Key Stats for GE Vernova Stock

- 52-Week Range: $306 to $1,007

- Current Price: $986

- Street Mean Target: $924

- Street High Target: $1,225

- TIKR Model Target (Dec. 2030): $2,852

What Happened?

GE Vernova (GEV), a global power equipment and grid infrastructure company spun from General Electric in April 2024, entered 2026 carrying a $150 billion backlog that has grown more than 50% in four years, and GE Vernova stock now trades near $986.

The company closed its $5.275 billion acquisition of the remaining 50% stake in Prolec GE, a transformer and grid equipment manufacturer previously held as a joint venture with Xignux, on February 2, immediately opening the North American market to transformer sales that had been contractually restricted under the old joint venture terms.

GE Vernova’s Q4 2025 orders surged 65% year-over-year to $22.2 billion, with gas power equipment backlog and slot reservation agreements, which are deposits customers place to secure future turbine delivery slots before converting to firm orders, expanding from 62 gigawatts to 83 gigawatts in a single quarter.

CEO Scott Strazik said at the Bank of America Global Industrials Conference that “the equipment margin in backlog from ’23 to ’26, those 4 years will add at least $22 billion in equipment margin driving future profitable growth,” connecting the backlog expansion directly to the company’s path from 8.5% EBITDA margins in 2025 to a 20% EBITDA margin target by 2028.

The combination of the Prolec acquisition, $11 billion in committed capex and R&D through 2028, and a gas turbine production ramp expected to reach an annualized 20 gigawatts per year starting in Q3 2026 positions GE Vernova to add at least $24 billion in cumulative free cash flow from 2025 through 2028 while simultaneously doubling transformer and switchgear output.

Furthermore, Morgan Stanley raised its price target on GE Vernova stock to $960 from $817 in March, citing increasingly bullish conviction on gas services and an Electrification segment where orders are outpacing revenue by $6 to $9 billion annually, with the backlog expected to double to $60 billion by 2028.

Wall Street’s Take on GEV Stock

The $150 billion backlog is the story, but the more important number is what is inside it: six points of equipment margin expansion added in 2025 alone, on top of five points added in 2024, creating a $22 billion pipeline of future margin dollars that has not yet hit the P&L.

GEV’s EBITDA reached $5.75 billion in 2025, a 79.8% year-over-year increase, and consensus now projects $8.67 billion in 2026 (up around 51%) on the back of the Prolec integration and the gas turbine production ramp, with EBITDA margins expanding from 12.9% in 2025 to around 17% in 2026 and around 23% by 2028.

Twenty-two analysts rate GE Vernova stock a buy, six rate it outperform, and five hold, with a mean price target of $923.63 against a current price of $985.92, meaning the stock is trading above the consensus mean, a reflection of how rapidly upward revisions have followed the backlog data.

The spread between the $600 low target and the $1,225 high target reflects a genuine debate: bulls are underwriting the full $22 billion of backlog margin materializing by 2028, while bears are discounting execution risk on the gas ramp and ongoing Wind losses that ran $600 million in 2025.

Priced at approximately 31x 2026 EBITDA, GE Vernova stock appears undervalued against a trajectory that puts the same enterprise value at roughly 18x 2028 EBITDA if management’s 20% margin target is achieved, a compression that implies substantial re-rating potential for investors willing to look past the near-term Wind drag.

If Wind losses remain elevated beyond the $400 million projected for 2026, driven by continued Vineyard Wind litigation or further U.S. offshore policy disruption, the consolidated margin expansion timeline shifts right and the 2028 target becomes harder to defend.

The April 22 first-quarter earnings call is the first test of whether the gas turbine production ramp is tracking to its promised Q3 inflection, with Power segment EBITDA margins, guided at 14% to 15% for Q1 against a 16% to 18% full-year target, as the specific figure to watch.

GE Vernova Stock Financials

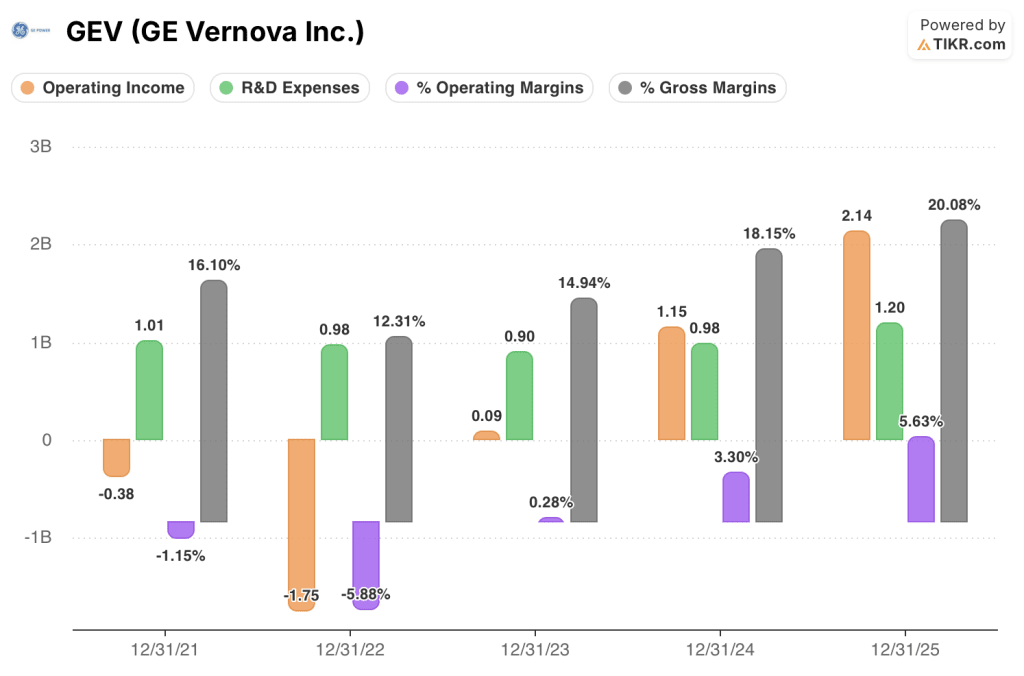

GE Vernova’s operating income reached $2.14 billion in 2025, an 85.9% year-over-year increase, representing the company’s most dramatic single-year profitability step-up since the spin as gas pricing strength and Electrification volume combined to drive a structural shift in the income statement.

The operating margin expansion from 3.3% in 2024 to 5.6% in 2025 reflects the first meaningful delivery of higher-priced backlog booked in 2023 and early 2024, a pattern that should accelerate as the 2024 and 2025 backlog vintages, carrying six additional points of equipment margin, begin hitting the P&L from 2027 onward.

Gross margins have expanded from 12.3% in 2022 to 20.1% in 2025, a nearly 800-basis-point improvement driven by pricing power in Gas Power services, Electrification volume leverage, and the declining weight of unprofitable offshore Wind contracts in the revenue mix.

The one tension in the income statement is that R&D spending rose from $980 million in 2024 to $1.20 billion in 2025, a 22% increase, compressing the gap between gross and operating margin expansion and signaling that the company is investing ahead of its production capacity in nuclear SMR development, solid-state transformer programs, and AI-driven engineering productivity tools.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $2,851 per share by December 2030 is built on a ~11% revenue CAGR through 2035 and a 17% net income margin assumption, inputs directly underpinned by the $22 billion of equipment backlog margin already locked in and a gas turbine order pipeline the CEO projects will reach 100 gigawatts under contract by year-end 2026.

With an 18.3% projected IRR and a mid-case return of 333% through 2030, GE Vernova stock appears undervalued for investors pricing the business on its 2028 earnings power rather than its 2026 transition-year P&L.

The entire investment case rests on a single question: can GE Vernova execute a factory ramp, absorb a $5.3 billion acquisition, and compress EBITDA margins from 12.9% today to 20% by 2028, simultaneously and without a quarterly miss?

What Has to Go Right

- Gas turbine output must reach the promised 20-gigawatt annualized run rate starting Q3 2026, unlocking higher-margin backlog vintages booked in 2024 and 2025 that carry 10 to 20 points more pricing than current deliveries

- The Prolec integration must open North American transformer revenues by 2027 as described, with the around $3 billion in Prolec revenue already contributing in 2026 and distribution transformer capability layered in for the data center market

- Electrification EBITDA margins must sustain 17% to 19% as backlog converts to revenue, validating the doubling of the segment backlog to $60 billion by 2028 alongside the Morgan Stanley upgrade thesis

- Wind losses must stay contained at around $400 million in 2026 with a clear path toward profitability as the remaining offshore backlog executes through Dogger Bank B and C

What Could Go Wrong

- Vineyard Wind litigation creates additional cost accruals beyond amounts already recorded, reopening the Wind loss trajectory in a year where the market is already discounting the segment

- Gas turbine deliveries remain back-half weighted through 2026 and the Q3 production ramp undershoots guidance, giving bears a concrete data point to anchor a multiple de-rating around

- Tariffs that cost around $70 million in Wind results in 2025 expand in scope under further U.S. trade policy changes, pressuring onshore wind margins and widening the 2026 Wind loss guidance

- The stock’s current premium to the $923 mean analyst target leaves no margin for error on any quarterly miss, and a reset of the 2028 margin guide would likely produce a sharp de-rating given the current multiple

Should You Invest in GE Vernova Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GEV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE Vernova Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GEV stock on TIKR for Free →