Key Takeaways:

- Capital Program Scale: Public Service Enterprise Group filed last January for $4.58 billion in Secured Medium-Term Notes, Series R, supporting its $22.5 billion to $26 billion 5-year capital investment plan funded without new equity issuance or asset sales.

- Data Center Load Pipeline: Public Service Enterprise Group stock carries 11.5 gigawatts of large load inquiries converting at 20% to new business, with PSE&G’s Q3 2025 non-GAAP operating earnings of $1.13 per share up 26% year-over-year as new distribution rates from the October 2024 rate case contributed $0.30 per share of margin improvement.

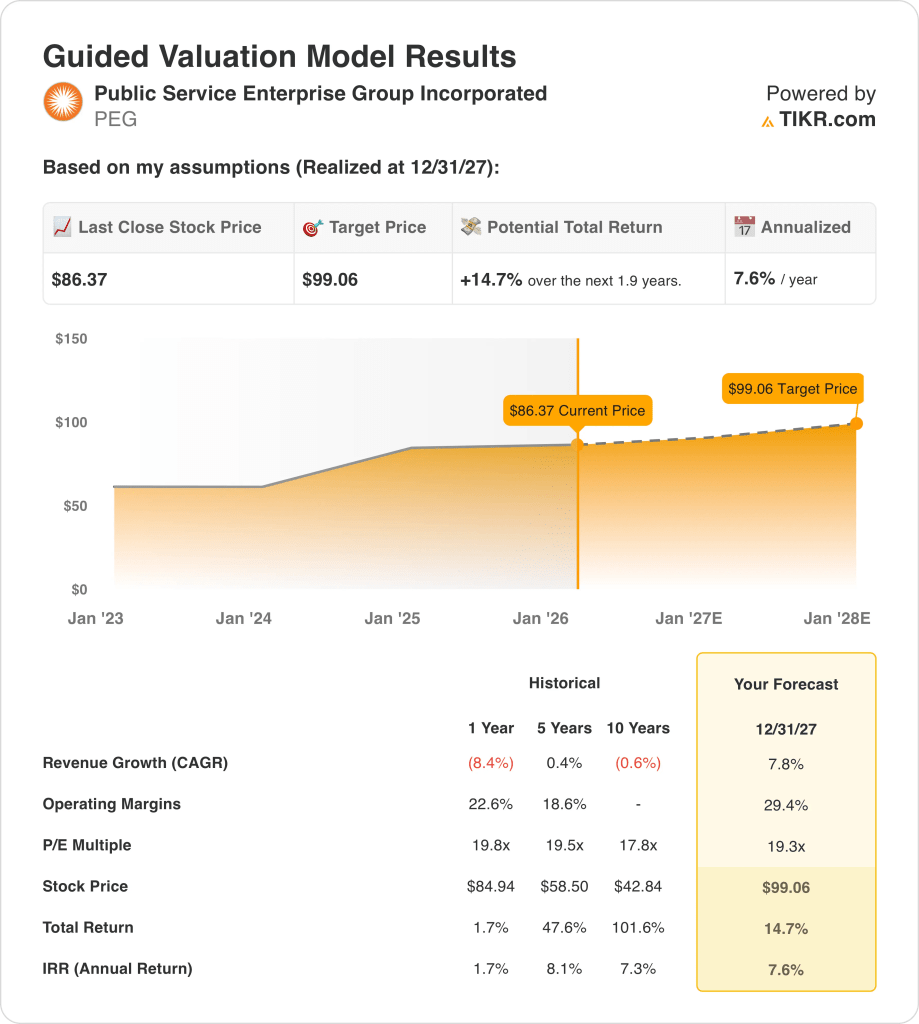

- Price Target: Based on 8% revenue growth, 29% operating margins, and a 19x exit multiple, Public Service Enterprise Group stock could reach $99 by December 2027 from $86 today.

- Return Profile: Public Service Enterprise Group implies 15% total upside from $86 to $99 over 2 years, equating to an 8% annualized return supported by a reaffirmed 5% to 7% EPS CAGR through 2029 and a $0.63 quarterly dividend yielding 3%.

Breaking Down the Case for Public Service Enterprise Group

Public Service Enterprise Group Incorporated (PEG) filed last January for $4.58 billion in Secured Medium-Term Notes, Series R, reinforcing its capacity to execute a $22.5 billion to $26 billion 5-year regulated capital plan without issuing new equity as fiscal 2025 revenue grew 16% to $12 billion and EBITDA margins expanded to 39%.

PSE&G’s Q3 2025 non-GAAP operating earnings of $1.13 per share reflected 26% growth over Q3 2024 as new distribution rates from the October 2024 rate case contributed $0.30 per share and $2.7 billion in 9-month regulated capital investment drove operating margins to 26% on a trailing 12-month basis.

CEO Ralph LaRossa stated on the November 3, 2025, earnings call that “our balance sheet continues to enable us to fund PSEG’s 5-year capital investment program of $22.5 billion to $26 billion without the need to issue new equity or sell assets and provides the opportunity for consistent and sustainable dividend growth,” framing capital allocation discipline as the foundation for shareholder value through 2029.

Also last January, Geisha J. Williams was elected to the PSEG Board of Directors as the company’s energy efficiency programs reported $900 million in annual customer savings and 480,000 program participants since October 2020, while Hope Creek’s fuel cycle extension from 18 to 24 months and Salem’s 200-megawatt up-rate targeting 2027 to 2029 support nuclear output growth.

The investment tension centers on whether PSE&G’s 11.5-gigawatt data center load pipeline converts beyond the current 20% rate, Argus’s January 2026 Strong-Buy upgrade contrasts with JPMorgan’s (JPM) January 2026 Neutral rating and $85 target, and a 7.6% annualized return through December 2027 sits below a 10% equity hurdle rate against a consensus average price target of $91.

What the Model Says for PEG Stock

Public Service Enterprise Group stock delivered 16% revenue growth in fiscal 2025 and Q3 non-GAAP EPS up 26%, yet the $4.58 billion debt filing last January and 11.5 gigawatt data center pipeline signal elevated capital intensity through 2027 as the P/E compressed from 21.2x in December 2024 to 20.5x by February 2026.

The model’s assumption underwrites 7.8% revenue growth, 29.4% operating margins, and a 19.3x exit multiple, producing a $99 target price by December 2027, with revenue growth above fiscal 2024’s negative 8.4% decline but margins sitting above the trailing 12-month level of 25.5%.

The model delivers 14.7% total upside and a 7.6% annualized return from $86.37, falling meaningfully below the standard 10% equity hurdle rate even as the $0.63 quarterly dividend adds 3% yield and the 5-year capital plan of $22.5 billion to $26 billion runs without equity dilution.

The model signals a Hold, as a 7.6% annualized return against a 10% equity hurdle rate does not compensate investors sufficiently for the capital intensity risk of a $26 billion 5-year program and regulatory dependency on New Jersey supply policy for data center load conversion above the current 20% rate.

With a 7.6% annualized return falling short of the 10% equity hurdle, the model supports capital preservation over appreciation, as the $99 target by December 2027 reflects earnings growth without multiple expansion, justified strictly by regulated utility math and dividend yield.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Public Service Enterprise Group stock:

1. Revenue Growth: 7.8%

Public Service Enterprise Group stock’s revenue history shows fiscal 2024 revenue declined 8.4% to $10.3 billion as fuel and purchased power costs reached $3.4 billion, yet LTM revenue recovered to $11.7 billion as new October 2024 distribution rates took full effect.

The 7.8% growth assumption draws support from fiscal 2025 estimated revenue of $12 billion up 16%, as PSE&G’s $3.8 billion full year regulated capital spending and the October 2024 rate case settlement contributed $0.30 per share of distribution margin improvement through Q3 alone.

Forward growth requires PSE&G’s 11.5 gigawatt data center load pipeline to convert above the current 20% rate, the $4.58 billion Medium-Term Notes filing from last January to fund infrastructure expansion without crowding capital allocation, and New Jersey supply policy to support regulated generation investments.

Any shortfall in data center load conversion below 20% or delay in the $22.5 billion to $26 billion 5-year capital plan approval compresses revenue growth faster than the model assumes, as PSE&G’s customer base grew only 1% annually and fuel and purchased power costs of $3.9 billion in the LTM period limit margin leverage from volume alone.

This sits above the 1-year revenue growth of negative 8.4%, as the October 2024 rate case settlement and PSE&G’s $2.7 billion 9-month capital investment restored revenue momentum, and sustaining 7.8% requires both regulatory continuity and data center load conversion that fiscal 2024’s revenue base did not reflect.

2. Operating Margins: 29.4%

Public Service Enterprise Group stock reported 23.6% operating margins in fiscal 2024 on $2.4 billion in operating income as operations and maintenance expenses reached $3.3 billion and depreciation and amortization rose to $1.2 billion, with LTM margins recovering to 25.5% after the rate case settlement began flowing through.

The 29.4% margin assumption sits materially above fiscal 2024’s 23.6% level, as fiscal 2025 EBIT margins are estimated at 26.9% and EBITDA margins at 38.9% from the full year benefit of new distribution rates and Hope Creek’s fuel cycle extension from 18 to 24 months reducing scheduled refueling O&M costs.

Margin expansion toward 29.4% depends on O&M remaining controlled as PSE&G’s 5-year energy efficiency program deploys up to $2.9 billion and nuclear generation sustains above 90% capacity factors, as the Q3 2025 nuclear fleet ran at 92.4% with 7.9 terawatt hours against $3.6 billion cleared at $329 per megawatt day in PJM’s July 2025 auction.

The forward P/E market assumption of 20.5x as of February 2026, down from 21.2x in December 2024, reflects investor skepticism about margin durability as capital intensity rises and New Jersey affordability pressures limit rate case aggressiveness, creating a ceiling on margin expansion even as PTC thresholds support nuclear earnings floors.

Any deviation in nuclear capacity factors below 90%, O&M cost acceleration from Salem’s 200-megawatt uprate between 2027 and 2029, or fuel cost volatility above $3.9 billion LTM levels compresses margins below 29.4% faster than earnings growth can recover, as three consecutive years of O&M around $3.1 billion to $3.3 billion demonstrate how cost discipline historically constrained margin expansion even in higher-revenue years.

This sits above the 1-year operating margin of 23.6%, as the October 2024 rate case settlement and nuclear PTC support restored earnings momentum through 2025, and reaching 29.4% requires capital investment productivity and data center load conversion to jointly materialize without regulatory pushback on New Jersey rate affordability.

3. Exit P/E Multiple: 19.3x

Public Service Enterprise Group stock’s valuation history centers on regulated utility earnings stability, with the forward P/E at 20.5x as of February 2026, down from 21.2x in December 2024, as capital intensity from the $22.5 billion to $26 billion 5-year plan and New Jersey supply policy uncertainty compressed investor sentiment.

The 19.3x exit multiple capitalizes normalized earnings at December 2027 under the assumption that 7.8% revenue growth and 29.4% operating margins materialize as PSE&G’s rate base earns a return on $21 billion to $24 billion of regulated capital, Hope Creek and Salem nuclear units sustain above 90% capacity factors, and data center load converts above 20% without regulatory affordability intervention.

This multiple assumes the market values PEG slightly below the current forward P/E market assumption of 20.5x, as the model does not embed multiple expansion and instead assumes that elevated capital intensity from the $4.58 billion Medium-Term Notes filing from last January and New Jersey’s 40% import dependency maintain investor caution about earnings durability beyond 2027.

The exit multiple sits below the 1-year historical P/E of 19.8x, as the model assumes slight compression from higher capital intensity through the 5-year $26 billion plan while regulated utility earnings grow at a pace constrained by New Jersey affordability policy, and any failure in data center load conversion or nuclear capacity factor decline would compress the multiple toward the 17.8x 10-year historical level rather than sustaining near 20x.

What Happens If Things Go Better or Worse?

Public Service Enterprise Group stock results are shaped by New Jersey regulatory policy, data center load conversion above the current 20% rate, and nuclear fleet capacity factors through December 2029.

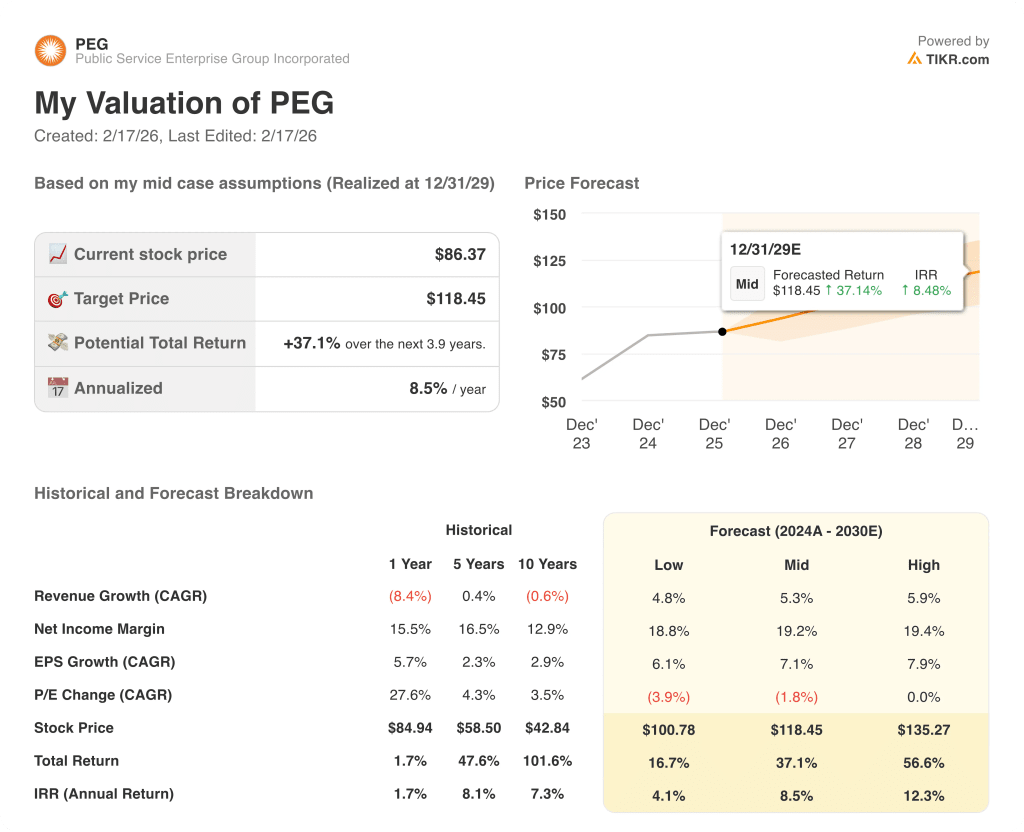

- Low Case: If data center load conversion stalls and regulated capital returns disappoint, revenue grows 5% and net margins hold near 19% → 4% annualized return.

- Mid Case: With the $22.5 billion to $26 billion capital plan executing and nuclear PTC floors holding, revenue grows 5% and net margins reach 19% → 9% annualized return.

- High Case: If New Jersey supply policy expands regulated generation opportunities and data center load converts above 20%, revenue grows 6% and net margins approach 19% → 12% annualized return.

How Much Upside Does Public Enterprise Service Group Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!