Key Stats for Oracle Stock

- Current Price: $170.77

- Target Price (Mid): ~$55

- Street Target: ~$244

- Potential Total Return: ~242%

- Annualized IRR: ~35% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

After weeks of grinding below $150, Oracle (ORCL) stock became the best-performing name in the S&P 500 on April 13, surging over 11% in a single session before adding another 5% the following day.

The two-session move pushed ORCL up roughly 17% from its recent range, recovering a meaningful slice of the 58.43% drawdown that had taken shares from a 52-week high of $345.72 down to a low of $121.24.

Two catalysts drove the move.

Oracle topped the S&P 500 after announcing AI-focused upgrades to its utilities software suite, targeting billing automation, grid operations, and asset management for electric, gas, and water utilities.

The next day brought a larger headline: Oracle agreed to purchase up to 2.8 gigawatts of fuel cell power from Bloom Energy, expanding an existing partnership, with 1.2 gigawatts already under contract and deployment underway.

Oracle surged 5.13% on the Bloom announcement, outperforming the broader tech sector’s 1.7% gain that session.

Both deals follow a strong Q3 FY26 earnings report on March 10 that sent the stock up 9.18% in a single day.

On the Q3 earnings call, Principal Financial Officer Doug Kehring told analysts: “Q3 being the first quarter in over 15 years where both organic total revenue and organic non-GAAP EPS grew at 20% or better in USD.”

Total revenue reached $17.2 billion, up 22% year over year. Cloud infrastructure revenue hit $4.9 billion, up 84%. Total cloud revenue came in at $8.9 billion, up 44%.

Bulls see a company booking contracted revenue at a pace no enterprise software peer can match. Bears see a balance sheet carrying real leverage and deeply negative free cash flow.

Both sides have a case.

See historical and forward estimates for Oracle stock (It’s free!) >>>

Is Oracle Undervalued Today?

The valuation conversation starts with the backlog. RPO, or remaining performance obligations, the total value of signed contracts not yet recognized as revenue, ended Q3 FY26 at $553 billion, up 325% year over year.

Oracle stated in its Q3 press release that most AI contract growth is funded through customer prepayments or customer-supplied hardware, meaning it does not expect to raise incremental funds to support these contracts.

That disclosure directly addressed the market’s biggest concern about how Oracle finances the buildout without further straining its balance sheet.

At $170.77, Oracle trades at 13.63x NTM EV/EBITDA (enterprise value relative to forward EBITDA) and 21.67x NTM P/E.

On the TIKR Competitors page, ServiceNow trades at 14.58x NTM EV/EBITDA and 22.62x NTM P/E, a slight premium despite slower infrastructure growth. Adobe sits at 7.54x NTM EV/EBITDA and 10.16x NTM P/E, a discount that reflects its more mature business profile. Oracle’s 7.27x NTM EV/Revenue looks elevated against Adobe’s 3.57x, but Oracle’s forward revenue growth is running several times faster, which narrows the justification gap considerably.

The growth pipeline supports the multiple. Oracle raised FY2027 revenue guidance to $90 billion at Q3 earnings. The company confirmed it is targeting over 10 gigawatts of computing capacity over the next three years. Cloud applications, which include Fusion ERP (enterprise resource planning), Fusion HCM (human capital management), and NetSuite, posted an annualized revenue run rate of $16.1 billion in Q3, with deferred revenue growing faster than in-quarter recognition.

The risk is real. LTM free cash flow is negative $18,976.50 million, and net debt stands at $123,033 million at 4.12x net debt/EBITDA.

Oracle announced plans to raise $45 to $50 billion in fiscal 2026 to fund infrastructure expansion. The FCF drag is expected to persist through at least fiscal 2028 per TIKR’s forward estimates. The partial offset is contract structure: customer prepayments and customer-owned hardware reduce Oracle’s net capital outlay on the largest AI deals, so the gross capex figure overstates the true balance sheet exposure.

See how Oracle performs against its peers in TIKR (It’s free!) >>>

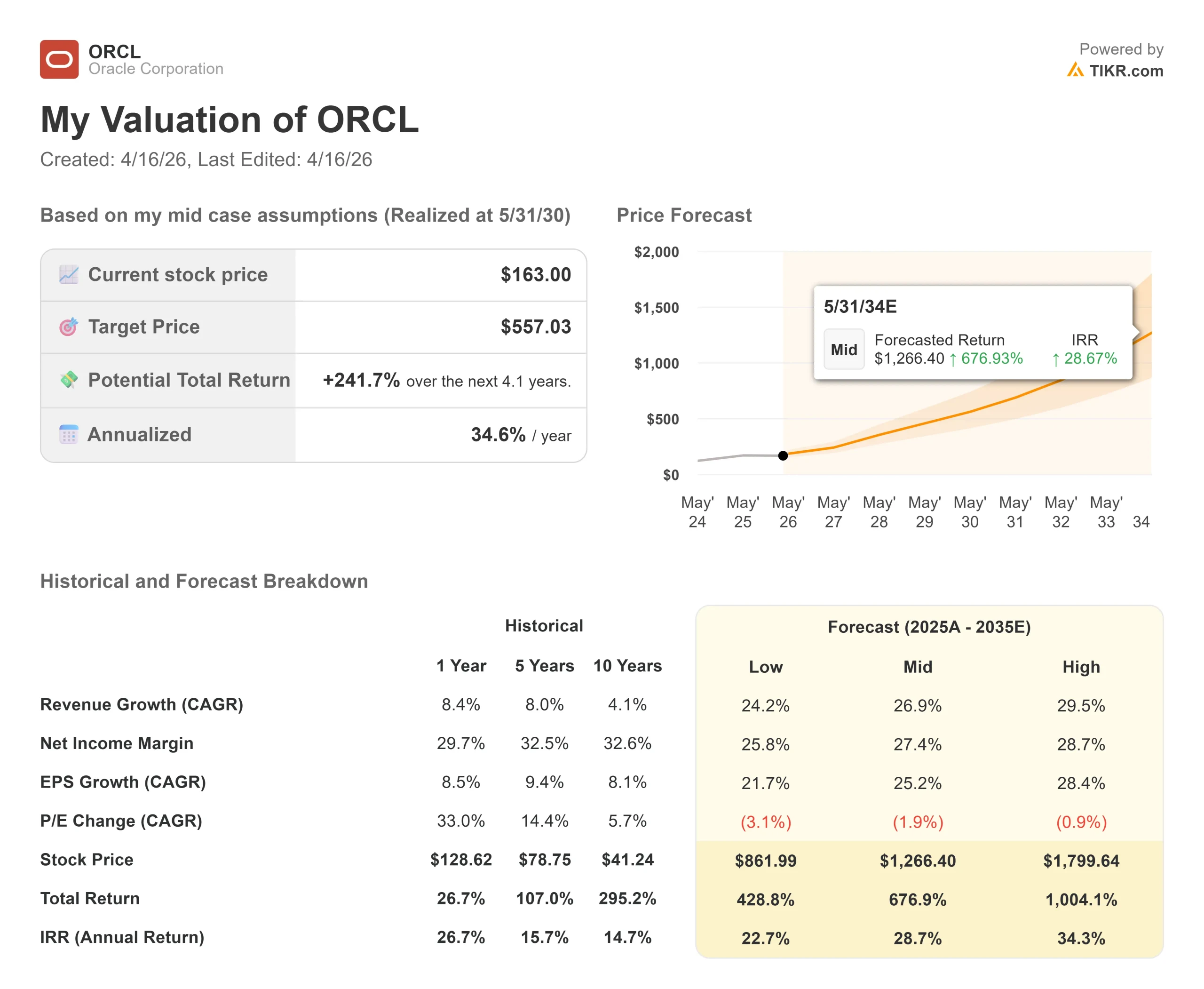

TIKR Advanced Model Analysis

- Current Price: $170.77

- Target Price (Mid): ~$557

- Potential Total Return: ~242%

- Annualized IRR: ~35% / year

See analysts’ growth forecasts and price targets for Oracle stock (It’s free!) >>>

The TIKR mid-case model was built at a $163.00 entry price. At today’s $170.77, the return from the current price is modestly lower, but the thesis is unchanged. The model targets around $557 by May 31, 2030, at roughly a 35% annualized return from the model entry.

Two revenue drivers support that path. The first is OCI, where AI infrastructure demand is compounding at 84% year-over-year growth, and the $553 billion RPO provides multi-year contracted visibility. The second is the cloud applications business, now running at $16.1 billion annualized with deferred revenue accelerating ahead of recognized revenue. Together, these support the model’s assumption of around 27% annual revenue growth through FY30.

The margin assumption of around 27% net income sits below Oracle’s recent historical range, a conservative input that accounts for ongoing interest expense and continued reinvestment. The upside: the backlog converts at current utilization rates, FY27’s $90 billion guidance proves conservative, and the multiple expands as free cash flow turns positive. The downside: AI demand softens, conversion slows, and the debt load leaves a limited buffer if revenue disappoints. The forecast ends May 31, 2030.

Conclusion

Watch cloud infrastructure revenue growth at Oracle’s Q4 FY26 earnings, expected mid-June 2026. If growth holds at or above the 84% posted in Q3, or gross margin on AI capacity expands beyond the 32% reported last quarter, the thesis strengthens materially. A deceleration below 60% alongside margin compression would signal that the capex cycle is running ahead of demand.

At 13.63x forward EBITDA against 44% annual cloud revenue growth, the TIKR model suggests the market has not yet fully priced in what Oracle has already booked.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Oracle?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Oracle, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Oracle alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!