Key Stats for Axon Stock

- 52-Week Range: $339 to $886

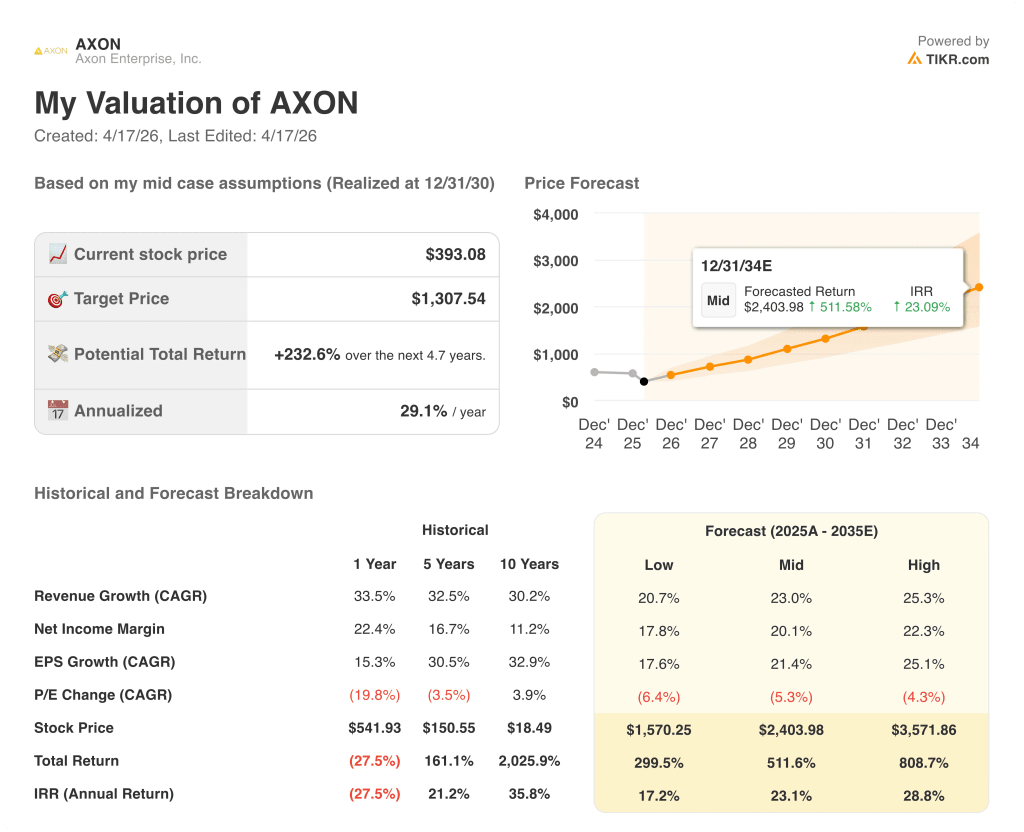

- Current Price: $393

- Street Mean Target: $708

- Street High Target: $825

- TIKR Model Target (Dec. 2030): $1,308

What Happened?

Axon Enterprise (AXON) is the dominant platform in public safety technology, selling body cameras, TASER devices, digital evidence management software, and an expanding suite of AI tools to law enforcement agencies, corrections facilities, and increasingly, enterprise customers worldwide.

Axon closed 2025 with $2.78 billion in revenue, up 33% year-over-year, marking its fourth consecutive year of 30%-plus growth.

Q4 alone delivered $796.7 million in revenue, a 39% increase over the prior-year period, with adjusted EPS of $2.15 against a consensus estimate of $1.60, a 34% beat.

Bookings were the headline: full-year 2025 bookings reached $7.4 billion, up 46% year-over-year, and Q4 bookings accelerated to roughly 50% growth, the strongest quarterly pace in years.

Future contracted bookings now stand at $14.4 billion, up 43%, giving Axon unprecedented revenue visibility heading into 2026 and beyond.

“There is a major opportunity across federal law enforcement for a number of our core products, as well as counter UAS technology,” said Axon President Joshua Isner on the Q4 earnings call.

Axon guided 2026 revenue growth of 27% to 30%, the strongest initial-year outlook the company has ever issued, and introduced a 2028 target of approximately $6 billion in revenue at a 28% adjusted EBITDA margin.

The company also launched three AI products at its Axon Week 2026 user conference on April 7, including Axon Vision for live video alerts, expanded Axon Assistant access, and the cloud-based Axon 911 platform built on the Prepared and Carbyne acquisitions completed in late 2025 and early 2026.

Axon stock has fallen roughly 34% year-to-date despite the earnings blowout, creating a valuation setup that is drawing significant attention across the analyst community.

Wall Street’s Take on AXON Stock

The Q4 earnings beat was not incremental. Axon’s bookings acceleration to 46% growth in a year when management had originally projected high-20s growth signals that the platform is expanding into new markets faster than its own forecasts assumed, resetting the revenue ceiling for 2026 and 2028.

Revenue consensus for 2026 sits at $3.59 billion, a 29% increase, accelerating further to $4.64 billion in 2027 (up 29%) and $6.05 billion in 2028 (up around 30%), the precise year management set as its formal target, implying consensus has essentially ratified the company’s own guidance as the base case.

Of 20 analysts covering Axon stock, 10 rate it a buy and 8 an outperform, with just 2 holds and zero sells; the mean price target sits at $707.96, implying 80% upside from current levels, while TD Cowen, even after trimming its target to $825 citing market volatility and data-privacy concerns, still maintained a buy rating.

Trading at roughly 57x forward earnings against a five-year P/E average that has historically sat in the 80x-to-100x range, Axon stock appears undervalued against a backdrop of accelerating bookings, a $14.4 billion contracted backlog, and consensus revenue growth compounding at around 29% annually through 2028.

The single risk the model cannot absorb is a data-privacy regulatory shock: CFO and COO Brittany Bagley acknowledged on the Q4 call that privacy and data-handling remain the area where a misstep would carry outsized negative consequences, particularly as Axon deepens AI-driven surveillance capabilities.

The catalyst to watch is Q1 2026 revenue guidance confirmation, where management has signaled year-over-year growth consistent with its full-year 27%-to-30% range, and any update on AI Era Plan bookings growth above the $750 million 2025 baseline.

What Does the Valuation Model Say?

TIKR’s mid-case model targets Axon at around $1,308 per share by December 2030, assuming a 23% revenue CAGR and a 20% net income margin, inputs that are notably more conservative than the 33% three-year revenue CAGR the company has already delivered and below the 25.5% adjusted EBITDA margin Axon achieved in 2025.

At $393 with a mid-case IRR of around 23% annually over 4.7 years, the 232% potential return implied by the model reflects an asset being priced as if growth is decelerating when the contracted backlog says the opposite: Axon stock is undervalued relative to the earnings power its bookings trajectory and platform expansion have already locked in.

The Platform Pivot Hinges on Whether 2025 Bookings Momentum Is Structural or a Pull-Forward

Axon enters 2026 with $14.4 billion in future contracted bookings, implying the next two to three years of revenue are largely secured, but the debate is whether 46% bookings growth in 2025 represents a genuine structural acceleration or a surge pulled forward by large corrections and international deployments that compress the 2026 comparison.

What Has to Go Right

- AI Era Plan bookings, which reached $750 million in their first full year of sales, continue scaling as only roughly 30% of existing customers are on premium subscription tiers, leaving substantial upsell runway across the existing base at officer-based ARPU approaching $600

- Federal demand converts: Axon’s federal pipeline is described by management as among the largest opportunities in 2026, driven by immigration enforcement investment and new federal leader Claudia Davidson’s early traction with umbrella contracts already in place

- International cloud adoption accelerates after the two large European cloud deals closed in Q4 2025, as AI product access becomes a forcing function for governments still on on-premise deployments

- Axon 911 (Prepared and Carbyne) gains traction in a 911 infrastructure market that has run on 40-year-old technology, with each new PSAP deployment opening a full platform sale across the Fusus and Axon ecosystem

What Could Go Wrong

- 2026 bookings comparisons are extremely difficult after Q4 2025 growth of roughly 50%, and management declined to provide 2026 bookings guidance, an unusual omission for a company that has beaten its own guidance for multiple consecutive years

- Data-privacy regulatory action targeting AI-driven surveillance could slow enterprise adoption, where Axon Body Mini launches in mid-2026 into commercial environments where privacy scrutiny runs higher than in law enforcement

- Tariff and memory cost headwinds could compress Connected Devices gross margins below the 49.3% Q4 2025 adjusted level, pressuring blended EBITDA margins even as software mix improves

- GAAP EPS of $1.51 in 2025 versus normalized EPS of $6.85 reflects a wide gap between accounting earnings and the economic earnings narrative management is selling, creating valuation vulnerability if the normalization thesis is questioned

Should You Invest in Axon Enterprise, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AXON stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Axon Enterprise, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AXON stock on TIKR for Free →