by $4.9 billion in combined cash outlays for two landmark acquisitions closed in rapid succession.

Additionally, Palo Alto completed its $25 billion acquisition of CyberArk, the identity security specialist focused on protecting privileged user and machine access, in February, followed immediately by the $3.35 billion close of Chronosphere, a cloud-native observability platform used by AI-native companies to monitor system health at scale.

The company’s platformization count, measuring how many customers have consolidated multiple security functions onto Palo Alto’s unified architecture, reached approximately 1,550, up 35%, with a record 110 net new platformizations in Q2 alone.

CEO Nikesh Arora stated on the Q2 2026 earnings call that “We are now the only company that can verify the who has secure the what simultaneously,” framing the CyberArk integration as a structural moat precisely as AI agents begin generating machine-speed login events at enterprise scale.

Palo Alto also completed the acquisition of Koi on April 14, a startup specializing in securing AI agents and MCP servers (software connectors that let AI models interact with external tools) operating at the endpoint, extending its AI security perimeter to cover the exact attack surface enterprises are generating fastest.

Wall Street’s Take on PANW Stock

The acquisition costs that punished Palo Alto Networks stock in 2026 are not a business deterioration story; they are a transformation spend story, and the FCF profile is what separates the two.

Palo Alto stock’s FCF reached $3.47 billion in FY25, and consensus estimates it reaching $4.13 billion in FY26 and $5.05 billion in FY27, representing 19% and 22% year-over-year growth, respectively, driven by the platform cross-sell engine that CyberArk and Chronosphere are designed to accelerate.

Forty-five of 49 analysts covering Palo Alto Networks stock rate it a Buy or Outperform, with a mean price target of $205.96 and a high of $265, reflecting 25% to 62% upside from the current $164.11 price; the consensus is waiting for CyberArk integration milestones to start converting pipeline into joint-platform ARR.

The spread from $114 at the low to $265 at the high encodes a real debate: the bears believe the integration complexity at $25 billion scale will compress margins for longer than guided, while the bulls believe a company governing human, machine, and AI agent identity simultaneously is an entirely new category.

Priced at roughly 26x FY27 free cash flow against 22% FCF growth and a platform net revenue retention rate of 119%, Palo Alto Networks stock appears undervalued, with the market pricing dilution risk while the cash generation machine compounds in the background.

CEO Arora’s $10 million open-market share purchase at approximately $147 per share in late March is not a narrative claim; it is a capital allocation decision made by the person with the most complete view of the integration pipeline.

If the CyberArk go-to-market integration stalls and joint ARR does not materialize in H2 FY26, the diluted share count from the 112 million shares issued keeps EPS growth below double digits for two consecutive years and the thesis breaks.

Q3 FY26 earnings are the first full-quarter read on combined CyberArk and Chronosphere revenue contribution; watch whether the $340 million inorganic revenue guided for Q3 flows through on pace and whether platformization net new additions hold above 100.

Palo Alto Stock Financials

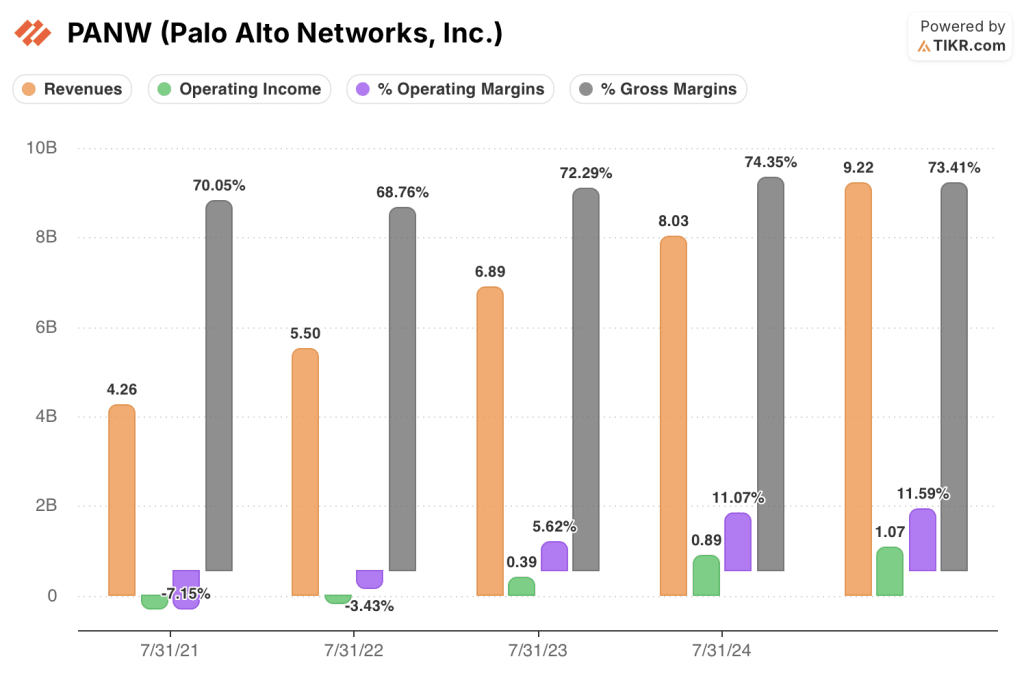

Palo Alto Networks grew revenue from $8.03 billion in FY24 to $9.22 billion in FY25, a 14.9% increase, while operating income expanded from $0.89 billion to $1.07 billion, pushing operating margins from 11.1% to 11.6%.

The margin expansion traces directly to the platformization flywheel: gross margins held at 73.4% in FY25 even as COGS grew, because the shift toward higher-margin SaaS subscription products within the network security segment outpaced hardware revenue growth.

Palo Alto stock’s operating margin trajectory over five years tells a clear direction, moving from (7.1%) in FY21 to (3.4%) in FY22 to 5.6% in FY23 to 11.1% in FY24 to 11.6% in FY25, with each year’s improvement driven by subscription gross margin leverage compounding faster than SG&A and R&D investment growth.

The near-term tension is real: acquisition-related integration costs and the absorption of CyberArk’s cost base will likely compress reported operating margins in FY26 before cross-sell revenue synergies flow through, which is precisely why the income statement alone understates the investment case for a company generating 37% FCF margins.

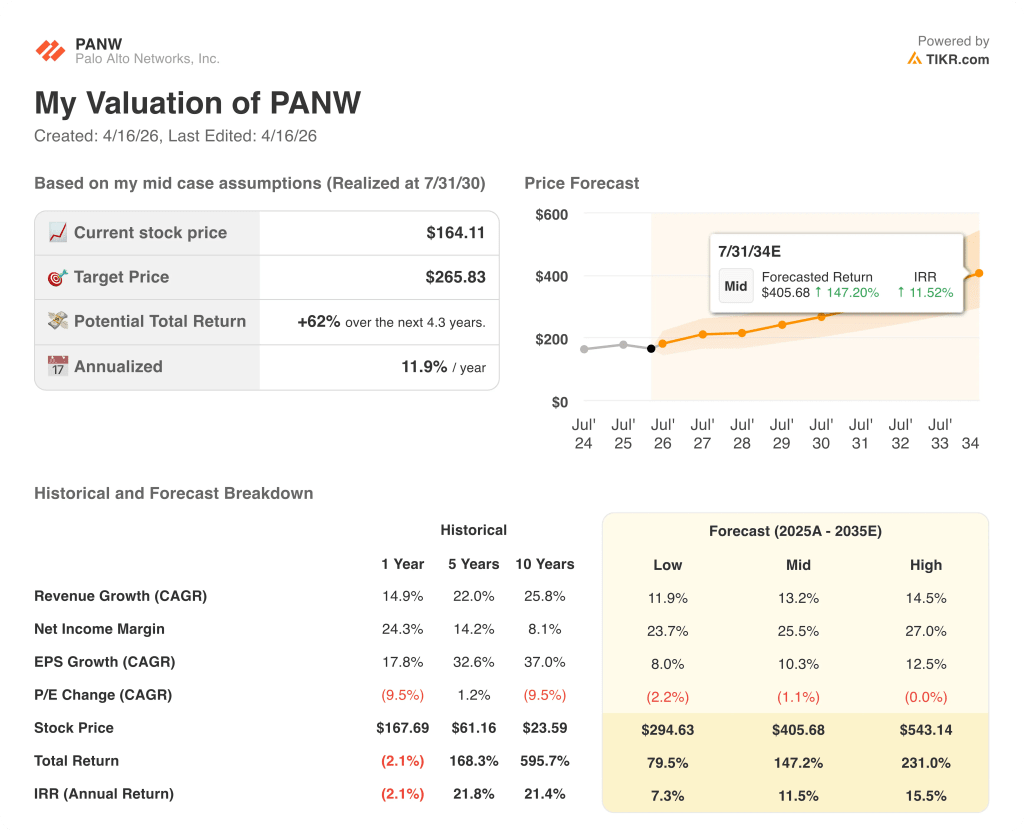

What Does the Valuation Model Say?

TIKR’s mid-case model assigns Palo Alto stock a price target of $266, implying a 62% total return over approximately 4.3 years, built on a revenue CAGR assumption of around 13% and a net income margin expanding toward 26%, both grounded in the cross-sell pipeline that CyberArk and Chronosphere bring to 65,000-plus existing firewall customers.

With FCF growing toward $5 billion and the stock trading at roughly 26x FY27 free cash flow, Palo Alto Networks stock appears undervalued at a moment when the market is pricing short-term EPS dilution rather than long-term platform cash generation.

The central tension is whether a company absorbing three major acquisitions in under twelve months can maintain platformization velocity while integrating 4,000-plus new employees and two entirely different ARR definitions.

What Has to Go Right

- Platformization net new additions must sustain above 100 per quarter, confirming the cross-sell engine is not distracted by integration workload; Palo Alto stock hit a record 110 in Q2 against exactly that threshold.

- CyberArk’s $1.2 billion ARR base must begin converting into joint Palo Alto platform deals, with management confirming initial joint pipeline is already forming as of the Q2 call.

- Chronosphere’s $200 million ARR must scale inside PANW’s enterprise go-to-market; the 9-figure expansion deal with a leading AI model provider signed in Q2 confirms the unit economics exist at the high end of the market.

- SASE, the secure access service edge product delivering network security from the cloud, must sustain above 40% growth; its $1.5 billion ARR milestone in Q2 confirms the velocity is real.

What Could Go Wrong

- The 112 million shares issued for CyberArk plus ongoing integration costs keep normalized EPS below $4 through FY27, extending the multiple compression window for earnings-focused investors.

- China’s national security ban on Palo Alto software across government and enterprise accounts creates a revenue ceiling on PANW’s Asia-Pacific expansion at precisely the moment AI factory buildouts are accelerating in that region.

- If frontier AI models deliver automated offensive capabilities faster than PANW’s platform can counter, the market-speed threat response differentiating Cortex XSIAM erodes and removes the pricing premium the platform commands over point-product alternatives.

- Integration complexity at the $25 billion CyberArk scale, which management acknowledged requires more reengineering than prior deals, could redirect engineering resources away from the Prisma AIRS and AgentiX roadmap at the exact moment AI security adoption is inflecting.

Should You Invest in Palo Alto Networks, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PANW stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Palo Alto Networks, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PANW stock on TIKR for Free →