Key Stats for Seagate Stock

- 52-Week Range: $71 to $517

- Current Price: $513

- Street Mean Target: $505

- Street High Target: $700

- TIKR Model Target (Jun. 2030): $1,086

What Happened?

Seagate Technology (STX), the world’s dominant manufacturer of high-capacity hard disk drives for cloud data centers, has delivered one of the sharpest earnings inflections in tech hardware history, with the stock up over 600% from its 52-week low as the AI storage boom permanently rewrites the company’s profitability trajectory.

The company posted Q2 fiscal 2026 adjusted EPS of $3.11, beating the $2.81 analyst consensus by 11%, as data center revenue reached $2.2 billion — up 28% year over year — and free cash flow hit $607 million, the highest level in eight years.

Management guided Q3 revenue to $2.9 billion (plus or minus $100 million), representing approximately 34% year-over-year growth at the midpoint, with non-GAAP EPS guided to $3.40 (plus or minus $0.20), well ahead of the prior $2.96 consensus estimate.

Seagate disclosed that its nearline hard drive capacity is fully allocated through all of calendar 2026, with volume and pricing locked in for every quarter, and that cloud customers are actively discussing demand requirements extending into 2027 and 2028.

The technology engine behind this margin expansion is HAMR (Heat-Assisted Magnetic Recording), Seagate’s proprietary manufacturing method that increases the amount of data storable per disk, allowing the company to grow exabyte output without adding unit production capacity and driving cost per terabyte lower with each product generation.

At the Morgan Stanley TMT Conference on March 3, CFO Gianluca Romano announced that “both customers that were in full for the 40-terabyte drive has now qualified the drive,” confirming that Mozaic 4, Seagate’s second-generation HAMR platform delivering 4 terabytes per disk, had cleared its first two major U.S. cloud service provider qualifications ahead of schedule, with volume shipments beginning in the current March quarter.

CEO Dave Mosley stated on the Q2 2026 earnings call that “as AI applications amplify the creation and economic value of data, modern data centers increasingly need storage solutions that combine performance and cost-efficiency at exabyte-scale,” framing the demand environment as a structural multi-year shift rather than a cyclical bounce.

On April 9, Seagate completed the divestiture of Lyve Cloud (its object storage-as-a-service business) to Wasabi Technologies in exchange for an equity stake, sharpening the company’s focus exclusively on high-margin hard drive manufacturing.

Wall Street’s Take on STX Stock

The market has repriced Seagate stock for the AI storage boom, but the rerating is not finished: Street price targets are chasing the EPS revisions upward rather than leading them, and the full Mozaic 4 cost-reduction payoff has yet to flow through analyst models.

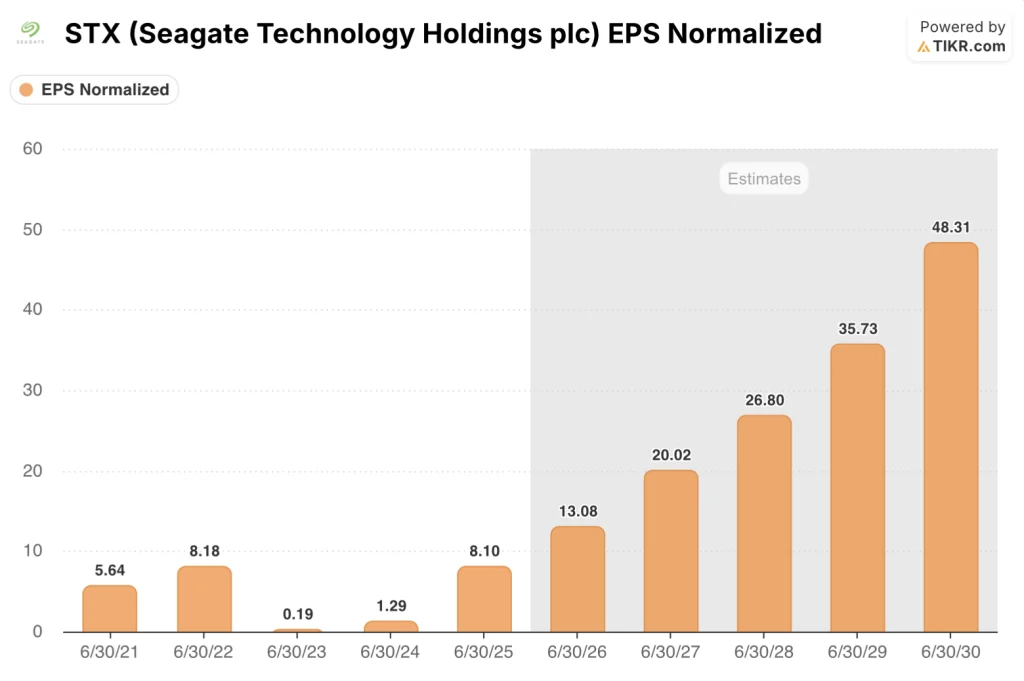

STX’s normalized EPS is expected to surge from $8.1 in fiscal 2025 to around $13 in fiscal 2026 and roughly $20 in fiscal 2027, a roughly 53% acceleration anchored to the Mozaic 4 ramp delivering 40-terabyte drives at a unit cost roughly equivalent to current 30-terabyte products, a transition that drops cost per terabyte by approximately 25% with no incremental capital spend.

Nineteen of 26 covering analysts rate Seagate stock a buy or outperform against five holds and two sells, with a mean price target of $505 and a median of $500, an unusual setup where the stock already trades roughly 2% above the mean — signaling that consensus is still catching up to the earnings trajectory rather than discounting it ahead of time.

The target spread runs from $375 on the low end to $700 on the high end: the $375 end assumes gross margins peak in the low-to-mid 40% range as Western Digital’s HAMR ramp intensifies competitive pricing pressure through 2027, while the $700 end assumes the HAMR cost curve keeps compressing and operating margins push toward 40% as full Mozaic 4 volume flows through the model.

At roughly 39x fiscal 2026 EPS estimates, Seagate stock looks expensive in isolation — until the fiscal 2027 forward multiple is applied, where roughly 53% EPS growth collapses that multiple to approximately 26x on accelerating earnings — leaving Seagate stock appearing undervalued against its three-year earnings trajectory even as it trades above every near-term analyst target.

Romano’s Mozaic 4 qualification announcement at the March 3 Morgan Stanley conference — volume shipments beginning this quarter rather than the second half — directly pulls forward the gross margin step-up timeline that the $505 mean target has not yet fully priced in.

Pricing discipline breaking down during the Mozaic 4 transition would be the most direct threat to the thesis: if cloud customers successfully renegotiate flat-to-down terms as 40-terabyte supply ramps, gross margin expansion stalls and the multi-year EPS trajectory compresses sharply.

Seagate’s Q3 fiscal 2026 earnings, expected in late April, will be the first report to reflect initial Mozaic 4 volume, with gross margin performance and the pace of additional CSP qualifications the specific numbers to watch.

Seagate Stock Financials

Seagate’s income statement has undergone one of the sharpest operating recoveries in storage sector history, with revenue rebounding from $6.55 billion in fiscal 2024 to $9.10 billion in fiscal 2025, a 38.9% increase driven entirely by the AI-fueled surge in nearline data center demand.

Operating income is the number that reframes the story: from a $0.12 billion loss in fiscal 2023 to $0.43 billion in fiscal 2024 to $1.93 billion in fiscal 2025, operating income expanded 344% in a single year as Seagate’s HAMR mix shift and disciplined pricing strategy pushed operating margins from 6.6% to 21.2%.

The LTM picture extends that trajectory further: on trailing revenue of $10.06 billion, Seagate is generating $2.59 billion in operating income at a 25.7% operating margin, a level that was structurally unachievable under the prior PMR (perpendicular magnetic recording) technology model and reflects the earnings leverage that HAMR delivers as volume scales.

Gross profit margins confirm the structural nature of the improvement: expanding from 23.6% in fiscal 2024 to 35.3% in fiscal 2025 and reaching 38.8% on an LTM basis, a trajectory that will extend further as Mozaic 4 drives (carrying materially lower cost per terabyte at the same unit cost as Mozaic 3) move from early qualification into high-volume production through the second half of calendar 2026.

What Does the Valuation Model Say?

The TIKR mid-case model targets $1,086 for Seagate stock by June 2030, implying 112% total return over 4.2 years at roughly 19% annualized, anchored to approximately 31% EPS CAGR assumptions through the period — a figure that sits below the consensus EPS growth forecast for fiscal 2026 and 2027, underscoring that the base case is a conservative rendering of what Mozaic 4 and future HAMR generations make structurally possible.

With EPS compounding from roughly $13 in fiscal 2026 to an estimated $27 in fiscal 2028 as Mozaic 4 drives cost-per-terabyte toward near-zero marginal cost, and the 39x near-term multiple collapsing to approximately 19x on fiscal 2028 earnings, Seagate stock is undervalued relative to its three-to-five-year earnings power even as it sits at its 52-week high.

The tension in the Seagate investment case is not whether the AI storage boom is real — it is whether the 11-quarter margin expansion streak reflects a permanent industry restructuring or a cyclical peak that eventually retraces the way the 2022 storage cycle did.

What Has to Go Right

- Romano confirmed at the Bernstein TMT Forum that the industry is running without unit capacity additions: “it’s not adding units, but it’s increasing exabyte from the same number of units” — a structural break from the 2021-2023 oversupply cycle that eliminated the glut mechanism which sent STX from $135 to $25 between 2022 and 2024

- Calendar 2026 nearline capacity is fully booked with pricing and volume locked in for every quarter, removing the intra-year pricing volatility that historically compressed storage margins in prior cycles

- Mozaic 4 qualifications at the first two major U.S. CSPs arrived ahead of schedule per Romano’s March 3 announcement, pulling forward the cost-per-terabyte reduction that is the largest gross margin driver in the model

- The TIKR high case targets $3,399 by fiscal 2034 on approximately 34% EPS CAGR and 36.2% net income margins, achievable if agentic AI, autonomous driving data, and AI-generated video each accelerate storage demand simultaneously as Romano described at both investor conferences

What Could Go Wrong

- STX already trades roughly 2% above the $505 consensus mean target at approximately 39x near-term EPS, meaning the stock has no valuation cushion if Mozaic 4 qualification milestones slip or gross margin guidance disappoints in the Q3 report

- Western Digital’s HAMR ramp is tracking, and Romano himself acknowledged at the Bernstein forum that cloud customers are technology-agnostic — caring only about terabytes per dollar — which means the pricing premium Seagate has extracted for being first may compress as WD achieves comparable 40-terabyte volumes in 2027

- The TIKR low case targets $1,624 by fiscal 2034 on approximately 27% EPS CAGR and 32.4% net income margins, still 216% above current levels but only around 15% annualized, a scenario that requires multi-year patience through what Romano acknowledged could include geopolitical disruptions to manufacturing operations

- The April 9 Lyve Cloud divestiture returned only an equity stake in a private company, which some investors may read as a signal that the storage-as-a-service segment was not performing to plan, removing a potential growth optionality lever from the thesis

Should You Invest in Seagate Technology Holdings plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up STX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Seagate Technology Holdings plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze STX stock on TIKR for Free →