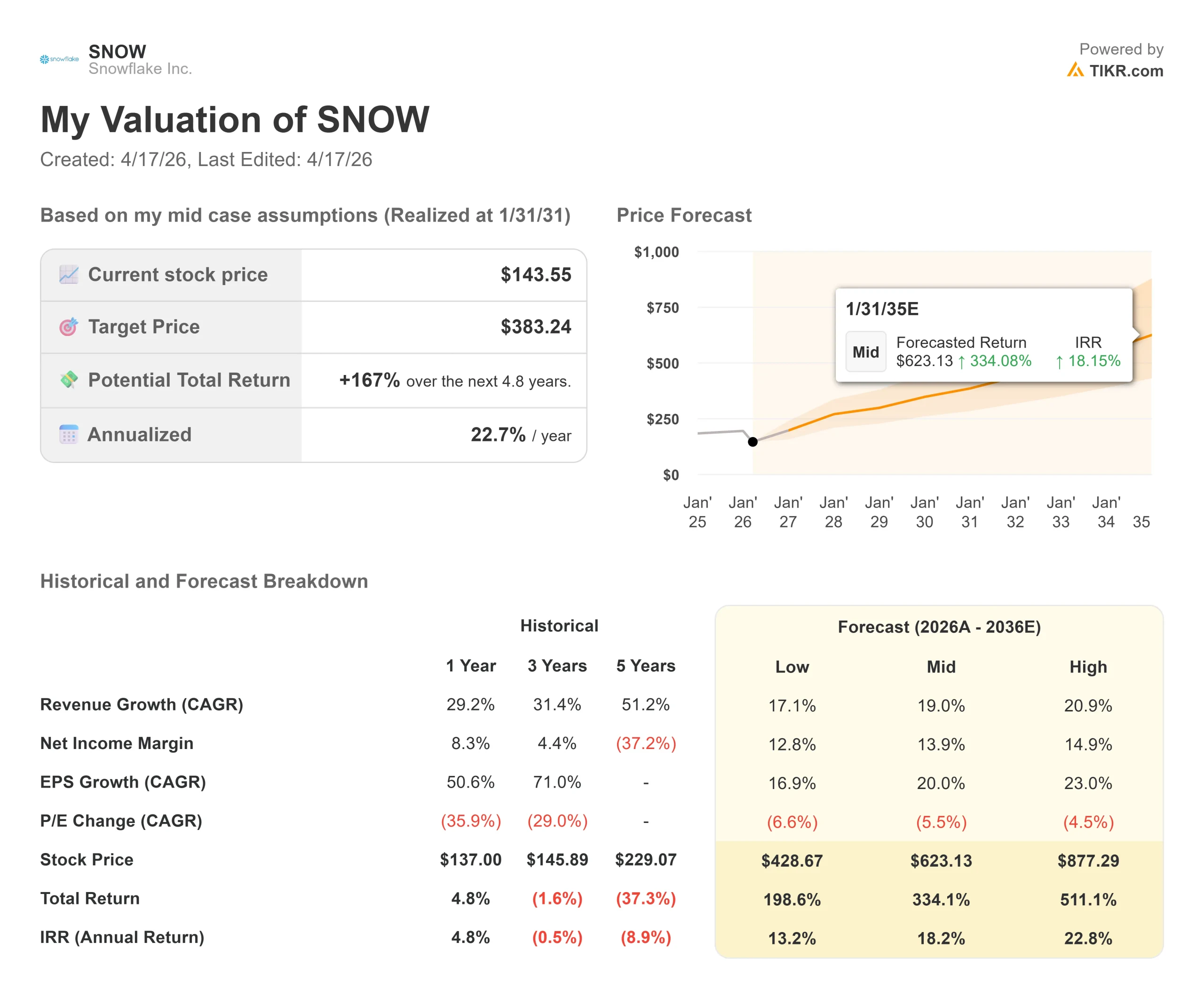

Key Stats for Snowflake Stock

- Current Price: $143.55

- Target Price (Mid): ~$383

- Street Target: ~$237

- Potential Total Return: ~167%

- Annualized IRR: ~23% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Snowflake (SNOW) has been one of the hardest-hit names in cloud software this year. The stock has fallen nearly 49% from its 52-week high of $280.67, touching a max drawdown of 56.30% on April 10 as a sector-wide repricing dragged high-multiple software names lower.

Bulls point to consistent earnings beats and a growing backlog as evidence that the selloff has overshot. Bears argue that Snowflake’s consumption-based model, where customers pay only for actual usage rather than a fixed subscription, makes it unusually vulnerable to enterprise budget cuts, and that AI-native competitors are beginning to threaten its pricing power.

The most recent pressure point came this week. On April 15, KeyBanc analyst Eric Heath cut his price target from $235 to $200 while maintaining an Overweight rating, citing channel checks showing 20% of partners were already redirecting budgets toward AI-native alternatives. Truist cut its target from $175 to $125 the same day. Evercore ISI trimmed its target from $225 to $200 on April 14. The stock fell roughly 9% on April 10, then partially recovered.

Those cuts came after a strong Q4. On February 25, Snowflake reported product revenue of $1.23 billion, up 30% year over year, alongside remaining performance obligations (RPO, or contracted future revenue) of $9.77 billion, up 42% for the second consecutive quarter of acceleration. The stock rose 2.28% on the day.

In Snowflake’s investor relations materials, CEO Sridhar Ramaswamy said: “Snowflake delivered another strong quarter with product revenue of $1.23 billion, up 30% year-over-year, and remaining performance obligations totaling $9.77 billion, up 42% year-over-year. Snowflake sits at the center of the enterprise AI revolution. Now, we’re activating world-class agentic capabilities on top of that platform.”

The bear case has never really been about execution. It is about what happens next.

See historical and forward estimates for Snowflake stock (It’s free!) >>>

Is Visa Undervalued Today?

The valuation reset has been severe. Snowflake’s forward revenue multiple (enterprise value divided by next twelve months’ expected revenue) fell from roughly 18x last October to 8x today, its lowest level since the post-IPO period.

That compression alone does not make the stock cheap, but it changes the entry point significantly.

The business is still expanding at a meaningful pace. LTM free cash flow reached $1.12 billion in fiscal 2026, and management guided for a roughly 23% free cash flow margin in fiscal 2027. Customer expansion at the top end is the clearest sign of platform health: 733 customers now spend over $1 million annually, up 27% year over year, and 56 customers surpassed $10 million in trailing spend, up 56%.

Snowflake also closed the largest deal in its history in Q4, a $400 million-plus contract with an existing financial services customer. The $9.77 billion RPO reflects those commitments.

The AI buildout adds a longer-term layer. More than 9,100 accounts used Snowflake AI features by Q4, and Snowflake Intelligence, the company’s agentic AI product, reached over 2,500 accounts within its first three months. Net revenue retention of 125% means existing customers are, on average, spending 25% more than they did a year ago. Those are not numbers that describe a platform losing the competitive battle.

The risks are real. The 20% of channel partners already shifting budgets to AI-native tools is the most important number to track over the next two quarters. A $1.33 billion GAAP operating loss in fiscal 2026 means profitability on a reported basis remains distant. And a federal securities class action with a lead plaintiff deadline of April 27 alleges that certain former executives failed to disclose how product efficiency gains, Iceberg Tables, and tiered storage pricing would pressure revenue growth, covering the period June 2023 through February 2024.

These are allegations, not findings, and Snowflake has not admitted wrongdoing.

See how Snowflake performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $143.55

- Target Price (Mid): ~$383

- Potential Total Return: ~167%

- Annualized IRR: ~23% / year

See analysts’ growth forecasts and price targets for Snowflake stock (It’s free!) >>>

The TIKR mid-case model targets approximately $383 by January 31, 2031, implying roughly 167% total return at around 23% annualized. The two primary revenue drivers are continued enterprise AI workload migration onto Snowflake Cortex AI and Snowflake Intelligence, and deepening consumption among the company’s largest customer cohorts. The margin driver is operating leverage as stock-based compensation falls from 34% of revenue today toward a guided 27% in fiscal 2027, with net income margins forecast to expand toward roughly 14% in the mid case on around 19% revenue CAGR.

The high case reaches approximately $877 by the same date, requiring around 21% CAGR. The low case lands near $429, still roughly triple today’s price on around 17% CAGR. All three scenarios produce a positive total return from the current entry price.

The scenario that breaks the model is faster-than-expected competitive displacement. If AI-native platforms capture share beyond the 20% of partners flagged by KeyBanc, Snowflake’s FY2027 product revenue guidance of $5.66 billion becomes harder to hit, and a stock still trading at 52x forward EBITDA has room to fall further.

The next real test is Q1 FY2027 results on May 20, 2026. Watch whether product revenue of $1.262–$1.267 billion is met or beaten, and whether management holds full-year guidance. A beat with stable guidance would be the first clear signal that the drawdown has found a floor.

Conclusion

Snowflake is a high-quality business near multi-year lows, with a $9.77 billion RPO growing 42%, LTM free cash flow of $1.12 billion, and a TIKR mid-case model implying around 167% total return through January 2031. The risks are real: AI-native competition, a consumption model that amplifies spending cycles, GAAP losses, and active litigation. This is not a turnaround thesis. It is a bet that Snowflake’s data governance moat and AI platform hold in a market that has priced in the worst case. May 20 will be the first clear test.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Snowflake?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Snowflake, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snowflake alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Snowflake on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!