Key Takeaways:

- Talc Litigation Escalation: Johnson & Johnson lost its second consecutive talc trial on February 13, 2026, with a Philadelphia jury awarding $250,000 to the Gayle Emerson estate, following a $40 million California verdict in December 2025, as the company now faces over 67,000 active lawsuits after three failed bankruptcy attempts and a January 2026 federal ruling allowing plaintiffs’ expert testimony linking baby powder to ovarian cancer.

- FDA Breakthrough Designation: Johnson & Johnson received FDA Breakthrough Therapy Designation on February 18, 2026, for RYBREVANT FASPRO as monotherapy in HPV-unrelated head and neck squamous cell carcinoma, adding to a pipeline that secured 51 regulatory approvals and 32 submissions in 2025 alone, with oncology sales already growing 21% operationally and DARZALEX crossing $14 billion in annual revenue.

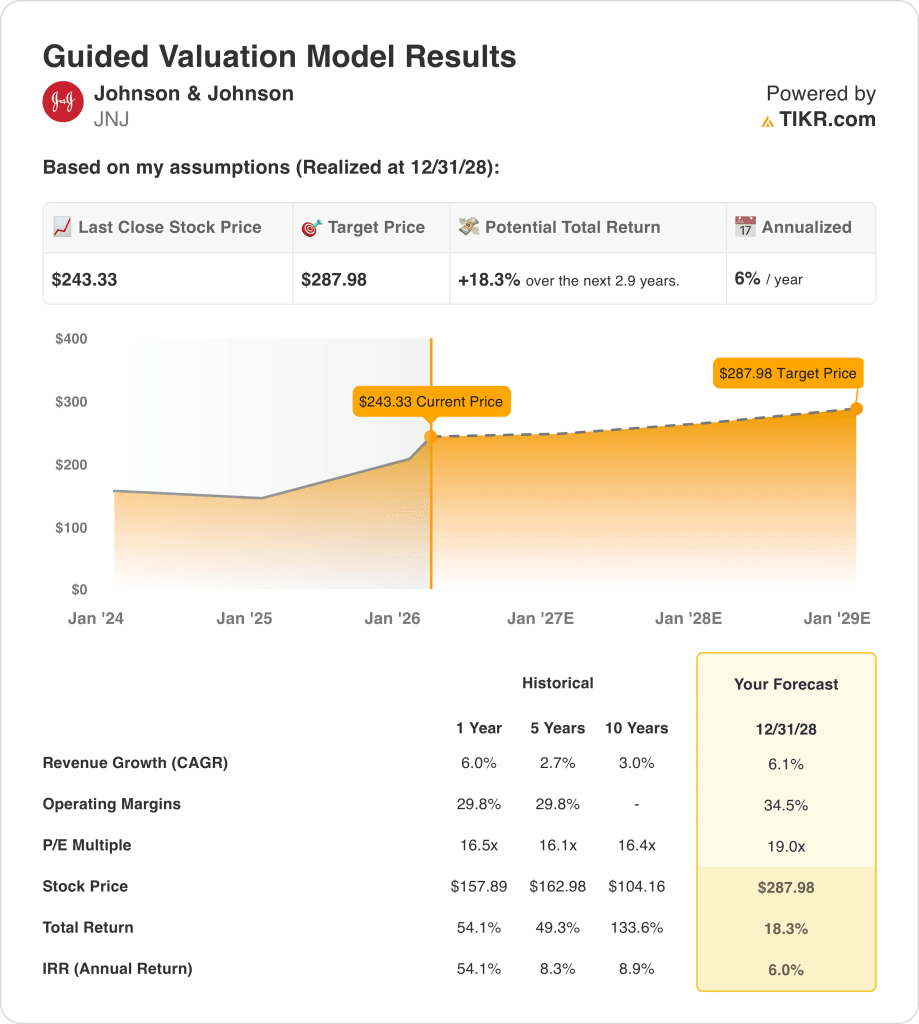

- Price Target: Based on 6% revenue growth, 34% operating margins, and a 19x exit multiple, Johnson & Johnson stock could reach $288 by December 2028 from $243 today.

- Return Profile: Johnson & Johnson implies 18% total upside from $243 to $288 over 2.9 years, equating to a 6% annualized return supported by $21 billion in projected 2026 free cash flow and a pipeline of 28 platforms generating at least $1 billion in annual revenue.

Breaking Down the Case for Johnson & Johnson

Last week, a Philadelphia jury found Johnson & Johnson (JNJ) liable for the ovarian cancer death of Gayle Emerson, awarding $250,000 in damages, the second consecutive talc verdict against the company following a $40 million California jury decision in December 2025, with more than 67,000 active lawsuits remaining and federal MDL trials now unblocked after a January 2026 magistrate ruling permitted expert testimony linking talc to ovarian cancer.

Full year 2025 revenue of $94.2 billion grew 6% operationally, with gross profit of $64.1 billion at 68% margins and operating income of $26.3 billion at 28% margins, as the business grew double digits excluding the approximately 620 basis point STELARA biosimilar headwind that defined the year’s narrative.

SG&A of $23.1 billion and R&D of $14.7 billion consumed $37.8 billion in total operating expenses against $64.1 billion in gross profit, yet operating margins expanded to 28% from 25.4% the prior year as the Intra-Cellular acquisition contributed CAPLYTA’s $249 million Q4 quarter and TREMFYA crossed $5 billion in annual sales for the first time.

CEO Joaquin Duato stated on the January 21, 2026, earnings call that “we have line of sight to double-digit growth by the end of the decade, which is notable as Johnson & Johnson is the only health care company that will soon deliver more than $100 billion in annual revenue,” a claim grounded in 13 pharmaceutical brands growing double digits in 2025 and 28 platforms each exceeding $1 billion in annual revenue.

Free cash flow of $19.7 billion in 2025 is guided to rise to $21 billion in 2026, while the planned Orthopaedics separation targeting mid-2027 will push the high-growth asset share of the MedTech portfolio from approximately 50% today to over 70%, with $500 million in full-year MedTech tariff costs and hundreds of millions from the MFN government drug pricing agreement already absorbed into the $11.43 to $11.63 adjusted EPS guidance range.

The investment tension centers on whether Johnson & Johnson can sustain 6% revenue growth toward a $100 billion 2026 midpoint and expand operating margins to 34.5% by 2028, against a backdrop of $243 current stock price, 19x forward P/E, and a 6% annualized return through December 2028 that requires clean pipeline execution across ICOTYDE, milvexian, and OTTAVA without talc litigation reserves re-emerging to disrupt the $21 billion free cash flow trajectory.

What the Model Says for X Stock

Johnson & Johnson’s second consecutive talc verdict on February 13, 2026, adds to 67,000+ active lawsuits proceeding without bankruptcy protection, creating direct earnings reserve risk against the $21 billion free cash flow trajectory the model requires to sustain margin expansion.

The model’s assumption underwrites 6% revenue growth, 34% operating margins, and a 19x exit multiple, producing a $288 target price by December 2028, with the margin assumption requiring 650 basis points of expansion above fiscal 2025’s 28% operating margin.

The market assumption for the forward P/E as of February 17, 2026, stands at 21x, expanded from 14x at December 2024, and the model’s 19x exit multiple sits below that current market assumption, anchoring on multiple compression from today’s elevated level.

The Street mean target of $231 as of February 17, 2026, sits 5% below the current $243 price, with the target-to-price ratio falling to 95%, the lowest across six observed periods, as 10 of 24 analysts rate the stock Hold or worse.

The model delivers 18% total upside and a 6% annualized return from $243 to $288, sitting materially below the 10% equity hurdle rate, as $500 million in MedTech tariffs and MFN drug pricing impacts already absorbed into guidance limit earnings expansion.

The model signals a Sell, as a 6% annualized return sits well below the 10% equity hurdle, the stock already trades above the Street’s $231 mean target, and the $288 price by December 2028 requires margin expansion no analyst currently prices in.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Johnson & Johnson stock:

1. Revenue Growth: 6.1%

Johnson & Johnson stock delivered 6% revenue growth in fiscal 2025 to $94.2 billion, as DARZALEX crossed $14 billion and TREMFYA exceeded $5 billion annually, yet the STELARA biosimilar headwind of 620 basis points that suppressed prior years will not repeat as a mathematical tailwind.

The fiscal 2026 revenue estimate of $100.6 billion reflects 6.8% growth, slightly above the model’s assumption, as TREMFYA’s 65% Q4 growth, SPRAVATO’s 57% full-year expansion, and the 53rd calendar week contributing approximately 100 basis points support the trajectory.

The 6.1% model’s assumption through December 2028 rests on DARZALEX sustaining above $14 billion annually, ICOTYDE launching successfully in psoriasis and expanding into IBD, and the Orthopaedics separation completing by mid-2027 without disrupting MedTech commercial execution.

Any stalling in TREMFYA’s IBD penetration, combined with MFN drug pricing pressure on Innovative Medicine and $500 million in MedTech tariffs compressing the revenue-to-earnings conversion ratio, compounds operating income shortfalls faster than the 28-platform portfolio breadth can absorb across a $100 billion revenue base.

This sits in line with the 1-year revenue growth of 6%, as the model embeds forward momentum from oncology launches and immunology expansion while the 53rd week provides a structural 2026 tailwind, and sustaining 6.1% through 2028 requires pipeline execution across ICOTYDE, milvexian, and OTTAVA without talc litigation reserve rebuilds disrupting free cash flow.

2. Operating Margins: 34.5%

Johnson & Johnson stock reported 32.2% EBIT margins over the last twelve months on $30.4 billion in operating income, consistent with the 3-year and 5-year averages of 31.4%, as oncology mix shift and post-STELARA portfolio recovery drove margins above the 10-year average of 29.8%.

The 34.5% model’s assumption sits 230 basis points above the current 32.2% level, above the fiscal 2026 EBIT margin estimate of 33.3%, as Orthopaedics separation, MedTech manufacturing optimization, and continued oncology revenue concentration support incremental annual expansion toward the target.

Reaching 34.5% by December 2028 requires the Orthopaedics separation to complete by mid-2027 without stranded cost overruns, OTTAVA’s de novo approval to avoid launch delays sustaining elevated Surgery R&D spend, and talc litigation settlements to remain contained without reserve rebuilds above the $7 billion reversal recorded in Q1 2025.

The market assumption for the forward P/E as of February 17, 2026, stands at 21.1x, expanded from 14.4x at December 2024, as STELARA headwinds cleared and oncology momentum accelerated, yet the stock trades 5% above the Street’s mean target of $231, with 10 of 24 analysts at Hold or worse, creating a sentiment premium the 34.5% margin assumption must validate through execution.

Each 100 basis point EBIT margin shortfall on $100 billion of fiscal 2026 revenue represents $1 billion in missed operating income, meaning any talc reserve rebuild combined with Orthopaedics separation costs and $500 million in MedTech tariffs compresses margins back toward 32% faster than TREMFYA and DARZALEX growth can recover.

This sits above the 1-year EBIT margin of 32.2%, as the model embeds the full benefit of portfolio pruning, Orthopaedics separation, and oncology mix shift, and reaching 34.5% requires sustained margin expansion without a single material litigation charge or separation cost overrun disrupting the 230 basis point climb from today’s baseline.

3. Exit P/E Multiple: 19x

The 19x exit multiple capitalizes Johnson & Johnson stock’s normalized net income at December 2028 under conditions of 6.1% revenue growth and 34.5% operating margins, treating the multiple as a terminal earnings anchor for a diversified healthcare company with 28 platforms each exceeding $1 billion in annual revenue.

The model already embeds 34.5% operating margin expansion and 6.1% revenue growth through fiscal 2028, meaning the 19x exit multiple does not require additional credit for pipeline approvals or Orthopaedics separation value unlock, as both are absorbed in the earnings trajectory and a higher multiple would double-count growth already in the model.

The market assumption for the forward P/E as of February 17, 2026, stands at 21x, expanded from 14x at December 2024, and the model’s 19x exit multiple sits below the current market assumption, treating today’s elevated sentiment as temporary and anchoring the terminal value on multiple compression from the current 21x level.

If talc litigation reserves require rebuilding above the $7 billion Q1 2025 reversal, or if the Orthopaedics separation generates material stranded costs, earnings compression below the 34.5% margin assumption pushes the sustainable multiple toward the 16x to 17x range observed across the 5-year and 10-year historical periods rather than sustaining near 19x, and the $288 target collapses toward the Street’s mean target of $231.

This sits above the 1-year historical P/E of 16.5x, as the model embeds premium earnings quality from post-separation portfolio concentration in high-growth oncology, immunology, and cardiovascular assets, and sustaining 19x through December 2028 requires the 67,000+ talc lawsuits to remain contained without a systemic verdict pattern that forces reserve recognition and compresses the market’s willingness to pay above 17x.

What Happens If Things Go Better or Worse?

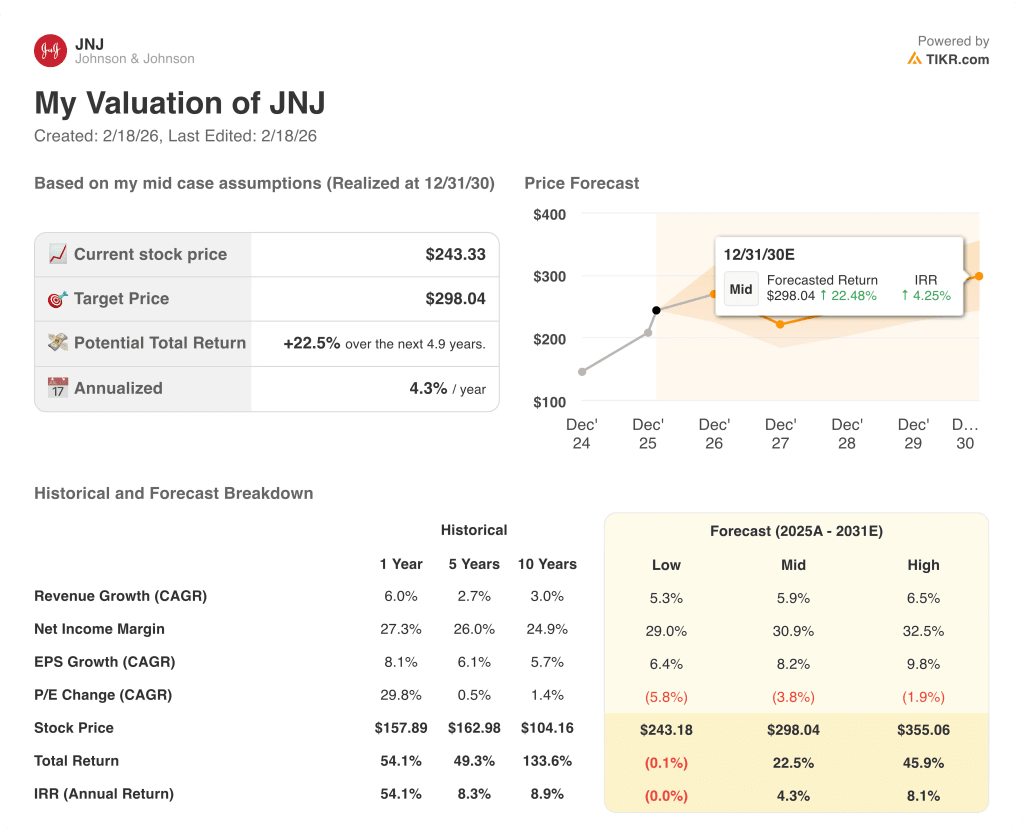

Johnson & Johnson stock outcomes through December 2030 rest on pipeline execution across oncology and immunology, talc litigation containment, and whether the Orthopaedics separation delivers the margin structure management has committed to.

- Low Case: If talc litigation accelerates reserve rebuilds and ICOTYDE or OTTAVA face regulatory delays, revenue grows around 5.3% and net income margins stay near 29% → 0% annualized return.

- Mid Case: With TREMFYA, DARZALEX, and SPRAVATO sustaining double-digit growth and the Orthopaedics separation completing on schedule, revenue growth near 5.9% and margins improving toward 31% → 4.3% annualized return.

- High Case: If ICOTYDE captures meaningful psoriasis and IBD share, milvexian delivers a positive readout, and talc exposure stays contained, revenue reaches about 6.5% and margins approach 33% → 8.1% annualized return.

How Much Upside Does Johnson & Johnson Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!