Key Stats for Teradyne Stock

- 52-Week Range: $68 to $373

- Current Price: $367

- Street Mean Target: $325

- Street High Target: $400

- TIKR Model Target (Dec. 2030): $612

What Happened?

Teradyne (TER), the world’s largest provider of automated test equipment for semiconductors, has emerged as the clearest infrastructure play on the AI buildout, with the stock up over 400% from its 52-week low of $68.24 to $365.51 as AI-driven chip demand floods its order books.

The company reported Q4 2025 revenue of $1.08 billion, a 44% year-over-year jump that beat the $973 million consensus estimate, fueled by a surge in test demand for AI compute chips, high-bandwidth memory, and networking components.

AI-related demand drove more than 60% of Teradyne’s Q4 revenue, up from roughly 40% to 50% in Q3, as hyperscalers accelerated their data center buildouts and pushed chipmakers to expand testing capacity at an unprecedented rate.

The Q1 2026 guidance was the number that shocked the street: management guided revenue of $1.15 billion to $1.25 billion, roughly 34% above the $934 million analyst estimate, which would mark a new all-time quarterly record and a 75% year-over-year increase.

CEO Greg Smith stated on the Q4 2025 earnings call that “Teradyne is positioned to deliver better than market growth in markets that are going to be growing robustly over the next few years,” tying the outlook to an automated test equipment TAM that management expects to grow from roughly $9 billion in 2025 to $12 billion to $14 billion over the mid-term.

Teradyne’s long-term target model, unveiled alongside Q4 results, projects revenue of roughly $6 billion and non-GAAP EPS of $9.50 to $11.00 at full TAM maturity, implying nearly 2x its 2025 revenue base and 2.5x its 2025 earnings per share within the same planning horizon.

Underpinning that model is a structural shift in Teradyne’s revenue mix: compute, which represented only 10% of SoC (system-on-chip) test revenue in 2023, reached nearly 50% of the mix by the end of 2025, growing 90% year-over-year as the company captured approximately 50% share of the VIP (vertically integrated platform) compute market serving the largest AI chip hyperscalers.

Universal Robots, Teradyne’s collaborative robotics unit, launched the UR AI Trainer in March with Scale AI, a system designed to capture imitation-learning data for training physical AI models on the same hardware deployed in production settings, adding a second AI-adjacent growth vector beyond semiconductor test.

Wall Street’s Take on TER Stock

The Q4 beat and Q1 guidance raise confirm what the income statement has been quietly building toward: Teradyne is no longer a cyclical semiconductor equipment company defined by mobile phone upgrade cycles, but an AI infrastructure supplier running at record volumes with structurally higher demand visibility.

Teradyne’s normalized EPS reached $3.96 in FY2025, a 23% year-over-year increase, and consensus now estimates around $6.26 for 2026, a 58% jump driven by the company’s record Q1 guidance and the continued AI demand surge its CEO described as a “4-quarter boom” still running at full pace through mid-2026.

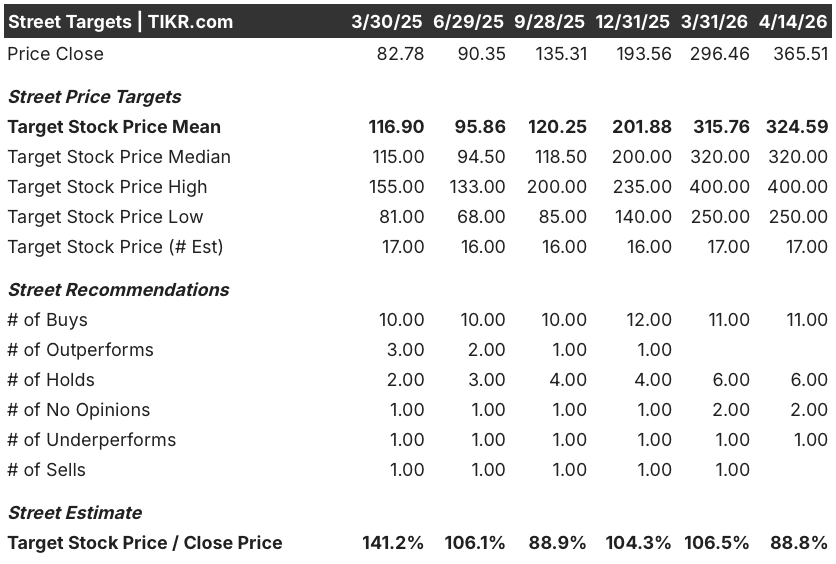

Eleven analysts hold buy ratings on TER, six hold neutral, and one rates it underperform, with a mean price target of $324.59 currently sitting 11% below the stock’s $365.51 close, a setup that reflects analyst targets set before the magnitude of the Q1 guidance raise became clear rather than a bearish consensus on the underlying business.

The analyst spread deserves attention: the street high target sits at $400, pricing in continued AI demand strength, while the low target of $250 reflects a downside scenario where compute demand digests faster than management’s multi-quarter boom timeline implies, making Q2 guidance the clearest signal for which end proves correct.

With 2026 EPS consensus near $6.26 against a stock at $365.51, TER trades at roughly 58x forward earnings, a multiple that looks stretched until the 58% EPS growth rate is applied: at near-1.0 PEG on a dominant ATE platform entering a multi-year AI infrastructure build, Teradyne stock appears undervalued relative to the earnings compounding its record backlog is now delivering.

Worth flagging as a genuine perception shift: management stated that more than 70% of Q1 2026 revenue is AI-driven, a share that moved from roughly 40% in Q3 to over 60% in Q4 to above 70% in Q1, a sequential acceleration that makes framing this as a peak-cycle story structurally difficult to sustain.

If AI data center CapEx compresses faster than Nvidia’s own multi-year demand signals suggest, Teradyne’s high revenue concentration in a small number of hyperscaler programs creates meaningful downside to both 2026 estimates and the long-term $6 billion model.

TER’s Q1 2026 earnings call on April 28 is the event to watch: the numbers that matter are Q2 revenue guidance relative to Q1’s record $1.15 to $1.25 billion range and any update to the AI demand mix percentage as a directional read on whether the current cycle has further to run.

Teradyne Stock Financials

Teradyne’s revenue climbed from $2.82 billion in FY2024 to $3.19 billion in FY2025, a 13.1% increase that marked the company’s return to growth after two consecutive years of revenue contraction totaling 28% from the 2021 peak.

The recovery is not cosmetic: TER’s operating income reached $680 million in FY2025, a 24.8% increase over $550 million in FY2024, as the compute-driven revenue mix shift produced higher-margin test demand that offset continued investment in R&D and SG&A expenses.

The operating leverage trajectory is the more striking story: from 2023’s trough operating margin of 19.3% to 21.4% in FY2025, Teradyne has rebuilt margin on volume recovery alone, with total operating expenses growing from $1.02 billion to $1.17 billion over that same period while operating income more than doubled from its trough.

What Does the Valuation Model Say?

TIKR’s mid-case valuation model targets $612 for TER, implying a 67% total return from current levels, built on a revenue CAGR of around 14% through 2030 and net income margins expanding toward 24%, assumptions that management’s own long-term model corroborates with a $6 billion revenue and $9.50 to $11.00 EPS target at ATE TAM maturity.

At $365.51, with 58% expected EPS growth in 2026 and a decade-high earnings model issued by management, Teradyne stock is undervalued relative to the compounding earnings power its AI-driven backlog is now demonstrably building toward.

The central tension in Teradyne stock is not whether AI demand is real. It is whether the current boom compresses into a sharp digestion before the next wave of complexity-driven test demand arrives to sustain the elevated revenue base.

Low Case: $583 (59% total return) The ATE TAM grows but digestion hits harder than expected in H2 2026, compressing revenue growth toward the low end of management’s range. Revenue CAGR comes in around 13%, net income margins hold near 23%, and the P/E multiple expands minimally. TER still compounds, but the path to $6 billion revenue stretches beyond the mid-term planning horizon.

Mid Case: $783 (114% total return) Management’s long-term model executes largely on schedule. Revenue grows at around 14% annually, net income margins expand toward 24%, and merchant GPU qualification in H1 2026 opens a new share gain cycle in a $4 billion-plus compute market. The ATE TAM reaches $12 billion to $14 billion within the model’s timeframe, and TER captures its projected $6 billion share.

High Case: $1,024 (180% total return) The AI infrastructure buildout accelerates beyond current hyperscaler CapEx commitments, co-packaged optics drive a new test intensity wave in networking, and TER captures materially above 50% VIP compute share as additional hyperscaler ASIC programs ramp. Revenue CAGR reaches around 16%, margins push toward 26%, and the $9.50 to $11.00 long-term EPS target arrives ahead of schedule.

Should You Invest in Teradyne, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TER stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Teradyne, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TER stock on TIKR for Free →