Key Stats for Motorola Stock

- 52-Week Range: $359 to $492

- Current Price: $440

- Street Mean Target: $505

- Street High Target: $540

- TIKR Model Target (Dec. 2030): $626

What Happened?

Motorola Solutions (MSI), the mission-critical communications and public safety technology company, closed its best fiscal year in company history with record revenue, record operating margins, and a backlog figure that resets the growth debate for 2026.

Fourth-quarter net sales reached $3.38 billion, a 12% year-over-year increase that beat analyst expectations, while non-GAAP EPS of $4.59 outpaced consensus by 5.5%.

The number that makes the outperformance structural rather than seasonal is the ending backlog of $15.7 billion, up $1 billion from the prior year and the highest in company history, anchored by $2.4 billion in Q4 product orders alone, up $500 million from the year prior.

MSI also launched its first two public safety AI Assist Suites in January, role-based software packages priced at $99 per user per month for 911 dispatchers and first responders that integrate transcription, translation, report writing, and computer-aided dispatch (CAD) automation into a single platform.

Silvus Technologies, the defense-focused mobile ad hoc network (MANET) radio subsidiary Motorola SolutionsI acquired for $4.4 billion in August, delivered 2025 revenue of $570 million and is now tracking toward $675 million in 2026, an upward revision of $75 million from guidance issued just one quarter earlier.

Chairman and CEO Greg Brown stated on the Q4 2025 earnings call that “Q4 was an exceptional quarter across the board with record revenue in both segments, record operating earnings and record operating margins,” adding that the company “grew orders by 26% and ended the year with our highest ever backlog of $15.7 billion, up $1 billion year-over-year.”

MSI’s guidance for full-year 2026 calls for approximately $12.7 billion in revenue and non-GAAP EPS between $16.70 and $16.85, representing continued double-digit earnings growth, supported by Command Center software expected to grow 15%, Software and Services at 10% to 11%, and Silvus accelerating through its defense and unmanned systems funnel.

Wall Street’s Take on MSI Stock

The record backlog and Q4 outperformance are not the story; they are the evidence that MSI’s platform strategy, five years in the making, has built the kind of recurring demand that turns a hardware cycle into a compounding software franchise.

MSI’s normalized EPS grew 11% in 2025 to $15.38, and consensus now calls for approximately $17 per share in 2026 and around $18 per share in 2027, a trajectory supported by the Assist Suites platform rollout and the ongoing APX NEXT device refresh cycle that has 300,000 paying subscribers on track by year-end, up from 200,000 at the close of 2025.

Thirteen buys, five outperforms, and two holds among the 15 analysts covering the stock reflect a consensus that has grown more conviction as backlog normalization fears proved overblown; the mean target sits at $505, implying roughly 15% upside, with Wall Street watching the pace of Assist Suite adoption and Silvus order flow to determine whether that target moves higher.

The spread from $470 to $540 at the extremes captures a real debate: the low end prices in tariff headwinds and Silvus Ukraine concentration risk, while the high end bets on accelerating Command Center growth and a federal sales ramp following the FedRAMP High certifications for SVX and CommandCentral DEMS secured in February.

Priced at approximately 26x 2026 consensus EPS against a five-year historical forward P/E range that has generally traded between 30x and 35x, while delivering its fifth consecutive year of double-digit earnings growth and guiding another year of 100 basis points of operating margin expansion, Motorola stock appears undervalued relative to the compounding earnings profile the backlog and platform data support.

The risk is tariff exposure in the first half of 2026, with management quantifying an incremental $60 million headwind, concentrated in Q1, that could pressure near-term margins if pricing actions and vendor diversification do not fully offset it.

The catalyst is Command Center’s Q1 revenue report, where management explicitly guided growth above the 15% full-year target due to implementation timing; a strong Q1 print would validate the Assist Suite adoption thesis and likely trigger upward estimate revisions across the coverage group.

Motorola Solutions Stock Financials

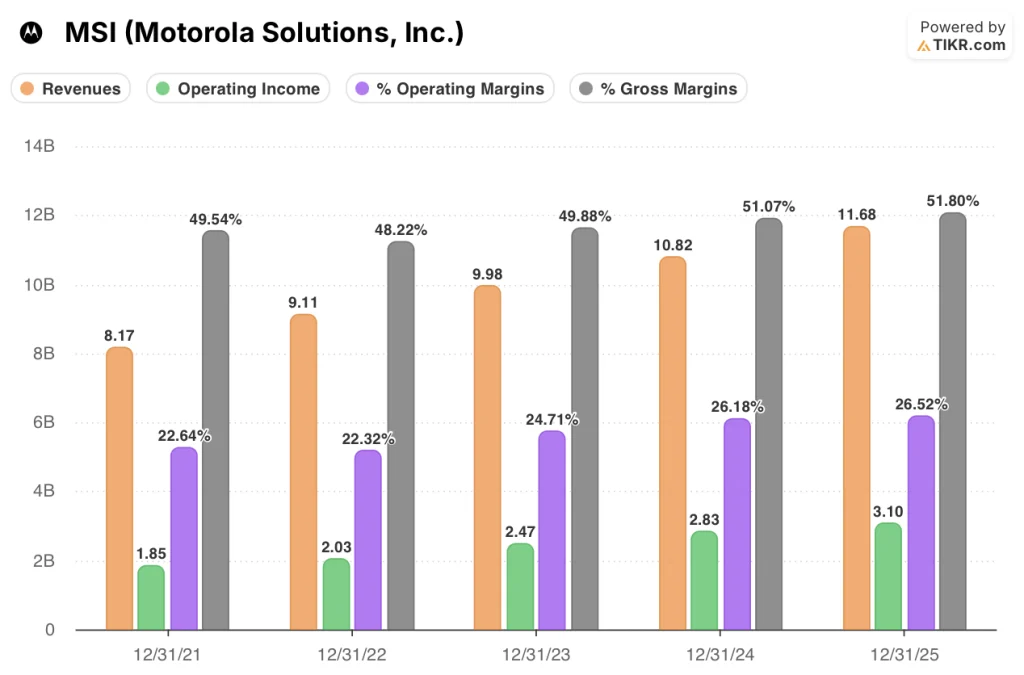

Motorola Solutions grew revenue from $8.17 billion in 2021 to $11.68 billion in 2025, a five-year compounding increase of 43% driven by consistent mid-to-high single-digit annual growth across both its Products and Software and Services segments.

The operating leverage story is more compelling than the revenue line: MSI expanded operating income from $1.85 billion to $3.10 billion over the same period, with operating margins climbing from 22.6% in 2021 to 26.5% in 2025, representing a 390 basis point expansion in four years as software and services mix shifted favorably.

Gross margins tell the same story, moving from 49.5% in 2021 to 51.8% in 2025, an increase that reflects the rising proportion of Software and Services revenue, which carried 32.5% operating margins in 2025 and is guided to grow 10% to 11% in 2026.

What Does the Valuation Model Say?

TIKR’s mid-case model assigns a target price of $626 to MSI, implying a 42% total return over roughly five years at an annualized rate of around 8%, driven by a 5% forward revenue CAGR assumption and a net income margin expanding from 21.9% toward approximately 23%, both inputs anchored by the Assist Suite recurring revenue rollout and Silvus scaling toward $675 million in 2026

With MSI trading at roughly 26x forward earnings while five consecutive years of double-digit EPS compounding and a $15.7 billion backlog argue for a significantly higher multiple, Motorola stock appears undervalued at current levels.

The central question is not whether MSI can maintain its platform-driven growth, but how fast the market re-rates a business that has quietly transitioned from a hardware cycle into a software compounder.

What Has to Go Right

- Command Center sustains its 15% growth rate in 2026, supported by 300,000 APX NEXT paying subscribers by year-end and Assist Suite adoption at $99 per user per month

- Silvus hits or exceeds its $675 million 2026 revenue target as defense and unmanned systems demand from NATO allies and U.S. federal customers offsets any moderation in Ukraine order flow

- Gross margins hold at or above 51.8% despite memory cost headwinds, supported by the continued Software and Services mix shift that now represents 38% of total revenue

- The $4.8 billion in backlog expected to convert to revenue in 2026 delivers on schedule, sustaining double-digit product order growth for a fourth consecutive quarter in Q1

What Could Go Wrong

- The incremental $60 million tariff headwind concentrated in Q1 2026 proves larger or more persistent than management modeled, pressuring operating margins below the guided 100 basis point expansion

- Silvus revenue is disproportionately Ukraine-dependent (Q4 upside was “largely led by Ukraine”), and any ceasefire scenario could reduce near-term order flow before NATO country demand fully offsets it

- APX NEXT subscriber ramp to 300,000 falls short of the year-end target, slowing Command Center software growth below the 15% guided rate and compressing the multiple re-rating thesis

- Competition in the AI-powered public safety software layer from Axon Enterprise, which already bundles competing AI features with its body-worn camera ecosystem, intensifies and pressures Assist Suite pricing or adoption rates

Should You Invest in Motorola Solutions, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MSI stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Motorola Solutions, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MSI stock on TIKR for Free →