Key Stats for AMD Stock

- Past week’s performance: Fell about 17% after the company’s latest earnings report, giving back a portion of its recent AI‑driven gains.

- 52-week range:$76 to $267

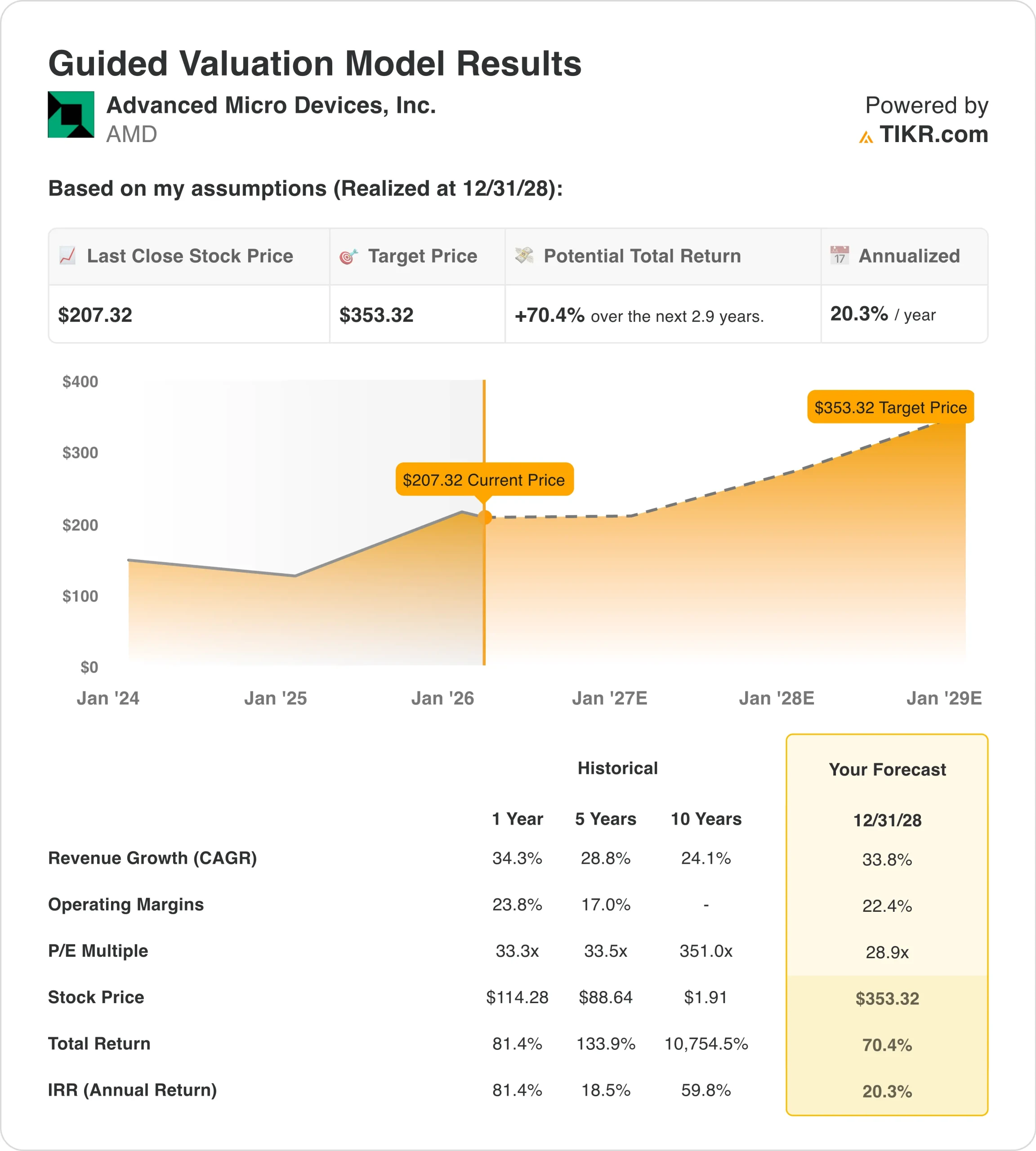

- Valuation model target price: $353

- Implied upside: 70.4% over 2.9 years

Value your favorite stocks like AMD with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Advanced Micro Devices (AMD) reported fourth‑quarter 2025 revenue of $10,270 million, which beat Street estimates of $9,670 million by 6.2% and grew 34.1% year over year.

Net income rose to $2,519 million, and adjusted EPS was $1.53, topping the $1.32 consensus estimate by about 16.0%. Free cash flow for the quarter was $2,082 million, up 90.8% year over year, as the operating cash flow of $2,304 million comfortably covered $222 million of capex.

Cash flow from operations over the last twelve months totaled $7,709 million, while cash from investing was a net outflow of $5,533 million because of acquisitions and capital spending tied to growth initiatives.

These metrics show that, despite the share‑price pullback, AMD’s financial position remains strong and supports continued AI and data‑center expansion.

Recent headlines include AMD’s strategy to lead the $1 trillion compute market, new AI collaborations with HPE and TCS, and contract wins for a new European supercomputer, all of which reinforce long‑term demand for EPYC CPUs, Instinct accelerators, and adaptive SoCs.

At the same time, February filings from the same feed show insider share sales by CEO Lisa Su and other executives, which added to investor caution after a big run‑up into earnings.

Together, these datapoints suggest the recent move reflects an expectations reset around timing and magnitude of AI growth rather than a deterioration in AMD’s underlying business.

See analysts’ growth forecasts and price targets for AMD (It’s free) >>>

Is AMD Stock Undervalued?

Under the valuation model assumptions realized through 2028, the stock is modeled using:

- Revenue growth (CAGR): 33.8%

- Operating margins: 22.4%

- Exit P/E multiple: 28.9x

Based on these inputs, the model estimates a target price of $353.32, implying 70.4% total upside from the current share price of $207.32 and an 20.3% annualized return over the next 2.9 years.

Those modeled returns are well above the 10% annual threshold that typically signals an attractive setup, and they assume AMD can sustain roughly mid‑30s revenue growth while lifting operating margins into the low‑20s as higher‑margin data‑center and AI products take a larger share of the mix.

However, the model’s outcome depends on AMD continuing to win share with EPYC and Instinct, executing its Helios and other AI platforms, and maintaining strong relationships with cloud and enterprise customers in a competitive market.

If those operational drivers hold, the current valuation looks more like an expression of execution risk and sector volatility than a sign the long‑term thesis has broken.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>