Key Stats for Starbucks Stock

- 52-Week Range: $76 to $105

- Current Price: $98

- Street Mean Target: $100

- Street High Target: $122

- TIKR Model Target (Dec. 2030): $133

What Happened?

Starbucks Corporation (SBUX), the world’s largest coffeehouse chain with over 41,000 locations across 90 global markets, delivered its first U.S. comparable sales growth in two years in Q1 fiscal 2026, making Starbucks stock the clearest turnaround story in large-cap consumer staples.

The catalyst was a January earnings report confirming the “Back to Starbucks” operational overhaul is generating transaction-level results: U.S. company-operated comparable store sales grew 4%, with transactions contributing 3 percentage points of that comp, the first positive U.S. transaction growth in eight consecutive quarters.

Total consolidated revenue reached $9.9 billion in Q1 fiscal 2026, up 5% year over year, with international comparable sales accelerating to 5% growth and China delivering 7% comp growth for its third consecutive positive quarter.

Brian Niccol, Chairman and Chief Executive Officer, stated on the Q1 fiscal 2026 earnings call that “we are now achieving top line growth driven by transactions, and we have clear plans on how we expect to turn top line growth into margin and earnings growth,” anchoring the bull case directly to a sequential earnings recovery in fiscal 2026’s back half.

On April 2, Starbucks finalized its joint venture with Boyu Capital, a Chinese private equity firm, transferring 60% ownership of approximately 8,000 China company-operated stores to a licensed model that structurally improves consolidated profitability, while both partners target eventual expansion to 20,000 China locations.

The same day, Starbucks announced a new U.S. barista incentive program covering weekly pay, expanded mobile-order tip access, and performance bonuses of up to $1,200 annually, with the company framing the package as a retention investment at a moment when labor stability is the operational foundation the entire earnings recovery depends on.

Wall Street’s Take on SBUX Stock

The Q1 report shifts the narrative on Starbucks stock from “when will the turnaround show up in transactions” to “how quickly can transaction growth convert to operating leverage,” a reframe that changes the forward earnings math meaningfully.

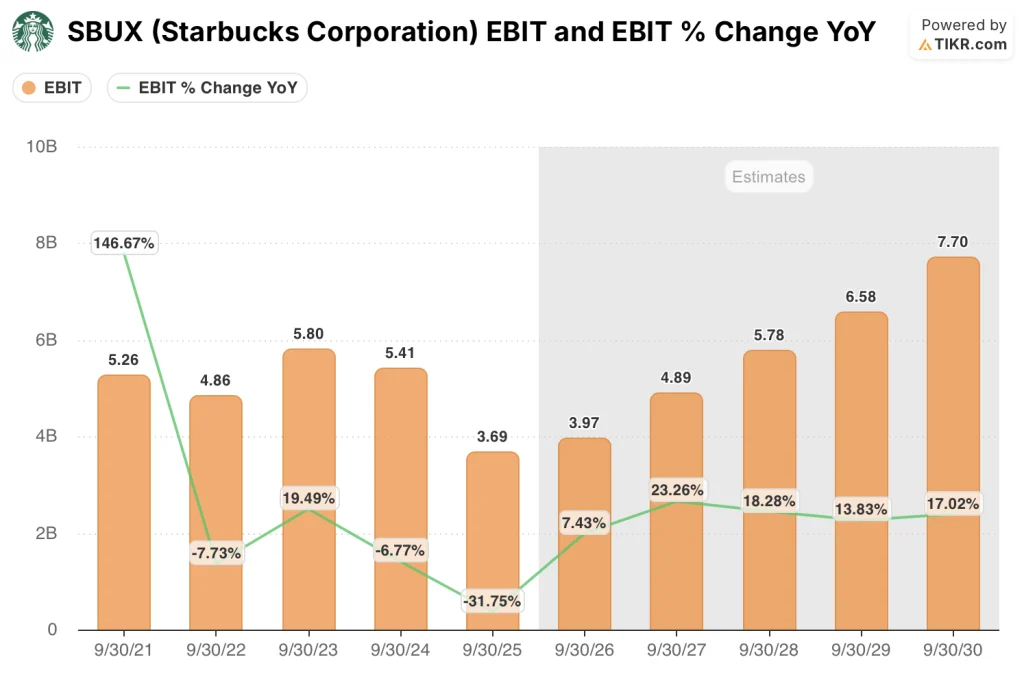

SBUX’s EBIT is projected to recover from $3.69 billion in fiscal 2025 to approximately $4 billion in fiscal 2026 and roughly $5 billion in fiscal 2027, representing close to 23% growth year over year, driven by the Green Apron Service labor model (a $500 million annualized coffeehouse staffing investment) anniversarying in Q4 and the Boyu JV eliminating company-operated China cost drag.

Sixteen analysts rate Starbucks stock a buy or outperform against 19 holds and 4 underperforms or sells across 34 analysts tracked by TIKR, with a mean price target of around $100 implying barely 2% upside; the tight consensus reflects a Street that acknowledges the turnaround is real but demands Q2 comp confirmation before committing to upgrades.

The spread between the $74 low target and the $122 high target reveals a genuine debate: bulls anchoring to fiscal 2028 EPS of approximately $4 see a compelling multiple, while bears anchoring to fiscal 2025 EPS of $2.13 near the trough argue the recovery timeline is longer than management’s public roadmap assumes.

With normalized EPS estimated at around $2 for fiscal 2026 and approximately $4 for fiscal 2028, the stock currently prices in a slow recovery; at roughly 25x fiscal 2028 estimated earnings, with a confirmed China JV and the first transaction growth in two years now on record, Starbucks stock appears undervalued relative to the earnings power two years out.

Jefferies upgraded Starbucks to “hold” from “underperform” on April 13, citing stabilizing U.S. business performance and materially reduced global risk following the China JV close, the first tangible sign of analyst sentiment shifting after a prolonged stretch of cautious ratings.

Labor negotiations remain the live risk: the Starbucks Workers United union filed a U.S. labor board complaint in April accusing the company of bad-faith bargaining, and an unfavorable contract outcome could entrench the elevated labor cost base that operating leverage is supposed to grow through.

Q2 fiscal 2026 earnings on April 28 are the confirmation gate: watch U.S. comparable store sales against the full-year guide of 3%-plus, because two consecutive quarters of transaction growth would give the bull case the momentum needed to close the gap between the $100 consensus and the $122 high target.

Starbucks Stock Financials

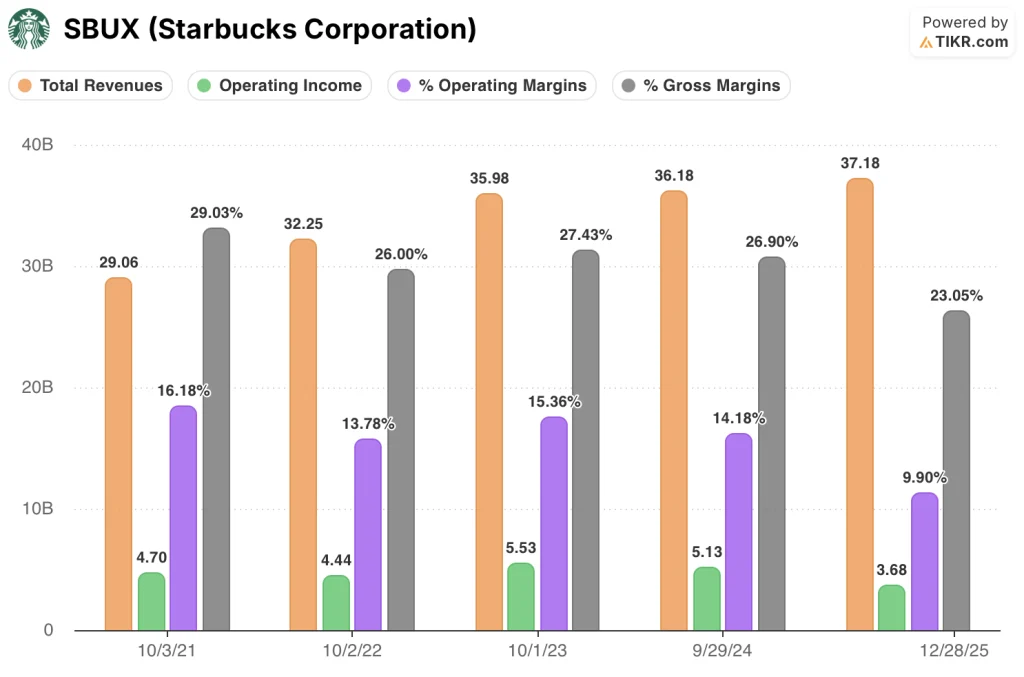

Starbucks’ income statement tells a deliberate sacrifice story: total revenues grew from $35.98 billion in fiscal 2023 to $37.18 billion in fiscal 2025, a modest cumulative gain, while operating income compressed from $5.53 billion to $3.68 billion as Niccol front-loaded $500 million in annualized labor investment under the Green Apron Service model.

The operating margin decline from 15.4% in fiscal 2023 to 9.9% in fiscal 2025 represents a deliberate trade of near-term profitability for the transaction growth that Q1 fiscal 2026 confirmed is materializing, with the cost structure now positioned to anniversary.

Gross margins also compressed, falling from 27.4% in fiscal 2023 to 23.0% in fiscal 2025, with the pressure coming from elevated Arabica coffee commodity costs, tariff-related input inflation, and a mix shift toward mobile ordering and delivery channels that carry higher fulfillment costs than traditional in-store transactions.

The income statement setup from here is an anniversary story: Green Apron Service investments lap in Q4 fiscal 2026, coffee commodity inflation is expected to peak in Q2 and ease in the second half, and the Boyu JV removes company-operated China cost drag, leaving the operating margin recovery path into fiscal 2027 materially cleaner than the fiscal 2025 financials imply.

What Does the Valuation Model Say?

TIKR’s mid-case model targets roughly $133 for SBUX, assuming approximately 5% revenue CAGR through fiscal 2030 and net income margins recovering to around 10%, a recovery that becomes more credible with each quarter the Q1 transaction inflection continues and the Boyu JV margin accretion compounds through the licensed model.

At roughly 25x fiscal 2028 estimated normalized EPS of approximately $4, with a confirmed China joint venture and management’s public commitment to 5%-plus revenue growth and operating margins of 13.5% to 15% by fiscal 2028, the current price underestimates where earnings are heading, leaving Starbucks stock undervalued for investors willing to hold through the remaining 18 to 24 months of the turnaround.

Everything in the Starbucks investment case converges on a single question: whether the Q1 transaction inflection is durable enough through the year to sustain the operating leverage the margin recovery math requires.

What Has to Go Right

- U.S. comparable store sales hold at 3%-plus through fiscal 2026, sustaining the transaction growth from Q1 across morning, afternoon, and drive-thru dayparts and preventing any single quarter from reopening the bear case

- The Green Apron Service labor investment anniversaries fully by Q4 fiscal 2026, unlocking the operating leverage that management projects will drive consolidated margins toward 13.5-15% by fiscal 2028

- The Boyu JV contributes structurally higher international margins, with the licensed model expected to push international segment operating margins toward 20%-plus by fiscal 2028 versus 13% in fiscal 2025

- The new three-tier Starbucks Rewards loyalty program, relaunched March 10, drives incremental frequency: management projects that half of active members transacting one additional time per year would add $150 million in annual revenue

What Could Go Wrong

- Union contract talks escalate beyond April’s labor board complaint into broader work stoppages, raising structural labor costs precisely when operating leverage is the primary mechanism for the margin recovery

- Macro-driven consumer softness weakens afternoon daypart traffic before the energy refresher and personalized beverage platforms scale, leaving comp performance dependent solely on morning ritual momentum into Q2

- Coffee commodity prices and tariff input inflation persist beyond Q2 fiscal 2026, delaying gross margin recovery and pushing the operating income inflection deeper into fiscal 2027 or beyond

- The fiscal 2028 EPS guidance range of $3.35 to $4.00 carries execution risk wide enough that Deutsche Bank analyst Lauren Silberman publicly called it “too wide” at Investor Day, a signal that the Street’s skepticism on timing has not been fully resolved

Should You Invest in Starbucks Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SBUX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Starbucks Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SBUX stock on TIKR for Free →