Key Stats for Intel Stock

- Current Price: $64.94

- Street Target (Mean): ~$51

- TIKR Target Price (Mid): ~$180

- Potential Total Return: ~177%

- Annualized IRR: ~12% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

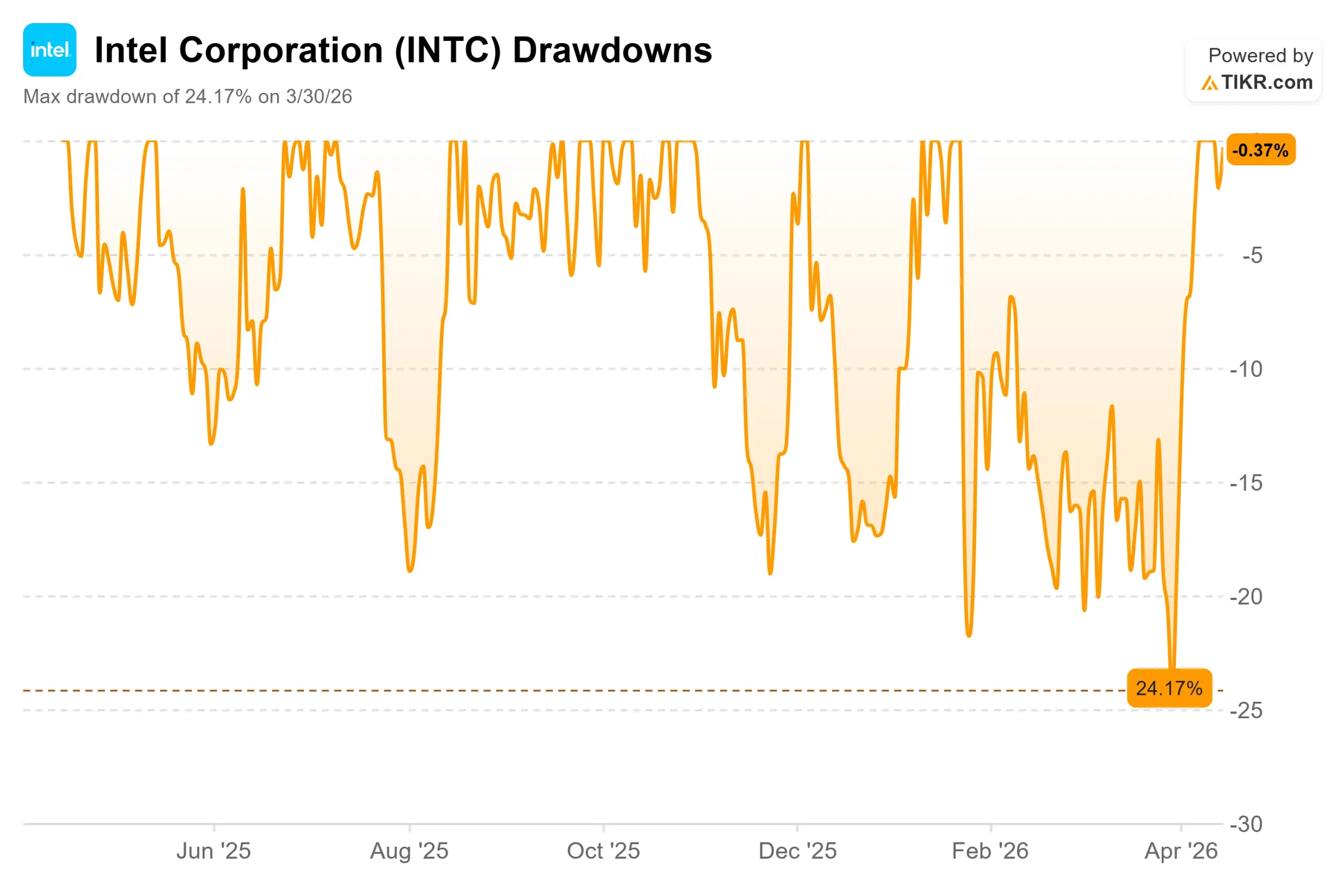

Intel (INTC) has staged one of the most dramatic rallies in its recent history. INTC has gained 76% year to date, rising from $36.90 at year-end 2025 to $64.94 as of April 15, on the back of a string of foundry catalysts that have reframed the entire investment case.

Bulls argue the turnaround under CEO Lip-Bu Tan is finally taking hold. Bears point to a stock now trading at 126x forward earnings with negative free cash flow, a Street consensus target of around $51 that the stock has already blown past, and an Intel Foundry unit that posted an operating loss of approximately $10.3 billion in fiscal 2025. The key question going into Q1 earnings on April 23: can the business actually catch up?

The catalyst that defined April came on April 7, when Intel announced it is joining Elon Musk’s Terafab project as primary foundry partner, a $25 billion semiconductor joint venture between Tesla, SpaceX, and xAI targeting one terawatt of AI compute per year at a facility in Austin, Texas.

Intel shares jumped roughly 4% on the announcement and added another 11% the next session. The deal is built around Intel’s 18A process node, which incorporates gate-all-around transistor architecture and backside power delivery, though exact financial terms and production timelines have not been publicly confirmed.

For a foundry business that generated just $307 million in external customer revenue for all of fiscal 2025, this is the most significant external commitment in its history.

That news followed another major move on April 1, when Intel reached a definitive agreement to repurchase Apollo Global Management’s 49% stake in Fab 34 in Leixlip, Ireland, for $14.2 billion. Intel had sold that same stake to Apollo in June 2024 for $11.2 billion when the company was under financial pressure. Buying it back at a $3 billion premium sent shares up roughly 9% and signaled management’s confidence in the balance sheet recovery.

On Intel’s Q4 2025 earnings call on January 22, Lip-Bu Tan, Chairman and Chief Executive Officer, was direct about what he is seeing from customers: “Their first choice is the CPU from Intel. They will try to get as much as we can give them.”

He also framed the ambition plainly: “The era of artificial intelligence is driving unprecedented demand for semiconductors.” CFO David Zinsner noted on the same call that Intel’s custom ASIC, meaning application-specific integrated circuit, business grew more than 50% in 2025 and reached an annualized revenue run rate above $1 billion in Q4.

See historical and forward estimates for Intel stock (It’s free!) >>>

Is Intel Undervalued Today?

At $64.94, Intel trades at 6.31x NTM EV/revenues and 20.91x NTM EV/EBITDA. The Street mean target sits at around $51, meaning the stock has already run past the average analyst’s twelve-month price objective.

Against peers, the valuation looks cheaper on the surface.

NVIDIA trades at roughly 12.76x NTM EV/revenues and AMD at around 8.79x, per TIKR’s Competitors page. Intel’s 6.31x discount is partially explained by its integrated device manufacturer, or IDM, model, which means it both designs and fabricates chips, carrying structurally higher capital intensity than fabless peers like AMD or Nvidia. The NTM market cap to free cash flow multiple is negative at (63.96x), reflecting ongoing cash burn.

The bear case rests on three figures that are hard to dismiss.

Intel Foundry’s operating loss in fiscal 2025 was approximately $10.3 billion. LTM free cash flow is negative $4.3 billion. And at 126x forward earnings, the stock is pricing in a recovery that has not yet appeared in reported results. Q1 2026 guidance, provided on the January 22 earnings call, points to a supply-constrained trough with revenue of $11.7 billion to $12.7 billion and management targeting roughly 40% gross margins for the full year, compared to the LTM gross margin of 36.6%.

What sustains the bull case is the foundry pipeline building beneath those losses.

Intel’s 18A node is the most advanced chip process developed and manufactured on U.S. soil, a differentiation that matters to hyperscalers and government customers seeking a domestic alternative to TSMC.

The custom ASIC business crossing a $1 billion annualized run rate confirms the external customer base is beginning to form. And the Fab 34 buyback is the clearest capital allocation signal yet: management chose to spend $14.2 billion on its own manufacturing assets when it could have preserved liquidity.

See how Intel performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $64.94

- TIKR Target Price (Mid, 12/31/34): ~$180

- Potential Total Return: ~177%

- Annualized IRR: ~12% / year

See analysts’ growth forecasts and price targets for Intel stock (It’s free!) >>>

The TIKR mid-case model projects Intel reaching approximately $180 by December 31, 2034, based on around 5% annual revenue growth and net income margins recovering to around 11%. Two drivers support that revenue path. The first is the Data Center and AI segment (DCAI), which posted $16.9 billion in fiscal 2025 revenue and benefits directly from the AI-driven server CPU demand Tan described on the earnings call. The second is Intel Foundry, which needs to convert the Terafab commitment and other pipeline deals into recurring external revenue. LTM gross margin sits at 36.6%, well below where margins need to go, and the path to around 11% net income by 2034 requires foundry losses to narrow materially as 18A production scales.

The high case reaches approximately $222 by 2034, around 242% total return at roughly 15% annualized. The low case reaches approximately $139, around 114% total return at roughly 9% annualized, which is less compelling given the execution risk involved. The primary downside trigger is yield failure on the 18A node or foundry customer attrition if Terafab does not convert to volume production.

Conclusion

The single metric to watch on April 23 is Intel Foundry’s external customer revenue. In Q4 2025, it was $222 million, the highest quarterly figure Intel has reported. Any sequential acceleration would confirm that Terafab and other foundry wins are converting from announcement to contract. A flat or declining figure would be the clearest signal that the rally has run ahead of the fundamentals.

Intel is not the same company that hit a 52-week low of $18.25. The Terafab deal, the Fab 34 buyback, and the 18A ramp are real catalysts. Whether a stock already past its Street consensus target can sustain 126x forward earnings depends entirely on how fast that foundry pipeline converts to revenue. April 23 is the first real test.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Intel?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Intel, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Intel alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!