Key Stats for Duolingo Stock

- 52-Week Range: $88 to $545

- Current Price: $99

- Street Mean Target: $105

- Street High Target: $145

- TIKR Model Target (Dec. 2030): $188

What Happened?

Duolingo, Inc. (DUOL), the world’s most downloaded education app with over 52.7 million daily active users, crossed $1 billion in annual revenue for the first time in 2025 and then watched its stock collapse more than 80% from its 52-week high of $544.93 as management voluntarily handed back near-term profit to chase a bigger prize.

The trigger came on the Q4 2025 earnings call when CEO Luis von Ahn announced a deliberate strategic pivot: instead of continuing to optimize monetization through friction, Duolingo would spend 2026 prioritizing daily active user growth, including absorbing more than $50 million in foregone bookings from removing conversion prompts and expanding access to premium AI features.

The most revealing number was not the revenue beat but the guidance gap: full-year 2026 bookings are expected between $1.27 billion and $1.30 billion, roughly $90 million below what Street consensus had modeled and what management acknowledged it could have delivered by staying the course.

Luis von Ahn stated on the Q4 2025 earnings call that “if we’re seeing faster user growth than we’re expecting, and what we are expecting is about 20%, then that means the strategy is working,” tying the entire 2026 investment case to a single measurable DAU acceleration target.

The medium-term logic centers on doubling daily active users to 100 million by 2028 across three growth engines: deeper language teaching powered by AI, a friction-reduced free experience to reaccelerate top-of-funnel growth, and fast-scaling new subjects including chess, which attracted 7 million DAUs in less than a year, alongside math and music, with a $400 million share buyback authorizing capital return alongside the growth investment.

Wall Street’s Take on DUOL Stock

The pivot reframes the investment case from “how fast can Duolingo monetize its existing user base” to “how large can the active learner base become before monetization resumes,” and the answer to that second question determines whether the current multiple is a trap or a generational entry.

DUOL’s revenue reached $1.04 billion in FY2025 at a 38.7% growth rate, and consensus still models $1.21 billion for FY2026 at around 16% growth, declining to around 15% in FY2027 as the transition year absorbs the foregone bookings, before recovering toward faster growth as DAU reinvestment pays off in FY2028 and beyond.

The analyst community has not rushed to endorse the strategy: just 4 of 23 analysts rate Duolingo stock buy or outperform, 18 are at hold, and one is a sell, with a mean price target of $105.44 implying barely 7% upside from current levels, a consensus that reflects wait-and-see positioning rather than conviction in either direction.

The target range from $81 to $145 captures the genuine debate: bulls anchoring near $145 believe the DAU acceleration materializes faster than modeled and monetization returns with a bigger denominator, while bears at $81 see the strategy stalling and EBITDA margins compressing further below the 25% guide.

A company growing revenue at roughly 16% this year while trading at around 14x forward normalized EPS represents a compression from the 80x-plus multiples DUOL sustained through its growth years, and with chess already at 7 million DAUs in under a year and advanced language content rolling out to B2 proficiency level, the business has more growth levers than the consensus multiple implies, leaving Duolingo stock appearing undervalued against a backdrop of deliberately deferred monetization rather than structural demand deterioration.

CFO Gilian Munson noted on the Q4 call that bookings were tracking above Q1 guidance as of late February, suggesting the friction-removal initiative has not cratered near-term engagement.

If DAU growth fails to hit the 20% target in 2026, the entire rationale for sacrificing near-term bookings collapses, and the Street will reassess whether management made the right call.

Q1 2026 earnings on May 4 is the first real data point: DAU growth relative to the 20% target and bookings relative to the $301.5 million guide will either validate the strategy or force the next leg down.

Duolingo Stock Financials

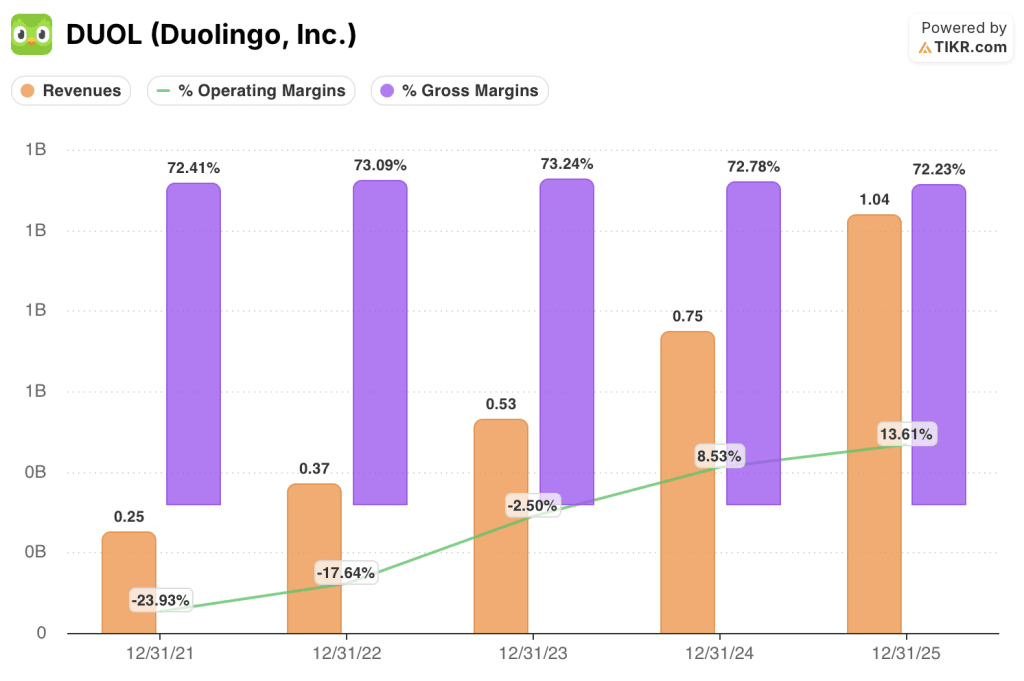

Duolingo generated $1.04 billion in revenue in FY2025, a 38.7% increase year over year and the fifth consecutive year of revenue growth accelerating from a base of $250 million in FY2021.

The operating leverage in the model is real: DUOL reached a 13.6% operating margin in FY2025, up from 8.5% in FY2024 and from deeply negative territory in the prior two years, as revenue growth consistently outpaced operating cost expansion driven by scale efficiencies in its content and technology infrastructure.

Gross margins have held structurally stable across the entire revenue scaling period, ranging from 72.2% to 73.2% since FY2021, confirming that the core delivery model does not degrade at scale even as the user base expanded more than 4x.

The tension in FY2026 is explicit: management’s plan to extend AI features including Video Call with Lily to Super Duolingo subscribers, a tier with roughly 10x the subscriber count of the prior Max-only tier, is expected to pressure gross margins below FY2025 levels, testing whether the structural cost advantage survives the deliberate access expansion.

What Does the Valuation Model Say?

The TIKR mid-case model targets $188 for DUOL by end of 2030 based on a revenue CAGR of around 10% from 2025 through the forecast period and net income margins expanding to around 32%, a scenario directly supported by the company’s stated path toward 100 million DAUs and management’s own projection of a $2.5 billion revenue business with over $700 million in adjusted EBITDA.

At roughly 14x forward normalized EPS for a platform compounding revenue above 15% this year, with 85% market share in language learning apps globally and chess scaling faster than almost any new product launch in the company’s history, the current price materially undervalues Duolingo stock relative to what the mid-case DAU scenario implies.

The entire investment case hinges on one question: does the 2026 DAU investment produce the user growth acceleration management is betting on, or does it prove that Duolingo’s active learner base is approaching saturation faster than the company believes?

What Has to Go Right

- DAU growth hits or exceeds the 20% target in 2026, with Q1 earnings on May 4 delivering the first confirmation; Q1 bookings were tracking above the $301.5 million guide as of late February

- Video Call with Lily expanding to Super Duolingo reaches roughly 10x more subscribers than Max, lifting engagement and retention in a way that rebuilds monetization at a larger base later in 2027 and 2028

- Chess at 7 million DAUs in under one year demonstrates Duolingo can build entirely new subject verticals at scale, with math targeting a 1 billion-person addressable market and carrying meaningfully higher parental propensity to pay

- The $400 million buyback provides a price floor and signals management confidence at a moment when the stock trades near its 52-week low of $87.89, with $1.04 billion in cash on the balance sheet at year-end 2025

- AI inference cost deflation continues: the cost of Video Call has already fallen more than 10x since launch, and continued cost reduction makes the access expansion self-funding faster than modeled

What Could Go Wrong

- Bookings growth of roughly 11% in 2026 is a structural deceleration from 33% in FY2025, and if DAU growth disappoints, the company will have sacrificed near-term profitability without capturing the user base expansion that justifies the trade

- EBITDA margin guided to compress from 29.5% in FY2025 to approximately 25% in FY2026 as AI and marketing spend accelerate; a second year of margin pressure in 2027 would force another re-rating of the stock

- Argus downgraded Duolingo stock to hold in March, specifically citing the “likely pressure” on bookings from the new strategy, and 18 hold-rated analysts represent a significant pool of potential downgrades if Q1 data misses

- Social media virality that once drove top-of-funnel growth at minimal cost has moderated significantly from peak levels, making organic user acquisition harder to replace at scale

- The TIKR low-case scenario carries a revenue CAGR of around 9% and still projects P/E multiple compression of (6.7%) per year through 2035, meaning execution at the low end of the range could leave the stock flat for years even as the business technically grows

Should You Invest in Duolingo, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DUOL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Duolingo, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DUOL stock on TIKR for Free →