Key Stats for Uber Stock

- Current Price: $78.38

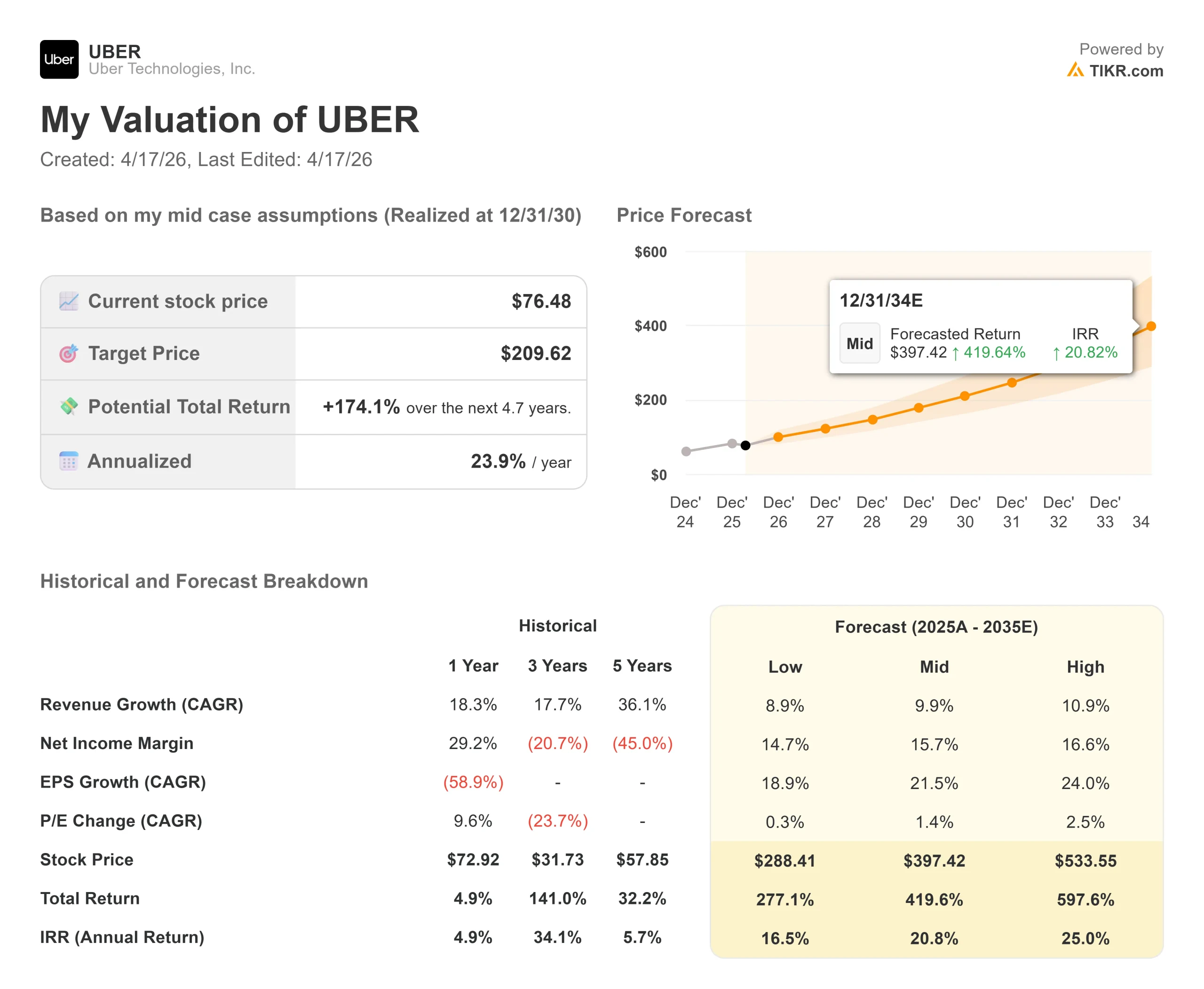

- TIKR Model Entry Price: $76.48

- TIKR Mid-Case Target: ~$210

- TIKR Mid-Case IRR: ~21% per year

- Street Target (Mean): ~$103

- Upside to Street Target: ~31%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Uber (UBER) closed 2025 above $101 and then spent the first quarter of 2026 giving most of it back. The stock hit a 52-week low of $68.46 before recovering to the high $70s, leaving it roughly 23% below its peak and at a maximum drawdown of 30.89% on March 27. The operating business underneath that price action, though, has rarely looked stronger.

Two events this week brought the bull-bear tension back into focus. On April 15, the Financial Times reported that Uber is committing over $10 billion to robotaxis, with roughly $7.5 billion going toward procuring autonomous vehicle fleets and over $2.5 billion in equity investments in AV developers, with capital tied to specific deployment milestones.

Partners include Rivian, Lucid Motors, and China’s Baidu. Then today, Uber announced it is buying a 4.5% stake in Delivery Hero from Prosus for €270 million, making it the fourth-largest shareholder in the Berlin-based food delivery platform.

The acquisition is part of Uber’s push into European food delivery, where it is targeting an additional $1 billion in gross bookings from new markets over three years.

The AV announcement lifted the stock roughly 6% over the past week. But it also reopened the central bear argument: Uber’s value was always built on being asset-light, meaning it collects platform fees without owning vehicles. Committing $10 billion to fleet ownership looks like a pivot away from that model precisely when free cash flow is at record levels.

CEO Dara Khosrowshahi addressed the tension on Uber’s Q4 2025 earnings call on February 4, 2026. “We enter 2026 with a rapidly growing topline, significant cash flow, and a clear path to becoming the largest facilitator of AV trips in the world,” he said.

His case is that a hybrid network of human drivers and autonomous vehicles on the same platform generates higher vehicle utilization than any AV-only competitor can match. Early data from Uber’s AV deployments in Austin and Atlanta already shows those markets among the fastest-growing in Uber’s entire U.S. network.

See historical and forward estimates for Uber stock (It’s free!) >>>

Is Uber Undervalued Today?

Uber generated $9,763 million in free cash flow in FY2025, up 42% year-over-year. At a market cap of roughly $155.8 billion, that is about 16 times trailing free cash flow, a difficult multiple to call expensive for a business compounding cash flow at 40%-plus annually.

The Q4 EPS miss that knocked the stock lower in February was almost entirely driven by a $1.6 billion non-cash hit from equity investment revaluations. Operationally, Q4 was strong: trips grew 22% year-over-year, delivery gross bookings crossed a $100 billion annualized run-rate for the first time, and operating cash flow reached $2,883 million for the quarter.

The $10 billion AV investment deserves a careful read before concluding it breaks the asset-light model. The capital flows out over time, tied to deployment milestones, not as a lump sum.

Uber’s own data shows its hybrid AV network in Austin and Atlanta delivers roughly 30% more trips per vehicle per day than comparable standalone AV deployments in other cities. That utilization advantage is what Khosrowshahi argues justifies the platform’s continued central role even as AV supply scales.

The Delivery Hero stake tells a parallel story about Uber’s delivery ambitions. Delivery revenue reached $17,248 million in FY2025, growing faster than the core ride-hailing segment. The €270 million investment deepens Uber’s footprint in European food delivery, a region where category penetration still has meaningful room to expand.

The risks are not trivial. Waymo has a multi-year head start in commercial robotaxi operations. Tesla’s ambitions in the space remain a genuine wildcard.

At 14.22 times NTM EV/EBITDA, the stock is not priced for distress. And the AV capital commitment, however milestone-contingent, represents a real shift in how much capital Uber needs to deploy to stay competitive.

See how Uber performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $78.38

- TIKR Model Entry Price: $76.48

- Mid-Case Target: ~$210

- Potential Total Return: ~174%

- Mid-Case IRR: ~21% per year

See analysts’ growth forecasts and price targets for Uber stock (It’s free!) >>>

The TIKR mid-case model targets approximately $210 by December 31, 2030, implying a potential total return of around 174% and an annualized IRR of around 21% from the model entry price of $76.48.

Two revenue drivers underpin that projection. The mobility segment generated $29,670 million in FY2025 and is expected to sustain high-teens growth as U.S. trip frequency accelerates. Delivery is the faster-growing engine: gross bookings crossed a $100 billion annualized run-rate in Q4 2025, and Uber One membership — which drives higher-frequency, higher-margin trips — reached over 46 million members globally. Together, TIKR consensus estimates project total revenue growing from $52,017 million in FY2025 to approximately $89,174 million by FY2030, roughly 11% compound annual growth over that five-year window.

The margin driver is operating leverage from advertising and membership. Advertising crossed a $2 billion annualized run-rate in FY2025, up over 50% year-over-year. EBITDA margins were 16.8% in FY2025; TIKR consensus projects them expanding toward around 23% by FY2030.

The downside scenario is a world where the $10 billion AV commitment generates returns that lag expectations, the market re-rates Uber toward a capital-intensive transportation multiple, and margin expansion stalls. Even in that case, the core platform’s free cash flow generation, projected at $10,390 million in FY2026, provides meaningful earnings support.

Conclusion

Watch Uber’s adjusted EBITDA margin as a percentage of gross bookings at the Q1 2026 earnings report, expected in early May 2026. In Q4 2025, that figure came in at 4.6% of gross bookings, up 40 basis points year-over-year. Continued expansion in Q1 confirms the operating leverage thesis is intact alongside the AV investment ramp. A compression would validate the bear concern that the capital shift is costing near-term profitability.

At roughly 23% below its 52-week high, Uber is priced as though the AV bet is a liability. The free cash flow trajectory suggests the market may be getting that wrong.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Uber?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up [Uber], and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track [Uber] alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!