Key Stats for Norwegian Cruise Line Stock

- 52-Week Range: $15 to $27

- Current Price: $21

- Street Mean Target: $25

- Street High Target: $38

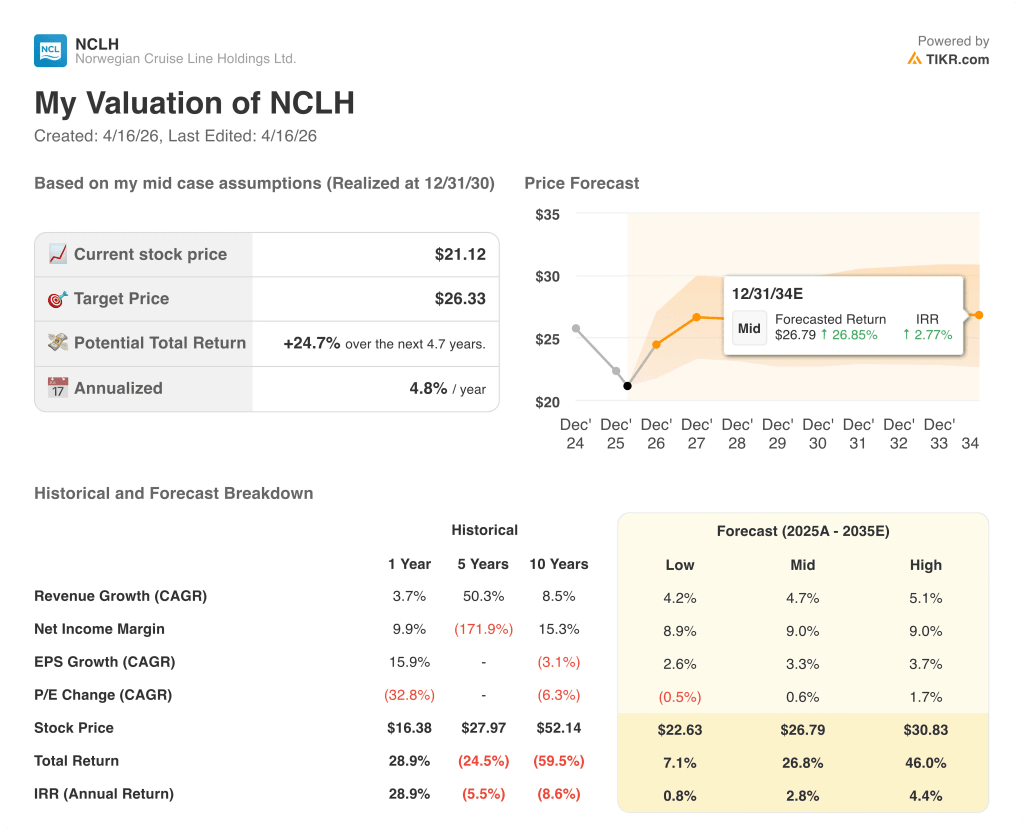

- TIKR Model Target (Dec. 2030): $26

What Happened?

Norwegian Cruise Line Holdings (NCLH), the world’s third-largest cruise operator running three brands across Norwegian Cruise Line, Oceania Cruises, and Regent Seven Seas Cruises, is trading near $21 as investors weigh a simultaneous leadership overhaul and Elliott Investment Management’s push to unlock what the activist believes is a $56-per-share business.

The story accelerated in February when Elliott disclosed a 10%-plus stake in NCLH, the largest in the company, alongside a public demand for board refreshment and a new business plan, citing years of underperformance against rivals Royal Caribbean and Carnival that have compounded while Norwegian Cruise Line stock fell 13% in 2025 alone.

Elliott’s pressure triggered a March Q4 2025 earnings report that confirmed the scale of the problem: revenue of $2.24 billion missed the $2.35 billion consensus estimate by roughly 5%, fiscal 2026 adjusted EPS guidance of $2.38 came in below the Street’s $2.55 estimate, and new CEO John Chidsey acknowledged the company had made “certain execution missteps” that left it entering 2026 slightly below its optimal booking range.

John Chidsey, President and CEO, stated on the Q4 2025 earnings call that “our strategy is sound, our execution and coordination have not been, and a culture of accountability is essential and necessary going forward,” framing the investment case as a turnaround of process rather than product.

On March 27, Norwegian reached a cooperation agreement with Elliott, adding five new independent directors including former British Airways CEO Alex Cruz as lead independent director and former Disney Experiences CFO Kevin Lansberry, with Chidsey also taking the chairman title and receiving a $48 million equity package tied to total shareholder return targets of 5% to 20% CAGR over four years.

The board reset coincides with a tangible operational catalyst on the horizon: the Great Tides Waterpark at Great Stirrup Cay, the company’s private Bahamian island, remains on track to open this summer, which management expects to meaningfully lift Caribbean yield performance beginning in Q4 2026 as roughly a third of passengers are routed through the island.

Wall Street’s Take on NCLH Stock

The Elliott board deal transforms Norwegian Cruise Line stock from a “management credibility discount” story to an “execution recovery” story, with the new leadership team’s ability to align revenue management, deployment, and commercial strategy now the single variable the entire forward earnings case depends on.

NCLH’s EBITDA is projected to recover from $2.73 billion in fiscal 2025 to approximately $3 billion in fiscal 2026 and roughly $3 billion in fiscal 2027, with the Street’s modest 4% to 10% annual EBITDA growth estimates reflecting genuine skepticism that itinerary misalignment in the Caribbean, Europe, and Alaska can be corrected within a single booking cycle.

Thirteen analysts rate Norwegian Cruise Line stock a buy or outperform against 11 holds across 24 analysts tracked by TIKR, with a mean price target of around $25 implying roughly 19% upside from current levels, a consensus that has been cut steadily from $30 in December and reflects the Street pricing in continued near-term yield headwinds before the board-driven improvements take hold.

The spread between the $18 low target and the $38 high target is the widest in at least a year and represents a genuine debate: bears anchoring to the near-flat 2026 yield guide and a 5.2x net leverage ratio see limited re-rating potential until NCLH demonstrates sustained execution, while bulls anchoring to Elliott’s $56 target see a business that is self-inflicting wounds the new board is now structurally positioned to reverse.

With normalized EPS estimated at approximately $2 for fiscal 2026 rising to around $3 in fiscal 2028, and the stock trading at roughly 10x forward earnings versus Royal Caribbean at over 15x, Norwegian Cruise Line stock appears undervalued relative to its earnings recovery potential, though the discount reflects real execution risk that has not yet been resolved.

The Risk: if the Great Tides Waterpark opening is delayed or fails to lift Caribbean yields in Q4 2026, the core assumption behind the second-half recovery breaks and the fiscal 2026 EBITDA guide of $2.95 billion comes under pressure.

Q1 2026 earnings, expected in early May, are the first confirmation gate: watch net yield growth against the company’s own guidance of approximately negative 1.6%, and any commentary on second-half booking momentum in the Caribbean and Europe is the specific signal to track.

Norwegian Cruise Line Stock Financials

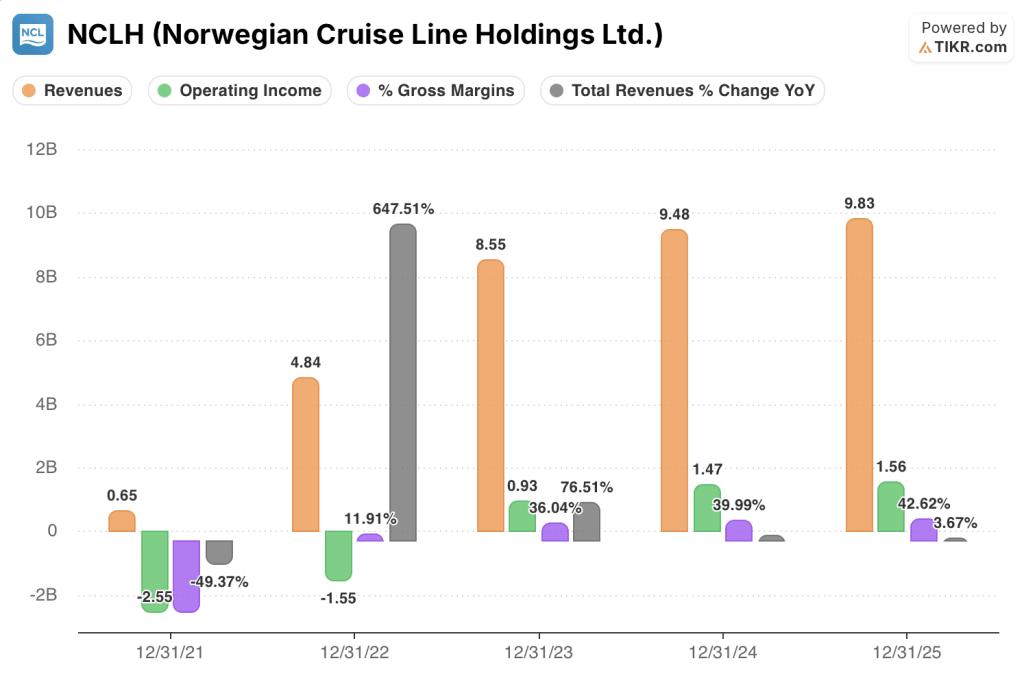

Norwegian Cruise Line’s income statement shows a business that has compounded its revenue base from $8.55 billion in fiscal 2023 to $9.83 billion in fiscal 2025, a 15% gain over two years, while operating income grew from $0.93 billion to $1.56 billion over the same period, expanding operating margins from 10.9% to 15.9%.

The margin trajectory is the bullish data point the stock price has not fully credited: gross margins expanded from 36% in fiscal 2023 to 42.6% in fiscal 2025, a 660-basis-point improvement driven by disciplined cost management that CFO Mark Kempa described as nearly three consecutive years of sub-inflationary unit cost growth against a $300 million-plus savings program.

The tension is that this healthy cost discipline has been partially masked by the revenue missteps: total revenues grew only 3.7% in fiscal 2025, the slowest pace since the post-pandemic recovery, and the execution failures in Caribbean deployment coordination mean the operating leverage the income statement should be generating is not yet showing up in net yield growth.

If the commercial realignment under the new revenue management leadership restores even modest net yield growth toward the 2% to 3% range the prior strategy targeted, the operating margin structure already in place positions NCLH to convert incremental revenue at a high flow-through rate as the fixed cost base is largely set.

What Does the Valuation Model Say?

TIKR’s model tests whether Norwegian Cruise Line’s cost discipline, which produced nearly three consecutive years of sub-inflationary unit cost growth, is durable enough to generate meaningful earnings power once the commercial realignment under the new board and CEO takes hold, and the range of outcomes is wide precisely because the execution question remains open.

- Low case (~$23): Revenue growth stalls near 4% as Caribbean and European yield headwinds persist through 2027, net income margins stay near 9%, and the leverage discount keeps the multiple compressed

- Mid case (~$27): Roughly 5% revenue CAGR, margins stabilize around 9%, Great Tides lifts Caribbean yield in Q4 2026, and the Elliott board deal gradually closes the multiple gap with peers

- High case (~$31): Full execution recovery under the new leadership team, revenue CAGR accelerating toward 5%, margins expanding as SG&A optimization delivers on the $300 million-plus savings program, and the re-rating toward Royal Caribbean’s peer multiple drives returns above 40%

With the mid-case implying around 27% upside from $21 and the high case pointing toward $31 on credible assumptions that require execution rather than optimism, NCLH appears undervalued at current levels for investors who believe the Elliott-backed board reset is a genuine operational catalyst and not just a governance headline.

The whole argument for Norwegian Cruise Line stock comes down to one question: is this a fixable execution problem or a structural competitive disadvantage?

What Has to Go Right

- Great Tides Waterpark opens on schedule this summer and lifts Caribbean yield performance in Q4 2026, giving the 2027 guidance cycle a credible foundation that restores analyst confidence in NCLH’s booking trajectory

- The new revenue management leadership, described by Chidsey as a “seasoned industry veteran” installed in recent months, successfully aligns deployment with commercial strategy across Caribbean, European, and Alaska itineraries in time to impact 2027 bookings

- Elliott’s five new board members, drawing on experience running British Airways (Cruz), Disney Experiences (Lansberry), and Bain Capital (Pagliuca), impose the financial discipline and accountability culture that Chidsey acknowledged was missing across the organization

- CEO equity award of $48 million vesting against a 5% to 20% TSR CAGR target over four years aligns Chidsey’s incentives directly with the recovery outcome investors are underwriting

What Could Go Wrong

- Net leverage at 5.2x at year-end 2026 leaves the balance sheet with limited flexibility: if the Middle East conflict keeps fuel costs elevated (Brent has already crossed $100 per barrel), NCLH’s 51% fuel hedge for 2026 means roughly half of any further spike flows directly through to earnings

- The company enters 2026 slightly below its optimal booking range across Caribbean, European, and Alaska itineraries, and the booking lead times inherent in the cruise industry mean 2026 is largely locked in, with any commercial realignment under the new leadership team not fully flowing through until 2027 at the earliest

- Royal Caribbean’s peer group trades at a meaningful premium to NCLH, and if Royal Caribbean continues to demonstrate execution superiority, the re-rating case for NCLH narrows to an absolute value argument rather than a relative catch-up trade

- Q4 2025 GAAP net income was $14.3 million on $2.24 billion in revenue, an effectively zero margin quarter driven by a $95 million IT asset write-off, signaling the technology underinvestment Chidsey flagged will require capital before it generates returns

Should You Invest in Norwegian Cruise Line Holdings Ltd.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NCLH stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Norwegian Cruise Line Holdings Ltd. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NCLH stock on TIKR for Free →