Reported earnings rarely reflect true ongoing profitability. Every income statement contains items that will not repeat: restructuring charges, asset write-downs, litigation settlements, gains from asset sales, and dozens of other entries that distort the picture of sustainable earnings. Investors who take reported figures at face value misjudge what the business actually earns in a normal year.

Adjusting for one-time items reveals the underlying economics that reported numbers obscure. A company showing $3 per share in GAAP earnings might have $4 in normalized earnings after removing a restructuring charge. Another showing $5 per share might have only $3.50 after backing out a one-time gain. These adjustments change valuation conclusions dramatically. A stock looking expensive on reported earnings might be cheap on normalized earnings, and vice versa.

The challenge is determining which items truly are non-recurring and which represent ongoing costs that management prefers to label as one-time. Companies have incentives to classify unfavorable items as non-recurring while treating favorable items as core results. Adjusting properly requires judgment about what belongs in normalized earnings and skepticism about management’s preferred presentation.

Identify Common One-Time Items

One-time items fall into several recurring categories. Learning to spot them quickly helps you focus on the adjustments that matter most.

Restructuring charges appear when companies reorganize operations, close facilities, or reduce headcount. These charges include severance payments, lease termination costs, and asset write-downs associated with the restructuring. They hit the income statement as operating expenses and can significantly depress reported earnings in the periods they occur.

Asset impairments and write-downs reduce the carrying amount of goodwill, intangible assets, or long-lived assets when their fair value is below their carrying amount. These non-cash charges flow through the income statement but do not affect the company’s cash position or ongoing operations. A large goodwill impairment could halve reported earnings without changing the business.

Gains and losses on asset sales distort earnings in the opposite direction. A company selling a division, real estate, or investment portfolio records the difference between sale proceeds and book value as a gain or loss. These transactions reflect balance sheet cleanup rather than operating performance.

Litigation settlements, insurance recoveries, and tax adjustments create earnings volatility unrelated to business operations. A company paying a large legal settlement or receiving a one-time tax benefit shows distorted earnings that will not repeat.

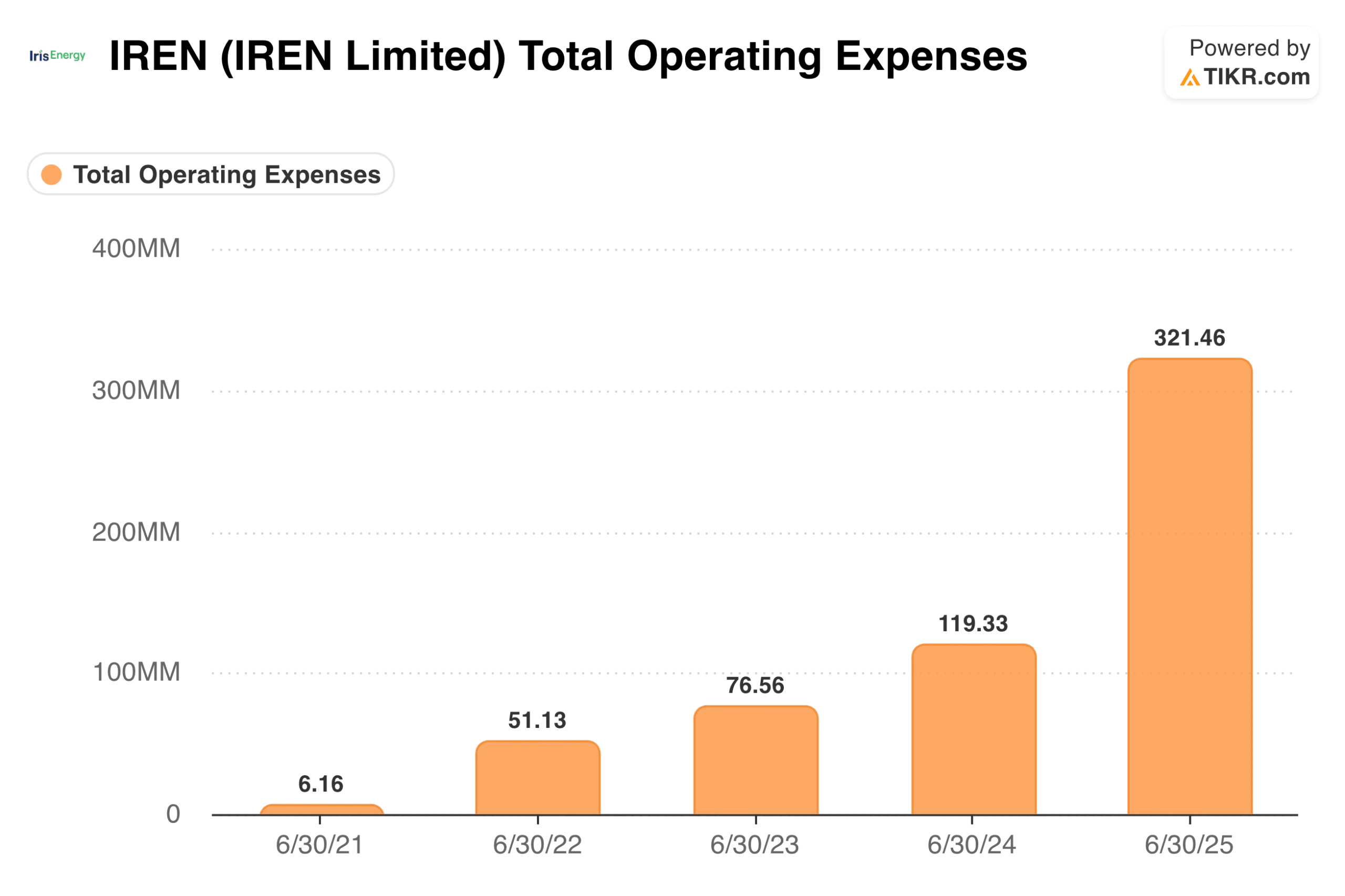

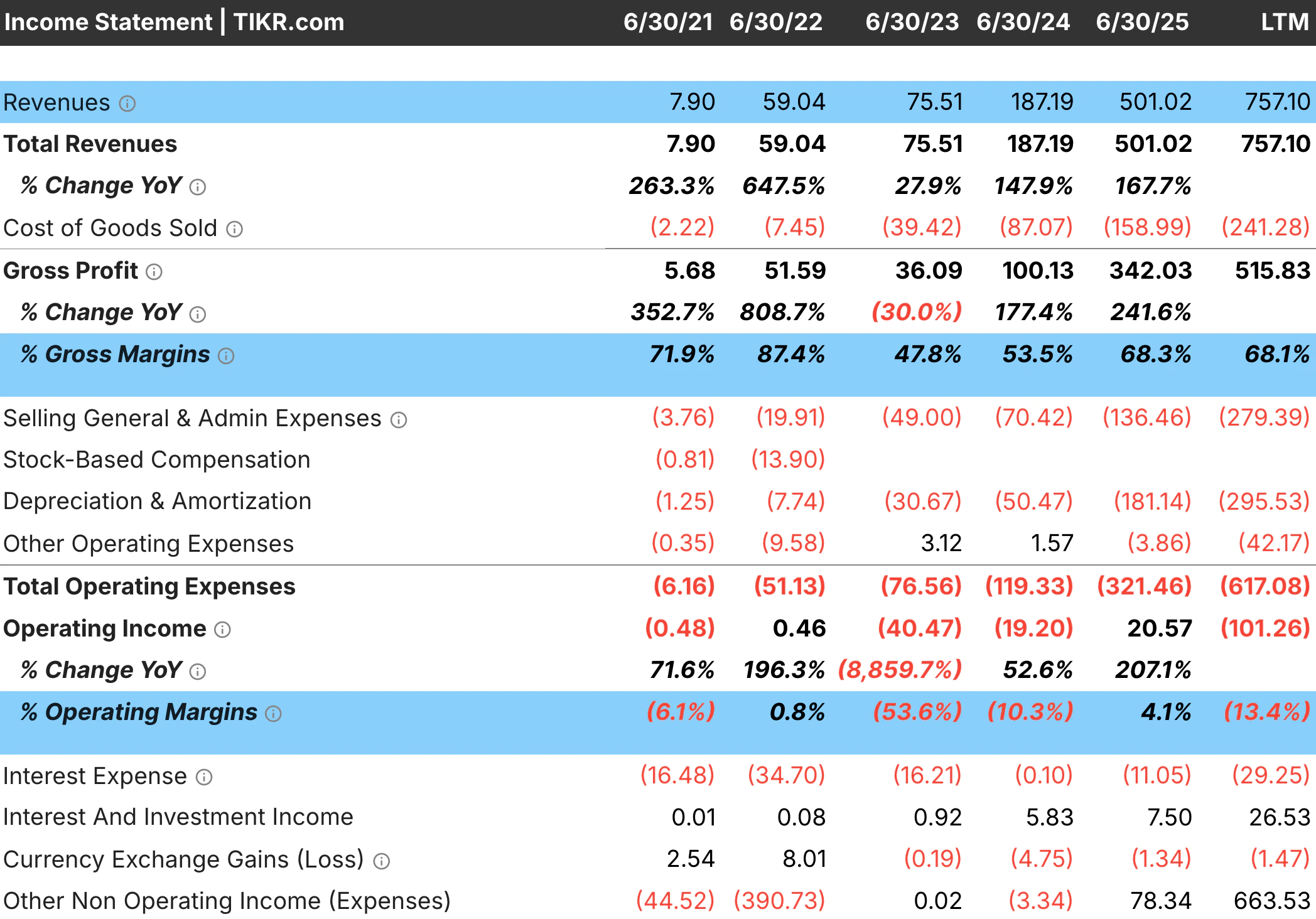

TIKR tip: Review the Income Statement for companies like IREN (IREN) that have seen significant increases in spending in TIKR’s Detailed Financials, particularly for unusual line items or significant year-over-year swings in operating expenses. Large changes often signal one-time items that warrant investigation.

Look for unusual line items for thousands of stocks in under 60 seconds (Free with TIKR) >>>

Determine What Truly Is Non-Recurring

Not every item labeled one-time actually is. Some companies report restructuring charges year after year, making them a recurring cost of doing business rather than a genuine anomaly. Distinguishing truly non-recurring items from chronic expenses disguised as one-time requires examining patterns over time.

Review five years of financial history for repeat appearances. A company that has taken restructuring charges in four of the past five years has restructuring as a normal operating cost. Excluding these charges overstates normalized earnings. A company with one restructuring charge following a major acquisition or strategic shift has a genuinely non-recurring item that should be adjusted for.

Examine management’s adjusted earnings presentation with skepticism. Companies highlight metrics that make results look better. They exclude unfavorable items as non-recurring while including favorable items in adjusted figures. Compare the items management excludes with your own assessment of what will not recur. Add back the excluded items in the items management that you believe are recurring. Remove items that they include that you believe are one-time.

Consider whether the item relates to ongoing operations or a discrete event. Charges associated with a specific acquisition, facility closure, or legal case are more likely to be genuinely non-recurring. Charges that reflect ongoing business challenges, such as inventory obsolescence or customer bankruptcies, are more likely to recur, even if management presents them as one-time.

TIKR tip: Look at multiple years of Income Statement data in TIKR’s Detailed Financials. Items that appear repeatedly are not truly one-time, regardless of how management labels them.

Evaluate any stock in less than 60 seconds with TIKR’s Income Statement dashboard (It’s free) >>>

Connecting Market Share to Financial Performance

Share gains typically precede margin expansion because scale improves cost position. A company gaining share spreads fixed costs over more units, gains bargaining power with suppliers, and can invest more than smaller competitors. These advantages accumulate gradually, so margin expansion may lag share gains by several years.

Share losses work in reverse, often with a delay before margins compress. A company can maintain margins for a while by cutting costs or reducing investment. Eventually, these approaches exhaust themselves, and the margin collapse that follows is often steeper than the gradual share erosion that preceded it.

Returns on capital often track market position over time. Industry leaders with dominant share typically earn higher returns than marginal players because their scale advantages translate to better economics.

TIKR tip: Use TIKR’s Detailed Financials to track revenue growth, margins, and ROC alongside your market share analysis. Connecting share trends to financial trends reveals whether competitive dynamics are improving or deteriorating.

Review revenues and margins to find stocks with solid revenue and profitability (Free with TIKR) >>>

Calculate Normalized Earnings

Once you identify genuine one-time items, adjust earnings to reflect ongoing profitability. The mechanics are straightforward but require attention to tax effects and consistency.

Add back one-time charges and subtract one-time gains on an after-tax basis. A $100 million restructuring charge does not reduce normalized earnings by $100 million because the charge is tax-deductible. At a 25% tax rate, the after-tax impact is $75 million. Use the company’s effective tax rate to calculate the true earnings impact of each adjustment.

Apply adjustments consistently across multiple years when making comparisons. If you exclude restructuring charges from the current year, exclude them from prior years as well. Mixing adjusted and unadjusted figures produces meaningless comparisons. Normalized year-over-year growth requires normalized figures in both periods.

Reconcile your adjusted earnings to cash flow as a sanity check. Operating cash flow should roughly align with your normalized earnings over time because cash flow already excludes many non-cash one-time items. Large persistent gaps between your adjusted earnings and cash flow suggest either additional adjustments needed or that some items you treated as one-time actually affect cash economics.

Document your adjustments explicitly. Write down what you added back or removed, the amounts, and your reasoning. This record helps you stay consistent when updating the analysis and reveals your assumptions clearly if results differ from expectations.

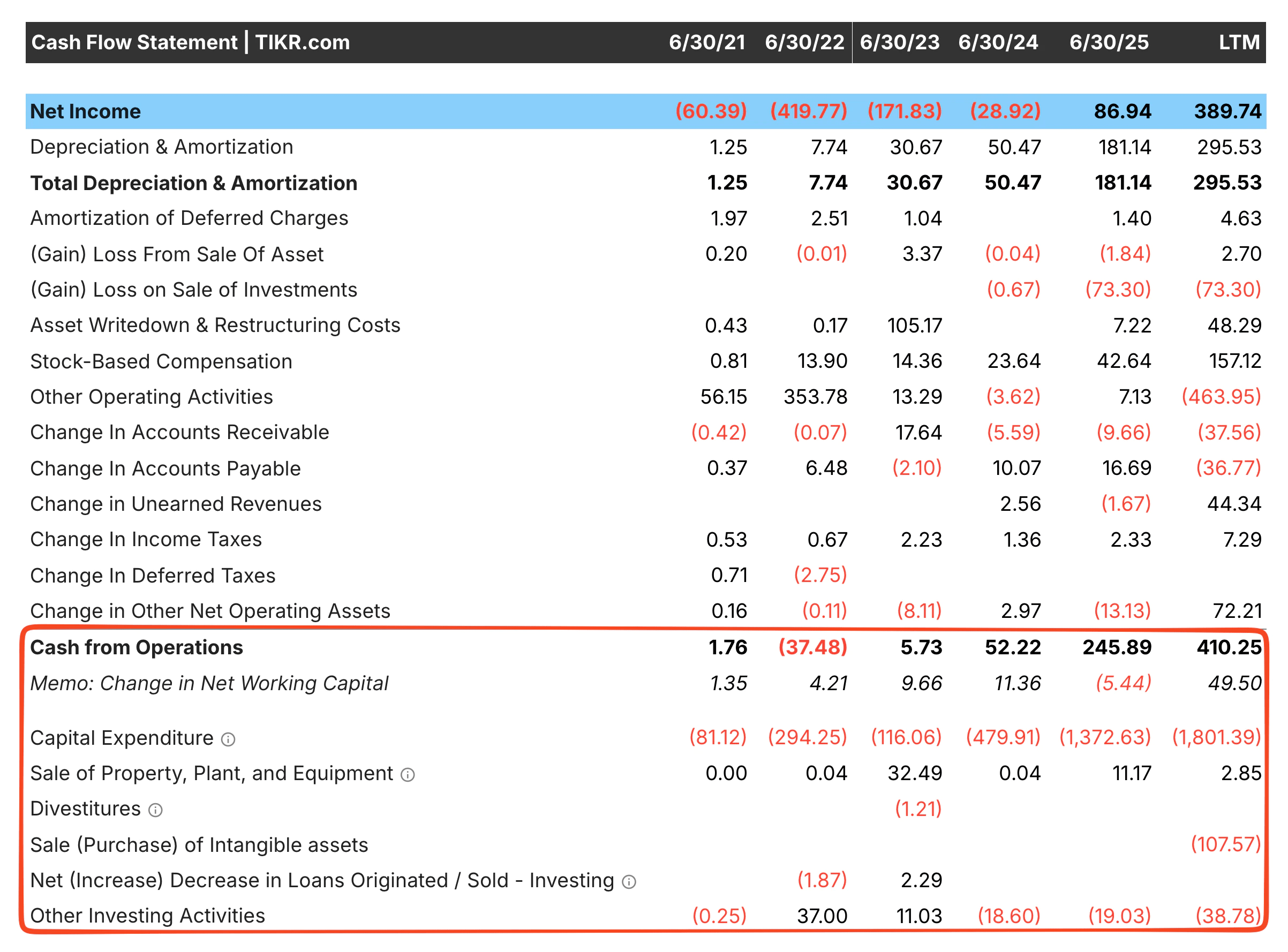

TIKR tip: Use the Cash Flow Statement in TIKR’s Detailed Financials to check your adjusted earnings against cash from operations. Non-cash charges, such as impairments, should already be added back to cash flow to help verify your adjustments.

Look at the cash flow statement for the top stocks in your portfolio (It’s free) >>>

Avoid Over-Adjusting

The temptation when adjusting is to remove every charge that depresses earnings. This approach produces unrealistically high normalized figures that overstate true profitability. Disciplined adjustment requires knowing when to stop.

Accept that some costs are real even if they are lumpy. A company that makes regular acquisitions will incur integration costs. A retailer refreshing store formats will take periodic charges. These costs may not appear smoothly each year, but they represent genuine expenses of running the business. Excluding them entirely overstates sustainable earnings.

Compare your adjusted margins to industry norms as a reality check. If your adjustments produce operating margins five points above any competitor, you have probably adjusted too aggressively. Genuine normalized margins should fall within reasonable range of peer companies with similar business models.

Be especially skeptical when management’s adjusted figures diverge dramatically from GAAP. A company where adjusted earnings exceed GAAP earnings by 50% or more every year is either in perpetual crisis or using adjustments to manufacture profitability that does not exist. The wider the gap, the more scrutiny your own adjustments deserve.

Consider that some one-time items reflect real economic events. A goodwill impairment may not repeat, but it signals that an acquisition destroyed value. A restructuring charge may be non-cash, but it reflects strategic mistakes that consumed resources. Adjusting away every consequence of poor decisions produces a sanitized picture that ignores how the company actually performed.

TIKR tip: Compare your normalized margin calculations to competitors using TIKR’s Detailed Financials for each peer company. Adjusted margins dramatically above the peer range suggest over-adjustment rather than superior economics.

The TIKR Takeaway

Adjusting for one-time items reveals the sustainable earnings that reported figures obscure. Restructuring charges, asset impairments, and litigation costs depress reported results temporarily. Asset sale gains and tax benefits inflate them. Removing these items produces normalized earnings that better reflect ongoing profitability.

The adjustment process requires identifying genuinely non-recurring items, distinguishing them from chronic costs labeled as one-time, calculating after-tax impacts, and applying changes consistently across periods. Cash flow provides a useful check on adjusted figures. Peer comparisons prevent over-adjustment that produces unrealistic margins.

TIKR provides the historical financial data to identify one-time items and verify adjustments. Multi-year Income Statements reveal patterns that separate true anomalies from recurring charges. Cash Flow Statements confirm that adjustments align with actual cash flow. The platform supplies the raw material for analysis, while your judgment determines which adjustments produce the most accurate picture of underlying earnings.

Find undervalued stocks in less than 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Value Any Stock in Under 60 Seconds with TIKR

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- Discover which stocks billionaire investors are purchasing, so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!