Key Stats for DoorDash Stock

- 52-Week Range: $143 to $286

- Current Price: $180

- Street Mean Target: $152

- Street High Target: $340

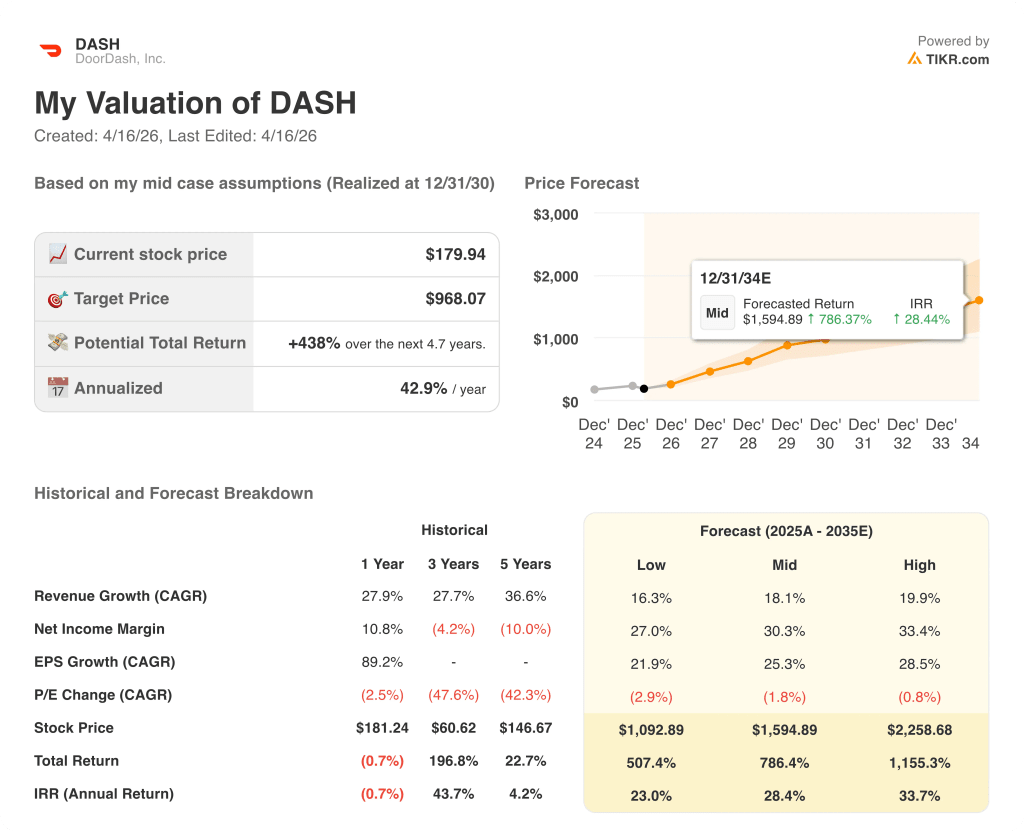

- TIKR Model Target (Dec. 2030): $968

What Happened?

DoorDash (DASH), the dominant U.S. on-demand delivery platform that connects consumers with restaurants, grocery stores, and retailers, reported its two fastest-growing U.S. quarters in four years in 2025 while simultaneously expanding into a global local commerce operating system.

Q4 2025 marketplace gross order value (GOV, the total dollar value of all orders placed on the platform) surged 39% year over year to $29.68 billion, beating the $27.65 billion consensus estimate by more than $2 billion.

Total orders grew 32% to 903 million in the quarter, and DoorDash ended 2025 with over 56 million monthly active users and more than 35 million members across its DashPass, Wolt+, and Deliveroo Plus subscription programs.

The Deliveroo acquisition (DoorDash’s 2025 purchase of the UK-based food delivery platform for approximately 2.9 billion pounds) is already outperforming: Q4 Deliveroo EBITDA contribution slightly exceeded the $45 million target set before the deal closed.

DoorDash co-founder, Chair and CEO Tony Xu stated on the Q4 2025 earnings call that “beyond restaurants, the US grocery and retail categories showed strength, with DASH attracting more new consumers in 4Q25 than in any prior quarter,” and the company confirmed it became the leading third-party marketplace in the U.S. by grocery and retail order volume as of December 2025.

The platform is investing several hundred million dollars in 2026 to merge its DoorDash, Wolt, and Deliveroo brands onto a single global tech stack, a unification that will accelerate feature velocity and reduce operational redundancy across the three platforms, with management expecting Deliveroo to contribute $200 million in adjusted EBITDA for the full year.

Autonomous delivery is advancing in parallel: DoorDash expanded its Wing drone partnership to metro Atlanta in April, invested $200 million in Rivian spinoff Also (a startup building small electric delivery vehicles) in a Series C round, and Barclays estimates autonomous delivery could unlock a $16 billion annual global profit pool for food delivery platforms as penetration scales toward roughly 10% by 2035.

Wall Street’s Take on DASH Stock

The Q4 earnings report repriced DoorDash stock on a near-term EBITDA guidance miss, but the structural story underneath is a platform on the verge of a free cash flow inflection that the headline numbers obscure.

DASH generated $1.83 billion in free cash flow in 2025 (FCF margins of 13.3%), and consensus estimates project that figure to nearly double to $3.22 billion in 2026 as the Deliveroo integration matures, tech replatform costs normalize, and grocery and retail unit economics turn positive in the second half of the year.

Thirty-six analysts carry buy or outperform ratings on DoorDash stock against nine holds and zero sells, with a mean price target of $252 implying roughly 40% upside from current levels; the specific catalyst Wall Street is watching is Deliveroo’s ramp toward the $200 million full-year EBITDA target confirmed on the earnings call.

The spread between the $185 low target and $340 high target reflects a genuine debate: bears see the 2026 EBITDA investment cycle as a structural margin problem, while bulls price in a global platform routing Wolt, DoorDash, and Deliveroo orders through one unified system by late 2026, unlocking scale that no single-geography competitor can replicate.

Trading at roughly 56x 2026 consensus FCF against a forward growth rate that nearly doubles free cash flow year over year, DoorDash stock appears undervalued given that the multiple compresses rapidly to under 25x 2027 FCF as the investment cycle rolls off and Deliveroo contributions accelerate.

Xu even stated on the Q4 2025 earnings call that “we are effectively building the operating system for local commerce,” a framing that redefines DASH’s addressable market well beyond food delivery into software, fulfillment services, autonomous vehicles, and advertising.

If the global tech unification slips into 2027 or Deliveroo’s $200 million EBITDA contribution disappoints, the near-term FCF recovery thesis breaks and the stock’s multiple has no floor at current levels.

Q1 2026 results, due May 6, are the first confirmation point: watch whether GOV hits the $31.0 to $31.8 billion guided range and whether Deliveroo EBITDA tracks toward the $25 million Q1 floor management cited.

DoorDash Stock Financials

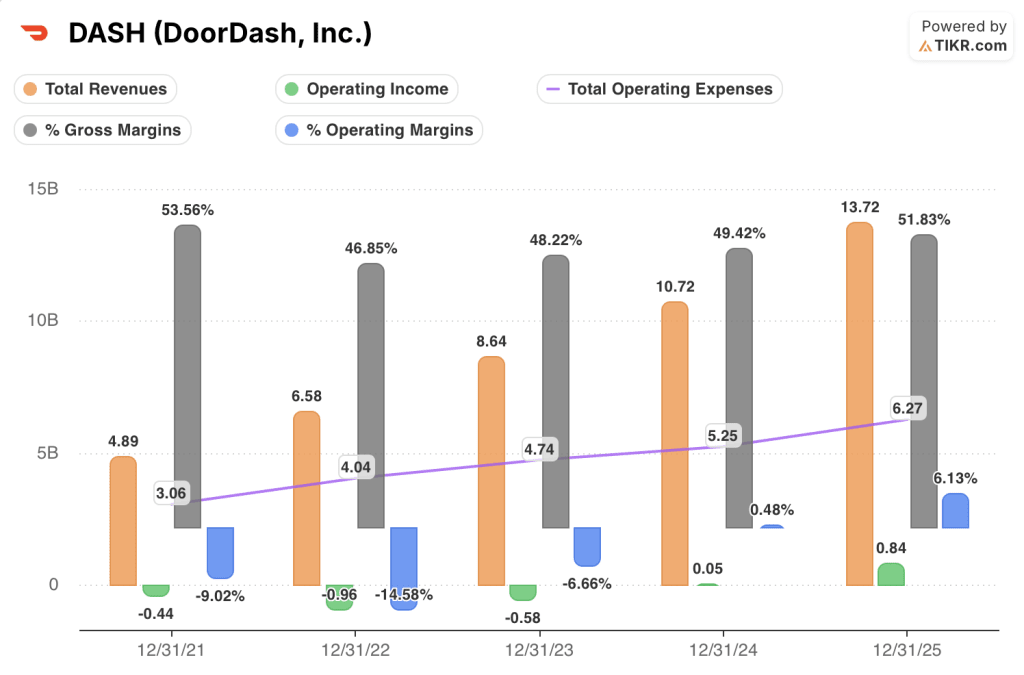

DoorDash grew total revenue from $4.89 billion in 2021 to $13.72 billion in 2025, a compound trajectory that absorbed the full cost of the Wolt acquisition and Deliveroo integration within the same five-year window.

The more important story is operating leverage: operating income flipped from a loss of $0.96 billion in 2022 to a profit of $0.84 billion in 2025 as SG&A and R&D scaled more slowly than revenue, confirming that the platform model generates margin expansion as order density increases.

Gross margins dipped from 53.6% in 2021 to 46.8% in 2022 before recovering to 51.8% in 2025, with the recovery driven by mix improvement as higher-margin restaurant orders grew alongside Wolt’s more favorable cost structure in international markets.

Total operating expenses grew from $3.06 billion in 2021 to $6.27 billion in 2025, a trajectory that now includes the 2026 tech re-platform investment and signals that operating margins at 6.1% still carry limited cushion if top-line growth decelerates.

What Does the Valuation Model Say?

TIKR’s mid-case model targets $968 per share by December 2030, built on an 18% revenue CAGR and net income margins expanding to 30%, assumptions grounded directly in the Deliveroo integration ramp, grocery and retail unit economics turning positive, and global tech stack unification driving operating leverage.

With free cash flow on track to nearly double in 2026 and the platform expanding into autonomous delivery, advertising, and merchant software, DoorDash stock is deeply undervalued at a price that implies the market expects the investment cycle to persist indefinitely rather than normalize.

The entire case rests on whether the 2026 investment cycle is a one-time setup cost for a global platform or the beginning of a structural margin cap as DoorDash competes in markets with higher regulatory and labor costs than the U.S.

What Has to Go Right

- Deliveroo delivers its $200 million full-year EBITDA target and demonstrates accelerating order growth, validating the $2.9 billion acquisition price paid in 2025

- Global tech stack unification completes in 2026, collapsing the cost of running three parallel platforms and accelerating feature velocity across all 40+ geographies

- Grocery and retail unit economics turn gross profit positive in the second half of 2026, as CFO Ravi Inukonda confirmed on the Q4 2025 earnings call

- FCF expands toward the $3.22 billion 2026 consensus estimate, nearly doubling from $1.83 billion in 2025 and compressing the forward FCF multiple to under 25x 2027

- Autonomous delivery scales beyond pilot markets, with Barclays projecting the category reaches roughly 10% penetration by 2035 and unlocks a $16 billion annual global profit pool for platforms already at scale

What Could Go Wrong

- Q1 2026 EBITDA comes in below the $675 million to $775 million guided range, confirming the investment cycle is heavier than disclosed and triggering estimate cuts across the full year

- Deliveroo’s Italian labor probe escalates to a material financial liability after Milan prosecutors placed Deliveroo Italy under judicial supervision in February over alleged exploitation of approximately 20,000 riders

- NYC and Seattle-style regulatory actions spread to additional U.S. cities, adding per-order cost through minimum pay mandates (NYC raised fees up to $0.50 per order in April to offset the $22.13 per hour Dasher minimum)

- DashPass growth decelerates as cost-of-living pressure reduces subscription spend, cutting the cohort that drives the highest order frequency and gross profit per user

- Tech replatform costs bleed into 2027 at a scale larger than the “smaller component” management characterized on the Q4 call, delaying the FCF inflection by 12 to 18 months

Should You Invest in DoorDash, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DASH stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DoorDash, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DASH stock on TIKR for Free →