Key Stats for ADM Stock

- Past-Year-to-Date Performance: 18%

- 52-Week Range: $41 to $70

- Valuation Model Target Price: $71

- Implied Upside: 6%

Value your favorite stocks like Archer-Daniels-Midland Company with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Archer Daniels Midland stock is up about 18% year to date, recently trading near $68 per share as investors repositioned around improving earnings visibility and expectations that 2025 marked a cyclical trough.

The rally reflects growing confidence that profit declines tied to weaker crush margins may be stabilizing heading into 2026.

Shares moved higher after ADM reported Q4 adjusted EPS of $0.87 and issued 2026 adjusted EPS guidance between $3.60 and $4.25, above the $3.43 delivered in 2025.

That guidance signaled a return to earnings growth driven by expected improvement in biofuel policy clarity, ethanol economics, and Nutrition execution, which helped offset concerns about continued softness in Starches and Sweeteners.

Total segment operating profit reached $821 million in the fourth quarter and $3.2 billion for the full year. The company generated $2.7 billion in cash flow from operations before working capital changes and realized a $1.5 billion cash flow benefit from inventory reduction.

Management also achieved about $200 million in cost savings through portfolio optimization initiatives and maintained capital discipline with its 376th consecutive quarterly dividend.

Institutional activity has also been active. CIBC World Market increased its stake by 229.3% in the third quarter, Allianz Asset Management raised its position by 45.8%, and Principal Financial Group added 5.7%, while LSV Asset Management and Alps Advisors trimmed their holdings.

Director David Mcatee II purchased 7,500 shares at $64.90 for about $486,750, signaling insider conviction.

Institutional ownership remains near 78%, and analyst sentiment remains cautious overall, with consensus ratings skewed toward Hold and Sell despite the stock’s year-to-date advance.

See analysts’ growth forecasts and price targets for Archer-Daniels-Midland Company (It’s free) >>>

Is ADM Undervalued?

Under valuation assumptions, the stock is modeled using:

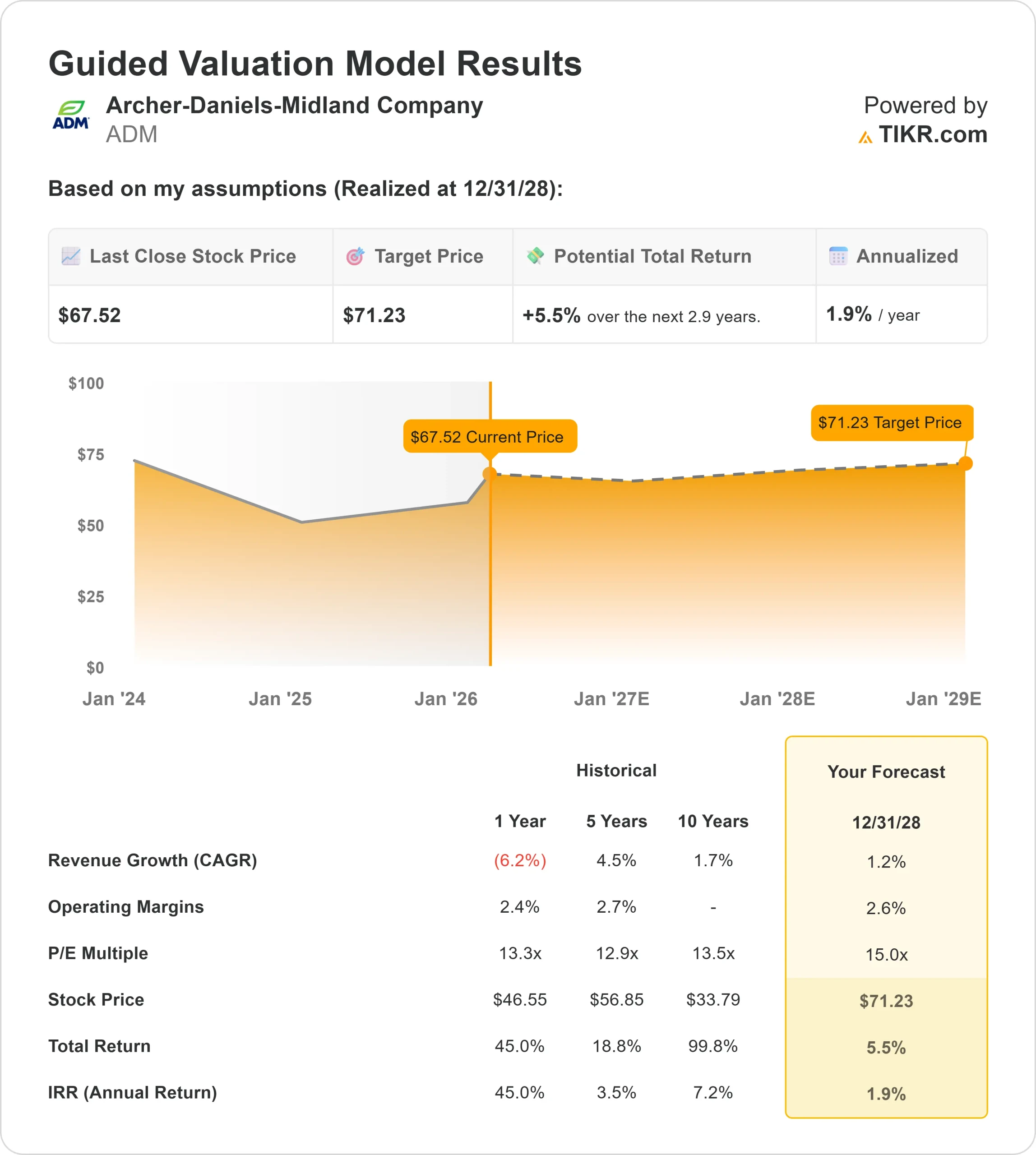

- Revenue Growth (CAGR): 1.2%

- Operating Margins: 2.6%

- Exit P/E Multiple: 15x

ADM’s revenue base has normalized following the post-2022 commodity surge, and forward projections imply low single-digit growth rather than reacceleration.

That means future returns depend primarily on operating leverage and margin expansion rather than revenue growth.

Crush margins remain the most important earnings driver in 2026. Biofuel policy clarity, renewable diesel demand, and global vegetable oil flows could meaningfully influence processing spreads.

Even modest improvement in cash crush margins can drive disproportionate gains in operating income given ADM’s scale.

Ethanol economics are another key lever. Export demand, mandated blending markets, and potential regulatory incentives could offset continued softness in liquid sweeteners.

Nutrition provides incremental support through strength in Flavors, recovery in Specialty Ingredients, and margin expansion in Animal Nutrition.

The company ended 2025 with a leverage ratio of 1.9x and expects capital expenditures of $1.3 billion to $1.5 billion in 2026, supporting investment in enhanced nutrition, biosolutions, and decarbonization initiatives.

Based on these inputs, the valuation model estimates a target price of $71.23, implying about 5.5% total upside over roughly 2.9 years, or 1.9% annually.

At current levels near $68 per share, ADM appears slightly overvalued under conservative assumptions.

Continued upside in 2026 will likely require sustained improvement in crush margins and biofuel-driven demand translating into higher cash margins rather than revenue growth alone.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>