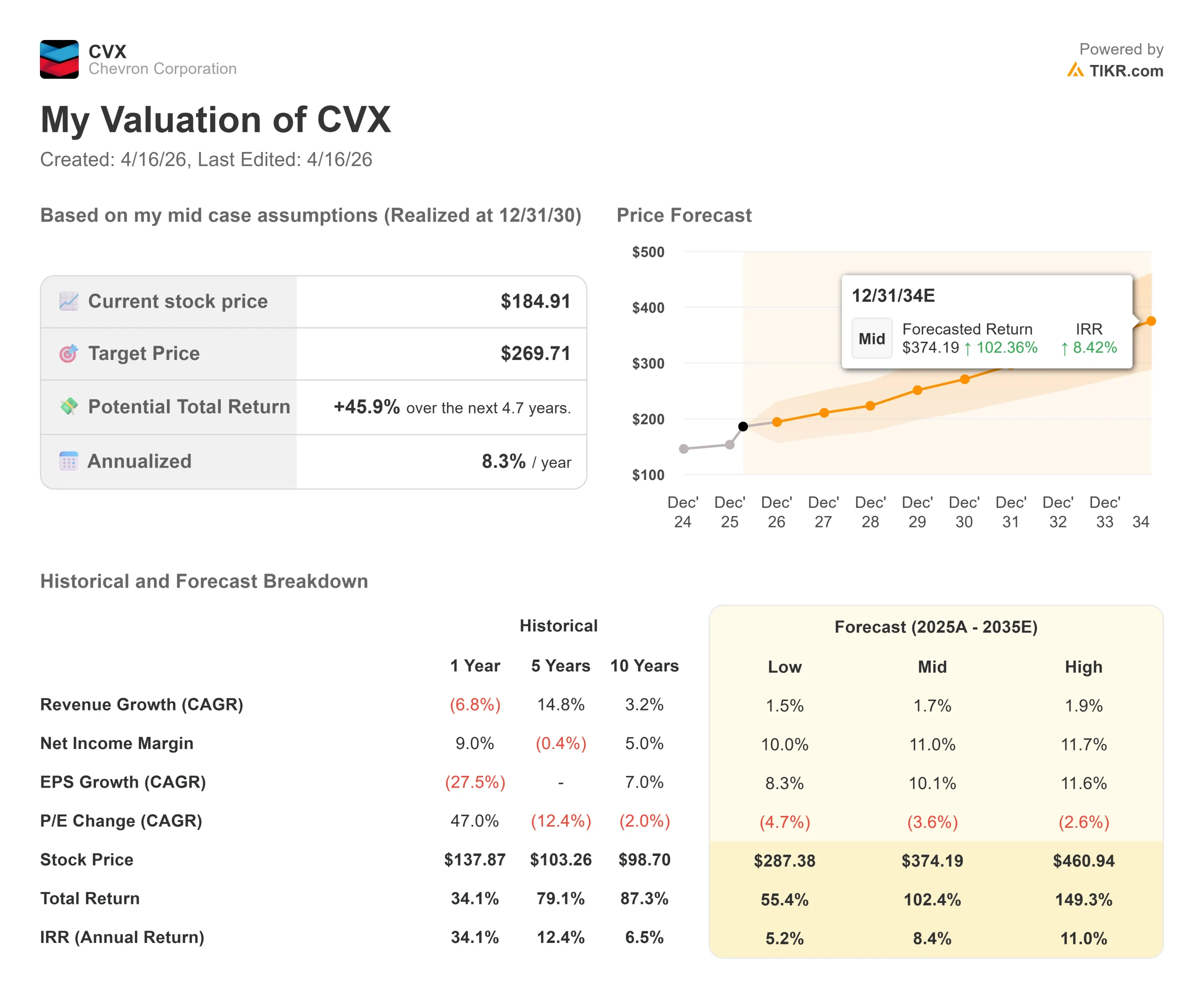

Key Stats for Chevron Stock

- Current Price: $184.91

- Target Price (Mid): ~$270

- Street Target: ~$211

- Potential Total Return: ~46%

- Annualized IRR: ~8% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Chevron (CVX) stock has pulled back nearly 14% from its 52-week high of $214.71, and the debate over what comes next is real.

Bulls point to record Permian production, a cost-savings program running ahead of schedule, and a Guyana ramp-up still in early innings. Bears argue that lower crude prices are compressing margins, that the Wheatstone LNG outage exposed operational risk, and that the recovery depends on factors Chevron cannot control.

The sell-off crystallized in early April. On April 1, Tropical Cyclone Narelle damaged Chevron’s Wheatstone LNG facility in Australia, one of its highest-margin businesses, sending CVX down nearly 6% in a single session. Then on April 12, the U.S. Navy’s blockade of the Strait of Hormuz added another layer of uncertainty, whipsawing energy stocks as markets priced in both supply disruption and potential ceasefire outcomes.

Two catalysts followed. On April 9, Chevron confirmed an oil discovery at the Bandit prospect in the Gulf of America, about 125 miles south of the Louisiana coast, where the well encountered high-quality oil-bearing Miocene sands. On April 14, Chevron finalized an asset swap with Venezuela’s state-owned PDVSA, deepening its footprint in the Orinoco Belt and increasing its stake in the Petroindependencia joint venture.

CEO Mike Wirth set the context on the Q4 2025 earnings call: “2025 was a year of execution. We set records, started up major projects, and strengthened our portfolio.” That included Permian production hitting 1 million barrels of oil equivalent per day and completing the Future Growth Project at Tengiz, which added 260,000 barrels per day. Q1 2026 results are due May 1.

See historical and forward estimates for Chevron stock (It’s free!) >>>

Is Chevron Undervalued Today?

At $184.91, Chevron trades at 7.41x NTM EV/EBITDA (next twelve months enterprise value to EBITDA). Exxon Mobil (XOM) trades at 7.75x on the same basis, Shell (SHEL) at 4.54x, and TotalEnergies (TTE) at 4.82x.

The Shell and TotalEnergies discounts reflect different downstream and geographic mixes. The Exxon comparison is most direct, and Chevron trades at a modest discount despite a 5-year beta of 0.59 that signals more stable cash flows than the sector average.

The cost program is the most important piece of the fundamental argument. CFO Eimear Bonner confirmed the cost reduction program exceeded expectations in 2025, delivering $1.5 billion in savings and capturing a $2 billion annual run rate, with more than 60% of savings expected to come from “durable efficiency gains.”

The target has since expanded to $3 to $4 billion by the end of 2026. Those savings flow directly into free cash flow. The TIKR forward estimates show FCF growing from $16.6 billion in 2025 toward $30.3 billion by 2030, with FCF margins expanding from around 9% to around 16%.

The dividend provides a floor. Chevron’s Q4 2025 earnings release confirmed a 4% increase in the quarterly dividend to $1.78 per share, marking 39 consecutive years of annual dividend growth. At $184.91, the annualized $7.12 payout yields about 3.9%. A company that maintained and grew its dividend through the 2020 oil price collapse has a different risk profile than a pure-play E&P.

The risk is direct: Chevron is a commodity business. Full-year 2025 net income came in at $12.3 billion, down from $17.7 billion in 2024, driven by lower crude prices. The TIKR model’s mid-case revenue CAGR of under 2% through 2030 reflects that honestly.

If Brent retreats to the low $60s and stays there, the free cash flow math weakens. Management has guided that its dividend-plus-capex breakeven sits below $50 Brent, which signals balance sheet resilience but not earnings power at depressed prices.

See how Chevron performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $184.91

- Target Price (Mid): ~$270

- Potential Total Return: ~46%

- Annualized IRR: ~8% / year

See analysts’ growth forecasts and price targets for Chevron stock (It’s free!) >>>

The TIKR mid-case targets around $270 by 12/31/30, implying around 46% total return and an annualized IRR of around 8%. That is a modest but risk-adjusted outcome for a company with a near-4% dividend yield, net debt/EBITDA of about 1x, and assets anchored in two of the lowest-cost basins on earth.

The two primary production drivers are Guyana and the Permian. Chevron’s 2026 growth is expected to come from shale and tight assets, adding around 130,000 BOE/d, Guyana adding around 125,000 BOE/d, the Gulf of Mexico contributing around 60,000 BOE/d, and TCO (Tengizchevroil, Chevron’s Kazakhstan joint venture) adding around 30,000 BOE/d. Guyana has not yet reached full run-rate contribution. The Hess acquisition brought Chevron into the Stabroek Block, and incremental barrels from that basin hit free cash flow at high margins because infrastructure is already in place.

The margin driver is the cost program. In announcing Chevron’s 2026 capital budget of $18 to $19 billion, CEO Mike Wirth said it “focuses on the highest-return opportunities while maintaining discipline and improving efficiency, enabling us to grow cash flow and earnings.” Chevron’s net income margin is projected to expand from around 7% in 2025 toward 11% by 2030 under the mid-case.

The high case reaches around $461, requiring faster cost savings, a faster Guyana ramp, and supportive oil prices. The downside case lands around $287, which still implies a positive return from current levels given the dividend yield.

Conclusion

Watch one number at the May 1 Q1 2026 earnings call: the cost savings run rate. If CFO Eimear Bonner reports a run rate above $2.5 billion against the $3 to $4 billion year-end target, the margin expansion thesis gets its first 2026 confirmation, and CVX should close the gap toward $211.

Chevron is a commodity business at a commodity valuation. The nearly 14% pullback from its highs has brought a Dividend Aristocrat with 39 consecutive years of dividend growth to a level where the margin of safety is real. The TIKR mid-case sees around 46% total return to 12/31/30, and at a 3.9% yield, you are paid to wait for it.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Chevron?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Chevron, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Chevron alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Chevron on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!