Key Takeaways:

- Earnings Miss on Guidance: IQVIA reported Q4 2025 adjusted EPS of $3.42, beating estimates by $0.02, yet guided full-year 2026 adjusted EPS of $12.55–$12.85 below the $12.95 consensus, with $80M in higher interest expenses from 2025 financing activities driving the shortfall and sending shares down 8% on February 5, 2026.

- Obesity Research Collaboration: IQVIA announced a strategic partnership with Duke Clinical Research Institute on February 10, 2026, covering 56 countries and 3,000+ sites, leveraging IQVIA’s track record of supporting 120+ obesity trials and every FDA-approved GLP-1 therapy, directly targeting the fastest-growing segment of clinical research spending.

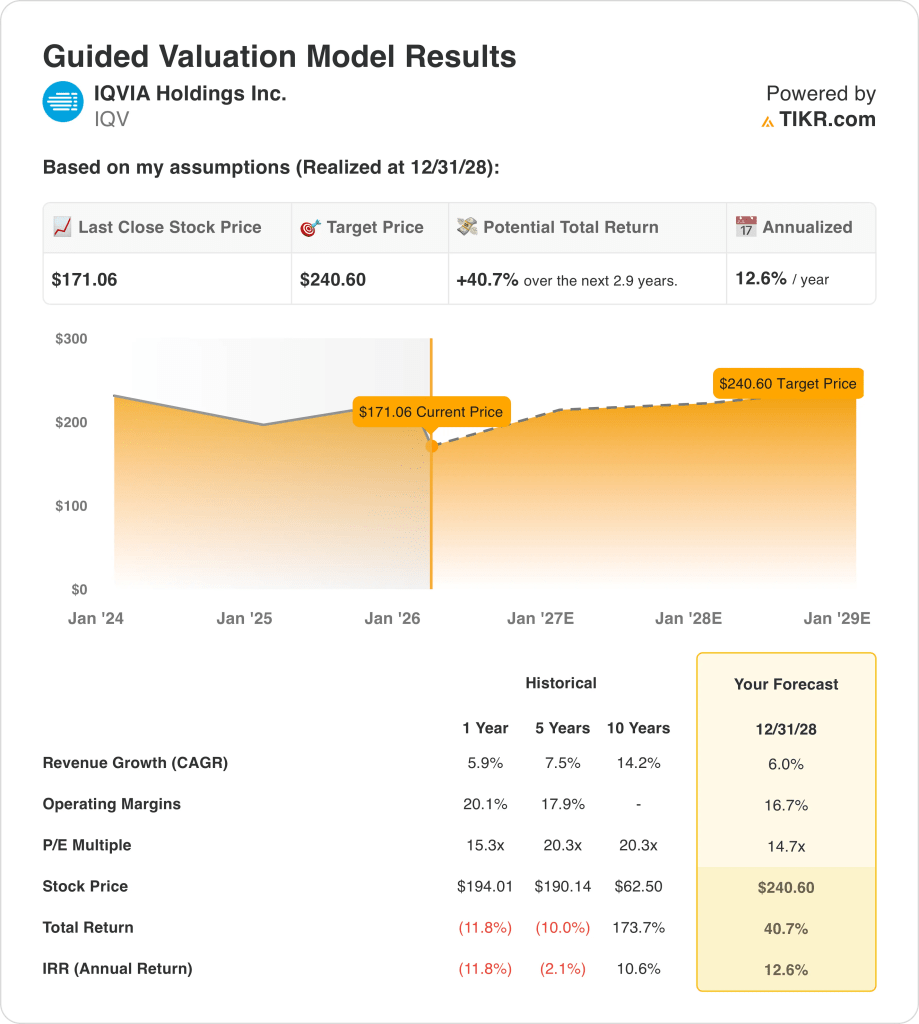

- Price Target: Based on 6% revenue growth, 17% operating margins, and a 15x exit multiple, IQVIA stock could reach $241 by December 2028 from $171 today.

- Return Profile: IQVIA implies 41% total upside from $171 to $241 over 2.9 years, equating to a 13% annualized return supported by $1.244 billion in full-year 2025 share repurchases at an average price of $159 per share.

Breaking Down the Case for IQVIA

February 5, IQVIA (IQV) reported Q4 2025 revenue of $4.36B, beating estimates by $120M, while guiding 2026 adjusted EPS of $12.55–$12.85 below the $12.95 consensus, triggering an 8% single-day stock decline driven by $80M in higher interest expenses.

Full-year 2025 revenue reached $16.31B at 5.9% growth, with R&DS backlog hitting a record $32.7B and next 12-month backlog revenue of $8.3B anchoring near-term revenue visibility despite muted top-line acceleration.

Operating income of $2.30B held at 14.1% margins as $1.99B in SG&A and $1.14B in D&A consumed the majority of $5.43B in gross profit generated at 33.3% margins across the global clinical and commercial platform.

CEO Ari Bousbib stated on the Q4 2025 earnings call that “IQVIA has the largest proprietary healthcare information assets in the world and is the foundation of our value to clients,” directly challenging analyst concerns that generative AI would displace the company’s clinical research and analytics services.

On February 10, 2026, IQVIA announced a strategic collaboration with Duke Clinical Research Institute targeting obesity and cardiometabolic trials across 56 countries, backed by 120+ prior obesity trials and operational support for every FDA-approved GLP-1 therapy.

The board repurchased $1.244B in shares during 2025 at an average price of $159, alongside a Cedar Gate Technologies acquisition adding approximately $140M in annual revenue and payer analytics capabilities to the Commercial Solutions segment.

The investment tension centers on whether IQVIA converts its record $32.7B R&DS backlog and 150+ deployed AI agents into accelerating revenue growth above 6% annually, against a backdrop of $171 current stock price, 16x forward P/E trading below the 5-year average of 19.8x, and 13% projected annualized returns through December 2028 that require margin recovery to 17% without a second year of interest expense headwinds materializing.

What the Model Says for IQV Stock

IQVIA’s $80M interest expense headwind from 2025 financing activities directly pressured 2026 EPS guidance below the $12.95 consensus, while the record $32.7B R&DS backlog and improving RFP flow establish the revenue foundation the model requires to reach $241.

The model’s assumption of 6% revenue growth, 17% operating margins, and a 15x exit multiple produces a target price of $241 by December 2028, with revenue growth in line with the 5.9% delivered last fiscal year, margins above the current 14.1% operating level requiring recovery, and the exit multiple below the 5-year historical average of 20x.

The market assumption for the forward P/E as of February 18, 2026 stands at 13x, compressed from 18x at December 31, 2025 and 13x at June 30, 2025, driven by the AI disruption selloff that wiped $830B in software and services market value, and the model’s 15x exit sits above the current depressed market assumption, requiring modest re-rating from current levels.

The street mean target stands at $243 as of February 18, 2026, a target-to-price ratio of 142%, expanding sharply from 113% at December 31, 2025, while Buy and Outperform recommendations hold at 19 combined versus 22 at December 31, 2024, showing stable conviction that the post-earnings decline has created a gap between fundamentals and price.

The CFO transition from Ron Bruehlman to Mike Fedock, effective in 2026, introduces communication and capital allocation continuity risk during a period when investor confidence in the AI strategy requires consistent and credible financial messaging across quarterly earnings calls.

This is a Buy signal of marginal quality: the 13% annualized return clears the 10% hurdle, the 142% street target-to-price ratio confirms analyst conviction that the stock is mispriced, and the model’s 15x exit multiple sits modestly above a 13x market assumption that requires only partial re-rating, though operating margin recovery from 14% to 17% and CFO transition risk prevent a high-conviction designation.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for IQV stock:

1. Revenue Growth: 6%

IQV stock delivered 5.9% revenue growth in fiscal 2025 to $16.31B as R&DS bookings reached a record $32.7B backlog and CSMS grew 9.7%, yet the 22.1% growth delivered in fiscal 2021 reflected pandemic-era demand that no longer exists as a structural support.

The fiscal 2026 estimate of $17.23B reflects 5.6% growth, in line with the model’s 6.0% assumption, as Commercial Solutions targets 7%–9% growth and R&DS targets 4% growth, yet $80M in higher interest expenses limits how much revenue growth converts to net income expansion.

The 6.0% model’s assumption through December 2028 rests on R&DS backlog converting at the $8.3B next 12-month run rate, the DCRI obesity collaboration across 56 countries and 3,000+ sites generating incremental clinical trial mandates, and biotech funding sustaining its 2025 recovery without a renewed post-pandemic funding freeze.

Any failure in R&DS backlog conversion, combined with a renewed slowdown in biotech funding and cancellations above the normal range seen in Q4 2025, compounds revenue shortfalls faster than the 150+ deployed AI agents and $1.244B repurchase program can absorb, as each 1% miss on $17B of forward revenue represents $170M in lost top-line that directly reduces the earnings base the 15x exit multiple capitalizes.

This sits on par with the 1-year revenue growth of 5.9%, as the model embeds incremental contribution from the Cedar Gate acquisition and the DCRI obesity collaboration, and sustaining 6.0% requires R&DS book-to-bill to hold above 1.18 while cancellations remain within the normal range through 2028.

2. Operating Margins: 16.7%

IQV stock reported 14.1% operating margins in fiscal 2025 on $2.30B in operating income, contracting from 14.8% in fiscal 2024, as gross profit of $5.43B at 33.3% margins funded $1.99B in SG&A and $1.14B in D&A, leaving less than 15 cents of every revenue dollar as operating income.

The 16.7% model’s assumption sits above fiscal 2025’s 14.1% level, consistent with the fiscal 2026 EBIT margin estimate of 15.5%, as SG&A at $1.99B held essentially flat year-over-year and pass-through growth moderation in 2026 removes the gross margin headwind that compressed Q4 results.

Reaching 16.7% by December 2028 requires SG&A to grow materially slower than the 6.0% revenue pace, the CFO transition from Bruehlman to Fedock to proceed without disruption to the finance organization’s cost discipline, and interest expense of $760M in 2026 to moderate in 2027 and 2028 as refinancing activity completes.

The market assumption for the forward P/E as of February 18, 2026 stands at 13x, compressed from 18x at December 31, 2025, as the AI disruption selloff that wiped $830B in software and services market value collapsed investor willingness to pay above 15x, creating a sentiment discount that the model’s 16.7% margin assumption partially addresses but does not fully resolve at current prices.

Any failure to moderate pass-through costs, combined with Cedar Gate integration expenses and CFO transition overhead, keeps operating margins pinned near the fiscal 2025 level of 14.1% rather than recovering toward 16.7%, and each 100 basis point shortfall on $17B of revenue represents $170M in missed operating income.

This sits above the 1-year operating margin of 13.4%, as the model embeds pass-through normalization, SG&A productivity from 150+ deployed AI agents, and the elimination of the one-time EBIT compression that drove fiscal 2025’s 29.6% EBIT decline, and reaching 16.7% requires all three cost lines to improve simultaneously without new financing headwinds materializing.

3. Exit P/E Multiple: 14.7x

The 14.7x exit multiple capitalizes IQV stock’s normalized net income at December 2028 under conditions of 6.0% revenue growth and 16.7% operating margins, treating the multiple as a terminal earnings anchor for a global clinical research and healthcare data platform with proprietary data assets that cannot be replicated by general-purpose AI models.

The model already embeds 16.7% operating margin recovery and 6.0% revenue growth through December 2028, meaning the 14.7x exit multiple does not require additional credit for AI agent monetization or the DCRI obesity collaboration, as both are absorbed in the earnings trajectory and a higher multiple would double-count growth already in the model.

The market assumption for the forward P/E as of February 18, 2026 stands at 13x, compressed from 18x at December 31, 2025, as the six-day AI disruption selloff wiped $830B in software and services market value and collapsed investor willingness to pay above 15x, and the model’s 14.7x exit sits above the current 13x market assumption, requiring modest sentiment recovery as AI disruption fears moderate.

If operating margins fail to recover from 14.1% toward the 16.7% assumption, or if the CFO transition disrupts 2026 earnings communication and investor confidence, earnings compression pushes the sustainable multiple toward the current 13x market assumption rather than sustaining near 15x, and the $241 price target compresses toward the 1-year historical stock price of $194.

This sits below the 1-year historical P/E of 15.3x, as the AI disruption fears and $80M interest expense headwind justify a valuation discount versus the trailing year multiple, and sustaining 14.7x through December 2028 requires both margin recovery to 16.7% and AI disruption concerns to moderate without a second wave of sector-wide sentiment compression materializing.

What Happens If Things Go Better or Worse?

IQV stock results through 2030 rest on R&DS backlog conversion, AI disruption sentiment recovery, and operating margin normalization after a year of interest expense headwinds.

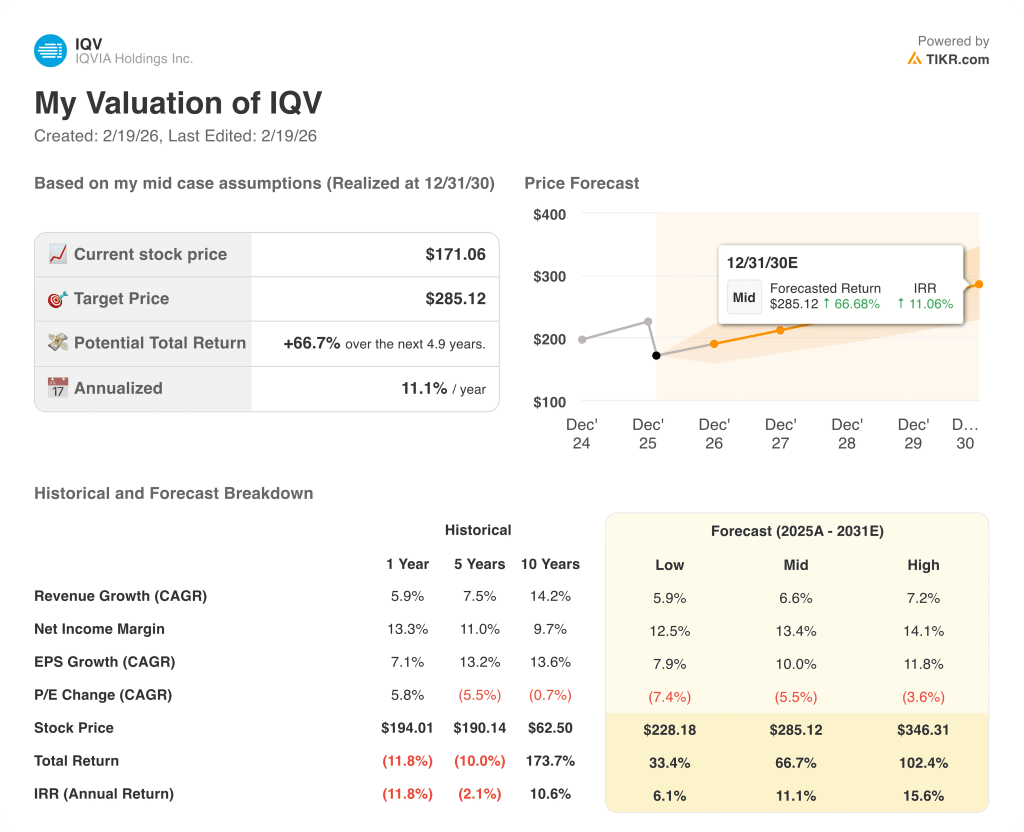

- Low Case: If biotech funding stalls and AI concerns continue pressuring clinical trial outsourcing demand, revenue grows around 5.9% and net income margins stay near 12.5% → 6.1% annualized return.

- Mid Case: With R&DS backlog converting at its $8.3B run rate and the DCRI obesity collaboration generating incremental mandates, revenue grows near 6.6% and margins improve toward 13.4% → 11.1% annualized return.

- High Case: If large pharma AI-enabled trial efficiency drives accelerated outsourcing and Commercial Solutions captures enterprise-wide partnerships, revenue reaches around 7.2% and margins approach 14.1% → 15.6% annualized return.

How Much Upside Does IQVIA Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!