Key Stats for Bloom Energy Stock

- 52-Week Range: $16 to $219

- Current Price: $219

- Street Mean Target: $144

- Street High Target: $207

- TIKR Model Target (Dec. 2030): $762

What Happened?

Bloom Energy (BE), a California-based fuel-cell manufacturer that converts natural gas and hydrogen into electricity through electrochemical reactions rather than combustion, surged 24% to a new 52-week high of $219.03 on April 14 after expanding its Oracle partnership to supply up to 2.8 gigawatts of fuel cell capacity.

Oracle contracted an initial 1.2 gigawatts under a master services agreement, with deployments already underway at U.S. cloud infrastructure projects and continuing into next year.

The scale of the commitment underscores a structural shift: Bloom’s product backlog grew 140% year over year to approximately $6 billion, now spanning six hyperscale and neo-cloud customers compared to just one twelve months earlier.

Mahesh Thiagarajan, Executive Vice President of Oracle Cloud Infrastructure, stated in the April 13 announcement that “by rapidly deploying Bloom’s reliable, efficient fuel cell energy, we are quickly meeting the demands of our customers across the United States.”

J.P. Morgan responded by raising its price target on BE to $231 from $166, citing the scale of the Oracle agreement and Bloom’s strong backlog as justification for potential further capacity expansion.

On the Q4 2025 earnings call, K.R. Sridhar, Founder, Chairman and CEO, told investors that Bloom delivered a hyperscale AI factory order in 55 days against a 90-day commitment, demonstrating that the company’s capital-light manufacturing model can fulfill large-scale contracts faster than customers can build the facilities to receive them.

Bloom is uniquely positioned for the next wave of AI infrastructure: its fuel cell systems natively produce 800-volt direct current electricity, the architecture that next-generation AI compute racks require, while competitors must install expensive transformers and rectifiers to convert their alternating-current output.

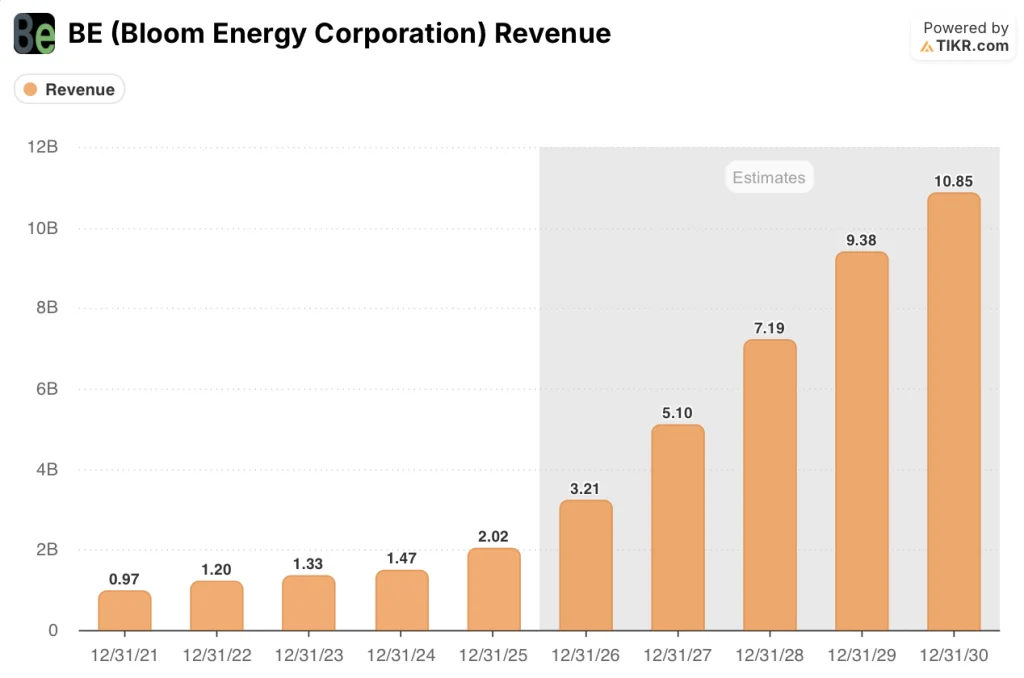

With 2026 revenue guided to $3.1 billion to $3.3 billion, commercial and industrial backlog up 135% year over year, and a $14 billion service backlog fully attached to product orders, Bloom’s growth story is no longer speculative — it is contracted.

Wall Street’s Take on BE Stock

The Oracle agreement does not merely add a revenue line: it signals that Bloom Energy stock is becoming the default on-site power solution for hyperscale AI infrastructure, a structural re-rating that consensus has not yet fully captured.

BE’s revenue reached $2.02 billion in 2025, a 37.3% increase, and consensus now projects $3.21 billion for 2026, a 59% jump driven by the Oracle deployment ramp and a commercial and industrial backlog surge that K.R. Sridhar described on the February earnings call as “secular and growing.”

Nine analysts rate Bloom Energy stock buy or outperform, twelve hold, and three carry sell-equivalent ratings, with a mean price target of $143.80 — sitting 34% below where the stock trades after the Oracle expansion was announced.

The spread between the $55 low target and the $207 high target reflects a genuine debate: bears see execution risk in deploying 2.8 gigawatts at pace, while the bulls who set the $207 target have now been validated by a stock that closed at $219 on announcement day.

With 26 consensus EBITDA at around $500 million, representing an 84% increase year over year, and EBITDA margins on a path from 13.4% in 2025 toward roughly 16% in 2026, Bloom Energy stock appears undervalued relative to the contracted revenue visibility that the Oracle master services agreement has now placed on the books, even as the share price has outrun stale consensus targets.

If natural gas prices spike materially, Bloom’s competitive cost position versus grid alternatives narrows and the premium multiple becomes difficult to defend.

The Q1 2026 earnings report is the next inflection point, where investors will watch whether the initial Oracle 1.2 GW deployment is converting to recognized revenue at the pace the $3.1 billion guidance floor requires.

Bloom Energy Stock Financials

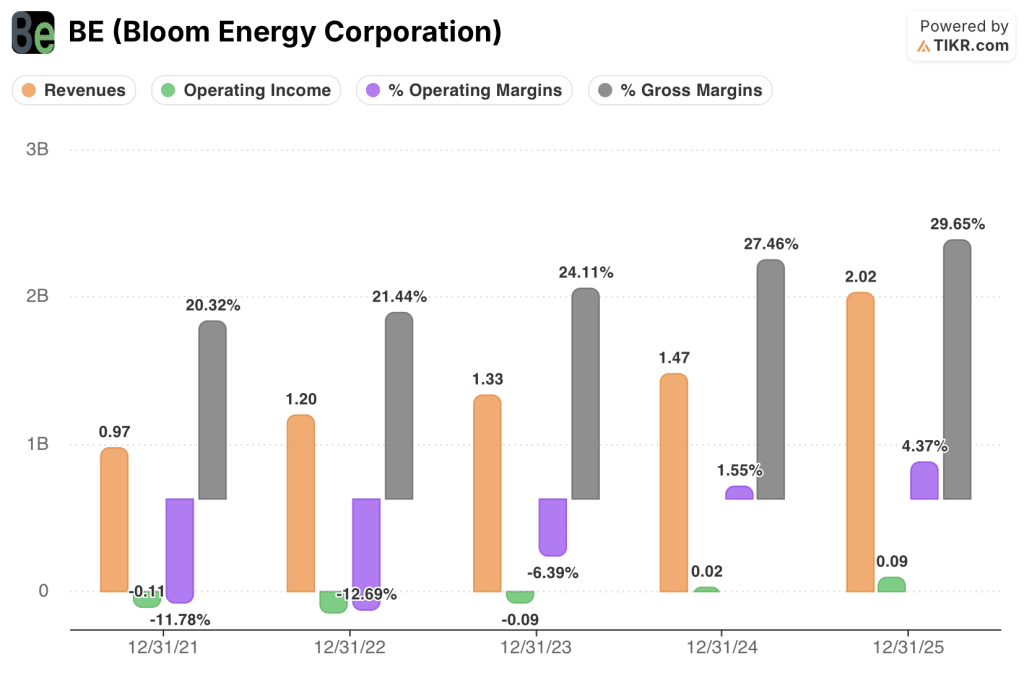

Bloom Energy’s revenue reached $2.02 billion in 2025, a 37.3% increase from $1.47 billion in 2024, marking the sharpest annual acceleration in the company’s five-year reported history.

The step-change in revenue traces directly to AI data center demand, which Bloom called out on the Q4 2025 earnings call as the primary driver of record full-year results, alongside broad commercial and industrial growth.

Operating income turned decisively positive in 2025, climbing from $0.02 billion in 2024 to $0.09 billion, as BE’s operating margin recovered from 1.6% to 4.4% — the first sustained profitability at the operating line in the company’s public history.

Gross margins have expanded in each of the past four reported fiscal years, from 21.4% in 2022 to 24.1% in 2023 to 27.5% in 2024 to 29.6% in 2025, a trajectory that reflects consistent fuel cell stack cost reduction and the contribution of a service segment that achieved approximately 20% non-GAAP gross margin in Q4 2025.

What Does the Valuation Model Say?

TIKR’s mid-case model assigns Bloom Energy a price target of $762, anchored to a 27% revenue CAGR from 2025 through 2030 and a net income margin expansion toward approximately 19%, assumptions the Oracle 2.8 GW master services agreement materially de-risks at the revenue line.

Against a contracted $6 billion backlog and 2026 revenue growth projected at 59%, a stock trading at $219 against a model mid-case of $762 leaves Bloom Energy stock appearing undervalued for investors who trust the secular AI power demand thesis behind the TIKR assumptions.

The investment case comes down to one question: whether Bloom’s capital-light manufacturing approach, where capacity expansion requires a fraction of legacy turbine suppliers’ upfront investment and delivers ROI in months, scales fast enough to fill the Oracle pipeline without margin deterioration.

What Has to Go Right

- The 1.2 GW initial Oracle tranche deploys on schedule, driving 2026 revenue toward the top end of the $3.1 billion to $3.3 billion guidance range

- C&I backlog, up 135% year over year, converts at historical rates, preventing dangerous over-concentration in hyperscale customers

- Gross margins hold above 29% and the service segment, already at approximately 20% non-GAAP gross margin for Q4 2025, scales with the installed base

- Bloom’s 800-volt DC native architecture becomes the preferred AI data center standard by 2027, creating a moat competitors cannot replicate without expensive retrofits

What Could Go Wrong

- Natural gas prices spike, compressing the cost advantage over grid alternatives and slowing C&I pipeline conversion in states where the economics were already tighter

- Oracle exercises the 3.5 million-share warrant at $113.28 and reduces incremental orders below the 2.8 GW maximum, leaving Bloom overbuilt on capacity

- Capacity expansion, described by management as “asset-light,” encounters supply chain bottlenecks as every major power infrastructure player races for the same components

- Consensus targets, currently averaging $143.80, take longer to catch up than the stock anticipates, capping multiple expansion until a revenue beat forces revisions

Should You Invest in Bloom Energy Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Bloom Energy Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BE stock on TIKR for Free →