Key Takeaways:

- Weak Q4 Guidance: Doximity projected Q4 FY2026 revenue of $143M–$144M, representing only 4% growth and missing Wall Street’s $148M estimate, as 16 of the top 20 pharma companies delayed upfront budget commitments due to MFN agreements signed with the White House in late December 2025.

- Record AI Adoption: Doximity surpassed 300,000 unique prescriber users on DocsGPT in its first full quarter post-Pathway acquisition, with physicians querying the platform an average of 4 times per week, while 100+ health systems covering 180,000 clinicians cleared privacy and AI committees and purchased the full AI suite.

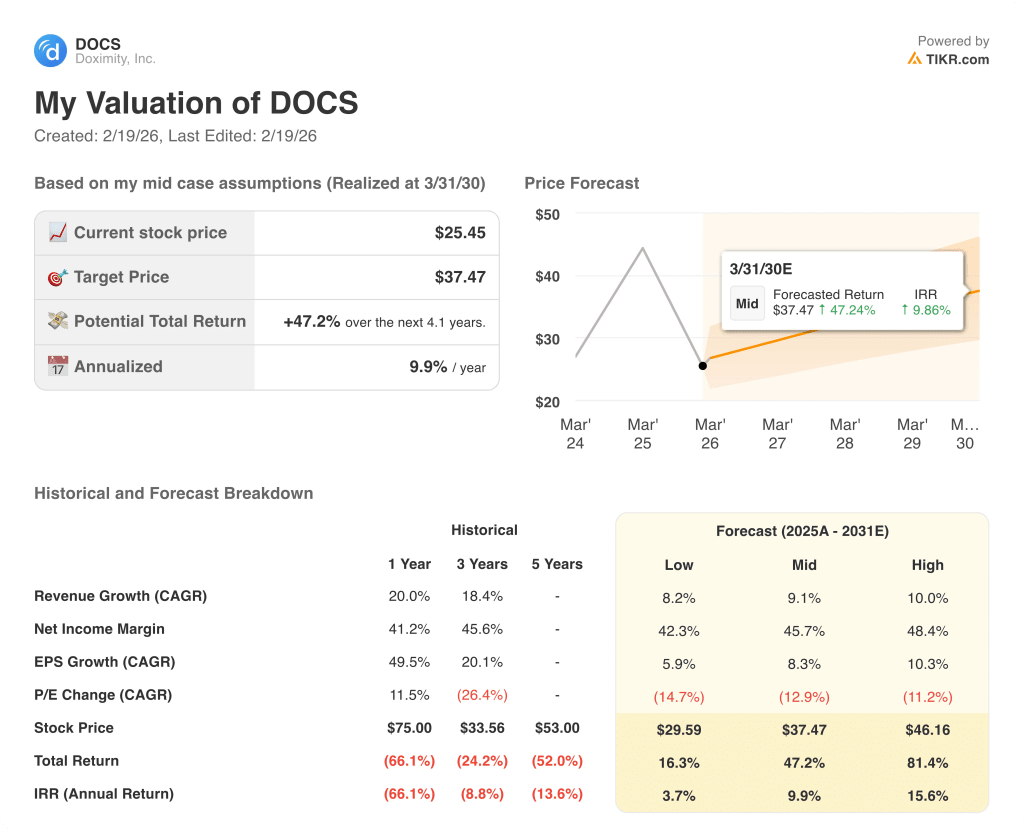

- Price Target: Based on 10% revenue growth, 53% operating margins, and a 16x exit P/E multiple, Doximity stock could reach $33.16 by March 2028 from $25.45 today.

- Return Profile: Doximity implies 30% total upside from $25.45 to $33.16 over 2.1 years, equating to a 13% annualized return supported by a newly authorized $500 million open-ended share repurchase program approved February 5, 2026.

Breaking Down the Case for Doximity, Inc.

In February, Doximity (DOCS) reported Q3 FY2026 revenue of $185M, beating estimates by $2.9M, while simultaneously guiding Q4 revenue to $143M–$144M, triggering a 30% single-day stock decline to $23.

Full-year FY2026 guidance was updated to $642.5M–$643.5M at 13% growth, supported by 90%+ gross margins and a trailing net revenue retention rate of 112% across its 126 largest customers.

Operating income reached $240M on an LTM basis at 37.5% operating margins, even as R&D spending climbed to $120M annually to fund AI infrastructure and the PeerCheck physician review program.

Meanwhile, on February 5, Doximity Dialer was named the #1 Telehealth Video Conferencing Platform in the 2026 Best in KLAS Report for the fifth consecutive year, earning A+ ratings in culture, loyalty, and value, with clinicians completing more than 300,000 calls each workday and a single-day record of 720,000 HIPAA-compliant calls during January’s winter storms.

CEO Jeff Tangney stated on the Q3 2025 earnings call that “in our first full quarter after acquiring something and growing with it, I don’t think any other company could have grown into this market that fast,” referencing 300,000 AI users reached within one quarter of the Pathway Medical acquisition.

The board simultaneously authorized a new $500M share repurchase program with no expiration date, following $196.8M in repurchases during Q3 alone against a cash balance of $735M.

January 2026 pharma bookings growth was described as the highest since the company’s IPO, driven by delayed December signings from 16 of the top 20 pharma companies that had not finalized 2026 budgets amid late-year MFN negotiations with the White House.

The investment tension centers on whether Doximity converts January’s record bookings momentum and uncommitted pharma budgets into double-digit revenue growth by year-end 2026, against a backdrop of $25.45 current stock price, zero AI revenue in guidance, and 13% projected annualized returns through March 2028 that require sustained 10% growth and 53% operating margins without further pharma budget delays materializing.

What the Model Says for DOCS Stock

Doximity’s Q4 FY2026 revenue guidance of $143M–$144M, representing only 4% growth, reflects pharma budget delays from MFN negotiations, with zero AI revenue included in guidance despite 300,000 active physician users on DocsGPT.

The model’s assumption of 10% revenue growth, 53% operating margins, and a 16x exit P/E produces a target price of $33.16 by March 2028, with revenue growth conservative versus the 20% delivered last fiscal year, margins in line with the 54% LTM EBIT margin, and the exit multiple aggressive versus the current market assumption of 16x.

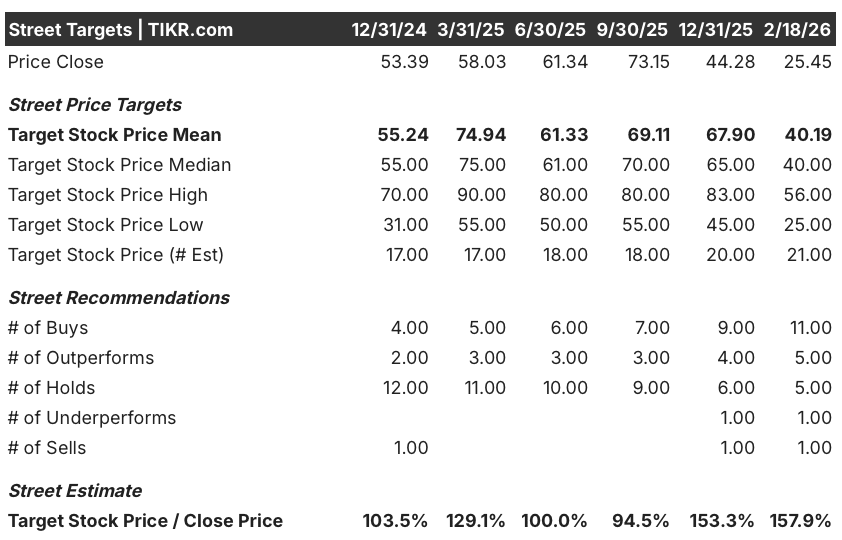

The market assumption currently sits at 16x forward P/E as of February 18, 2026, compressed sharply from 48x at September 30, 2025 and 42x a year prior, driven by the 30% single-day stock decline following weak Q4 guidance, meaning the model’s 16x exit multiple assumes no re-rating from current depressed levels.

The street mean target stands at $40.19 as of February 18, 2026, a target-to-price ratio of 158%, up from 153% at December 31, 2025 and sharply higher than the 100% ratio at June 30, 2025, while Buy and Outperform recommendations have risen to 16 combined versus 7 at December 31, 2026, signaling rising analyst conviction that the post-earnings selloff is overdone.

The model delivers 30% total upside from $25.45 to $33.16 over 2.1 years at a 13% annualized return, clearing the 10% equity hurdle rate, supported by the $500M repurchase program, though zero AI revenue in guidance and a 4% Q4 growth rate represent near-term constraints on that return.

The CFO Anna Bryson’s medical leave, resulting in interim financial leadership under board member Tim Cabral, introduces execution and communication risk during a period when pharma clients are renegotiating budgets and AI commercialization decisions require clear strategic direction from finance.

This is a Buy signal of marginal quality: the 13% annualized return clears the 10% hurdle, the street’s 158% target-to-price ratio and rising Buy count confirm analyst conviction, and the model’s 16x exit multiple requires no valuation re-rating from current levels, though near-term execution risk from delayed pharma budgets and interim CFO leadership prevent a high-conviction designation.

The model delivers a 13% annualized return against a 10% equity hurdle rate, producing a marginal Buy signal reinforced by a 158% street target-to-price ratio and 16 combined Buy and Outperform ratings, tempered by interim CFO leadership, zero AI revenue in guidance, and a forward P/E already compressed to 16x at the model’s exit level.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Doximity stock:

1. Revenue Growth: 10.4%

DOCS stock delivered 20% revenue growth in fiscal 2025 to $570M, driven by record net revenue retention of 112% and a strong upfront selling season, yet the MFN-driven pharma budget delays that produced only 4% Q4 FY2026 guidance eliminated that seasonal structural support.

The fiscal 2026 estimate of $643M reflects 13% growth at the full-year midpoint, above the model’s 10.4% assumption through March 2028, as the top 20 pharma customer cohort growing at 117% NRR provides the base, yet delayed upfront commitments constrain how quickly that retention converts to recognized revenue.

The 10.4% model’s assumption through March 2028 rests on uncommitted pharma budgets releasing during the mid-year upsell season, AI commercial products reaching market in calendar 2026 and capturing innovation budgets, and the market growing at roughly 5% annually while DOCS takes share as it has every year since going public.

Any failure in pharma budget release timing, combined with AI commercialization delays beyond calendar 2026 and continued MFN-related planning uncertainty, compounds revenue shortfalls faster than the 112% net revenue retention rate can absorb, as each 1% miss on the $643M revenue base represents $6M in lost top-line that flows directly into the earnings base the exit multiple capitalizes.

This sits below the 1-year revenue growth of 20%, as the structural post-upfront-season slowdown evident in 4% Q4 guidance removes the seasonal tailwind that inflated fiscal 2025, and sustaining 10.4% requires pharma innovation budgets to unlock mid-year without a second wave of policy-driven spending freezes.

2. Operating Margins: 53.1%

DOCS stock reported 40.5% operating margins in fiscal 2025 on $230M in operating income, expanding from 36.3% in fiscal 2024, as gross margins held above 89% and R&D spending of $90M remained contained relative to the growing revenue base.

The 53.1% model’s assumption sits in line with the current 53.9% LTM EBIT margin, consistent with the forward EBIT margin estimate of 54.1% for fiscal 2026, as AI infrastructure investment compressed non-GAAP gross margin by 200 basis points year-over-year to 91%, creating a structural cost layer not present in prior periods.

Reaching 53.1% by March 2028 requires AI infrastructure unit costs to decline as usage scales, PeerCheck editorial investment to plateau after the 10,000 expert reviewer milestone, and SG&A at $220M annually to grow no faster than the 10.4% revenue assumption without additional talent war compensation escalation.

The market assumption for the forward P/E as of February 18, 2026 stands at 16x, compressed sharply from 48x at September 30, 2025, as the 30% single-day stock decline following weak Q4 guidance collapsed investor willingness to pay above 20x, and the model’s 53.1% margin assumption sits above the current market pricing that implies significant operational skepticism.

Any acceleration in AI infrastructure costs beyond current usage levels, combined with CFO medical leave creating finance team execution risk and pharma budget uncertainty dragging into the mid-year upsell season, compresses operating margins back toward the 3-year average of 47.9%, as each 100 basis point margin shortfall on $700M of revenue represents $7M in missed operating income that directly reduces the earnings base the 16x exit multiple capitalizes.

This sits below the 1-year operating margin of 53.9%, as AI infrastructure investment compressed gross margins by 200 basis points year-over-year and the model embeds that cost normalization taking time to flow through, and reaching 53.1% requires infrastructure unit costs to decline as usage scales without additional PeerCheck or talent investment exceeding the revenue growth pace.

3. Exit P/E Multiple: 16.4x

The 16.4x exit multiple capitalizes DOCS stock’s normalized net income at March 2028 under conditions of 10.4% revenue growth and 53.1% operating margins, treating the multiple as a terminal earnings anchor for a high-margin physician platform with 85% U.S. physician penetration and no direct structural competitor.

The model already embeds 53.1% operating margin expansion and 10.4% revenue growth through March 2028, meaning the 16.4x exit multiple does not require additional credit for AI commercialization upside or pharma market share gains, as both are absorbed in the earnings trajectory and a higher multiple would double-count growth already in the model.

The market assumption for the forward P/E as of February 18, 2026 stands at 16x, compressed from 48x at September 30, 2025 and 43x a year prior, as the weak Q4 revenue guidance and MFN-driven pharma uncertainty collapsed the premium investors previously assigned to DOCS’s high-margin subscription model, and the model’s 16.4x exit sits essentially in line with the current depressed market assumption.

If AI commercialization stalls beyond fiscal 2027 or pharma budget uncertainty extends into a second annual selling season, earnings compression below the 53.1% margin assumption pushes the sustainable multiple toward 11x, the current NTM EV/EBITDA market assumption, rather than sustaining near 16x, and the $33.16 price target compresses toward the $23 post-earnings low.

This sits below the 1-year historical P/E of 38.7x, as the post-guidance selloff collapsed the premium once assigned to DOCS’s high-margin platform and zero AI revenue in current guidance removes the growth optionality that historically supported above-40x multiples, and sustaining even 16.4x through March 2028 requires AI products to reach market in calendar 2026 without further pharma budget disruption materializing.

What Happens If Things Go Better or Worse?

Doximity stock outcomes rest on pharma budget release timing, AI commercialization execution, and physician platform engagement through March 2030.

- Low Case: If pharma budget uncertainty persists and AI products reach market late, revenue grows around 8.2% and net income margins stay near 42.3% → 3.7% annualized return.

- Mid Case: With uncommitted pharma budgets releasing mid-year and AI commercial products launching in calendar 2026, revenue grows near 9.1% and margins improve toward 45.7% → 9.9% annualized return.

- High Case: If AI search and member engagement products capture innovation budgets ahead of schedule and pharma digital spending accelerates, revenue reaches around 10% and margins approach 48.4% → 15.6% annualized return.

How Much Upside Does Doximity Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!