Key Takeaways:

- Rotisserie Chicken Lawsuits: Costco faces 2 proposed class action lawsuits filed last January and last February, one alleging salmonella contamination at the Lincoln Premium Poultry plant in Nebraska testing 15% of chicken parts positive, and a second alleging false preservative-free advertising on 157 million rotisserie chickens sold in fiscal 2025.

- January Sales Momentum: Costco reported $21.33 billion in January net sales up 9.3% year-over-year, with digitally-enabled sales surging 34% and Canada comparable sales up 11%, while tariff lawsuits filed alongside hundreds of companies challenge Trump’s sweeping trade duties before the U.S. Court of International Trade.

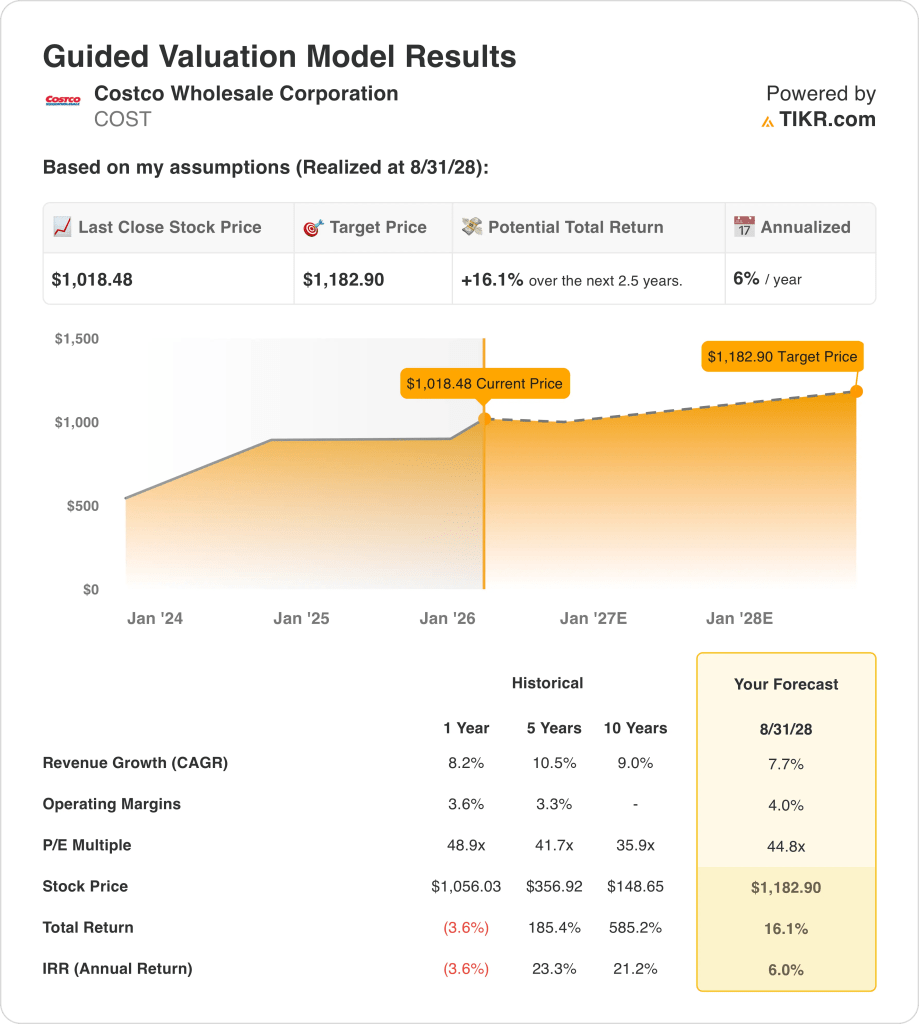

- Price Target: Based on 8% revenue growth, 4% operating margins, and a 45x exit multiple, Costco Wholesale Corporation stock could reach $1,183 by August 2028 from $1,018 today.

- Return Profile: Costco Wholesale Corporation implies 16% total upside from $1,018 to $1,183 over 3 years, equating to a 6% annualized return as fiscal 2025 revenue of $275 billion and EPS of $18 support the earnings trajectory toward the $1,183 target.

Breaking Down the Case for Costco Wholesale Corp.

Costco Wholesale Corporation (COST) faces 2 proposed class action lawsuits filed last January and last February, the first alleging false preservative-free advertising on rotisserie chicken and the second alleging salmonella contamination at the Lincoln Premium Poultry plant in Fremont, Nebraska, with 15% of chicken parts testing positive and 157 million units sold in fiscal 2025 at $4.99 each.

January net sales reached $21.33 billion up 9.3% from $19.51 billion in the prior year period, as digitally-enabled sales surged 34% and Canada comparable sales grew 11%, with the first 22 weeks of fiscal 2026 totaling $123 billion up 9% as Midwest, Southeast, and Texas led U.S. regional performance.

Fiscal 2025 revenue of $275 billion grew 8% on gross profit of $35 billion at 13% margins, yet operating income of $10 billion held at 4% operating margins as $25 billion in SG&A expenses consumed the majority of gross profit generated across 924 warehouses worldwide.

IR Director Andrew Yoon noted on the February 4, 2026 sales call that comparable traffic frequency rose 2.4% worldwide and the average transaction grew 4.6%, demonstrating membership renewal strength even as gas price deflation created a 100 basis point headwind to reported comparable sales.

Costco also filed tariff lawsuits alongside hundreds of companies before the U.S. Court of International Trade challenging Trump’s sweeping trade duties, with the case now pending U.S. Supreme Court review after a three-judge panel blocked most tariffs in May and the Federal Circuit upheld that decision in August.

The investment tension centers on whether Costco stock at $1,018 and a 45x exit multiple through August 2028 delivers only 6% annualized returns against a 10% equity hurdle rate, even as the rotisserie chicken lawsuits, tariff uncertainty, and Walmart’s $1 trillion market cap competitive pressure converge on fiscal 2026 earnings.

What the Model Says for COST Stock

Costco Wholesale Corporation delivered $21.33 billion in January net sales up 9.3%, yet 2 active class action lawsuits over rotisserie chicken contamination and tariff litigation before the U.S. Supreme Court introduce legal cost risk that constrains the earnings growth trajectory through fiscal 2028.

The model’s assumption confirms 7.7% revenue growth, 4.0% operating margins, and a 44.8x exit multiple, producing a $1,183 target price by August 2028, with margins slightly above fiscal 2025’s 3.8% level and revenue growth modestly below last year’s 8.2%.

The market assumption for the forward P/E as of February 2026 stands at 49.4x, down from 53.9x in November 2024, as investor sentiment compressed despite 34% digitally-enabled sales growth and 9.3% January net sales growth, and the model’s 44.8x exit multiple sits below the current 49.4x market assumption.

The model delivers 16.1% total upside and a 6.0% annualized return from $1,018.48, falling meaningfully below the standard 10% equity hurdle rate, as the rotisserie chicken lawsuits, tariff uncertainty, and Walmart’s $1 trillion competitive threat limit the earnings expansion needed to close that gap.

The model signals a Sell, as a 6.0% annualized return sits well below the 10% equity hurdle rate and the $1,183 target by August 2028 does not compensate investors for the legal, regulatory, and competitive risks present at the current $1,018 share price.

With a 6.0% annualized return falling well short of the 10% equity hurdle, the model signals capital preservation rather than appreciation, as the $1,183 target by August 2028 does not reward investors for Costco stock’s legal exposure and competitive pressure at the current valuation.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Costco stock:

1. Revenue Growth: 7.7%

Costco stock delivered 8.2% revenue growth in fiscal 2025 to $275 billion as January net sales of $21.33 billion grew 9.3% year-over-year, yet digitally-enabled sales surging 34% and Canada comparables up 11% introduced faster-growing but lower-margin revenue channels that limit earnings conversion.

The 7.7% model’s assumption through fiscal 2028 rests on the 924-warehouse global network sustaining comparable traffic growth above 2%, nofoods comparable sales continuing at low double digits, and fresh foods and food court growth offsetting gas price deflation that already reduced total reported comp sales by 100 basis points in January.

Two active class action lawsuits over rotisserie chicken, one alleging salmonella contamination at the Lincoln Premium Poultry plant testing 15% of chicken parts positive and one alleging false preservative-free advertising, introduce legal cost and reputational risk that the model’s 7.7% growth assumption does not explicitly account for across fiscal 2026 to 2028.

The fiscal 2026 revenue estimate of $297 billion reflects 8.1% growth, in line with the model’s assumption, as SG&A expenses of $24.97 billion in fiscal 2025 represented 9.1% of revenue and any litigation settlement or warehouse remediation cost at the Nebraska plant pressures the efficiency ratio faster than membership fee growth can absorb.

This sits below the 1-year revenue growth of 8.2%, as the model anticipates modest deceleration from the fiscal 2025 pace, and the tariff lawsuit pending before the U.S. Supreme Court and rotisserie chicken litigation create legal expense headwinds that compound against the already thin gross margin structure of 13%.

2. Operating Margins: 4%

Costco stock reported 3.8% operating margins in fiscal 2025 on $10.38 billion in operating income, as gross profit of $35 billion at 13% margins funded $24.97 billion in SG&A expenses, leaving less than 4 cents of every revenue dollar as operating income across a $275 billion revenue base.

The 4.0% model’s assumption represents modest expansion above fiscal 2025’s 3.8% level, consistent with the fiscal 2026 EBIT margin estimate of 3.9% and EBITDA margin of 4.8%, as warehouse productivity gains from 34% digitally-enabled sales growth and nofoods comparable sales outperformance in jewelry, tires, and majors support incremental margin improvement.

Reaching 4.0% by fiscal 2028 requires SG&A expenses to grow slower than the 8.2% revenue pace of fiscal 2025, the Lincoln Premium Poultry plant salmonella lawsuit to resolve without material remediation costs, and the tariff challenges before the U.S. Supreme Court to avoid import cost increases that flow directly into cost of goods sold at 87% of revenue.

The market assumption for the forward P/E as of February 2026 stands at 49.4x, up from 44.8x at August 2025, as investors priced in 34% digitally-enabled sales acceleration and 9.3% January net sales growth despite the active litigation risk, creating a sentiment premium that the model’s conservative 4.0% margin assumption does not fully support at current stock prices.

Any failure in SG&A cost discipline, combined with litigation settlements across 2 class action lawsuits and potential tariff duty payments, collapses operating margins back toward 3.6% from fiscal 2024 faster than the 924-warehouse membership model can recover, as each 10 basis point margin shortfall on $275 billion of revenue represents $275 million in missed operating income.

This sits above the 1-year operating margin of 3.8% from fiscal 2025, as the model embeds warehouse productivity gains from digital sales acceleration and nofoods category outperformance, and reaching 4.0% requires SG&A discipline to hold while 2 active lawsuits add legal costs not yet visible in the fiscal 2025 income statement.

3. Exit P/E Multiple: 44.8x

The 44.8x exit multiple capitalizes Costco stock’s normalized net income at August 2028 under conditions of 7.7% revenue growth and 4.0% operating margins, treating the multiple as a terminal earnings anchor for a membership-based warehouse retailer with structural earnings durability and limited competitive substitution risk.

The model already embeds 4.0% operating margin expansion and 7.7% revenue growth through fiscal 2028, meaning the 44.8x exit multiple does not require additional credit for digital sales acceleration or new warehouse openings, as both are already absorbed in the earnings trajectory and a higher multiple would double-count growth already in the model.

The market assumption for the forward P/E as of February 2026 stands at 49.4x, down from 53.9x at November 2024, as the rotisserie chicken lawsuits and tariff litigation compressed investor willingness to pay above 50x for a business with 3.8% operating margins, and the model’s 44.8x exit sits 5 points below the current market assumption to account for litigation resolution uncertainty through fiscal 2028.

At 44.8x, the exit multiple reflects the scarcity premium investors historically assign Costco stock for its membership renewal model and warehouse traffic consistency, while also acknowledging that legal expense risk from 2 class action lawsuits and potential tariff cost pass-through limit the re-rating capacity above the current 49.4x market assumption.

If rotisserie chicken litigation results in material damages or the Supreme Court rules against the tariff challenge and import costs rise, earnings compression below the 4.0% operating margin assumption pushes the sustainable multiple toward the 37.4x EV/EBIT market assumption rather than sustaining near 45x, and the $1,183 price target collapses toward the 1-year historical stock price of $1,056.

This sits below the 1-year historical P/E of 48.9x, as the litigation risk from 2 active class action lawsuits and tariff court uncertainty justify a valuation discount versus the trailing year, and sustaining even 44.8x through August 2028 requires both margin expansion to 4.0% and litigation resolution without material earnings impact.

What Happens If Things Go Better or Worse?

Costco stock results are shaped by warehouse traffic frequency, SG&A cost discipline against a $275 billion revenue base, and litigation resolution across 2 active class action lawsuits through August 2030.

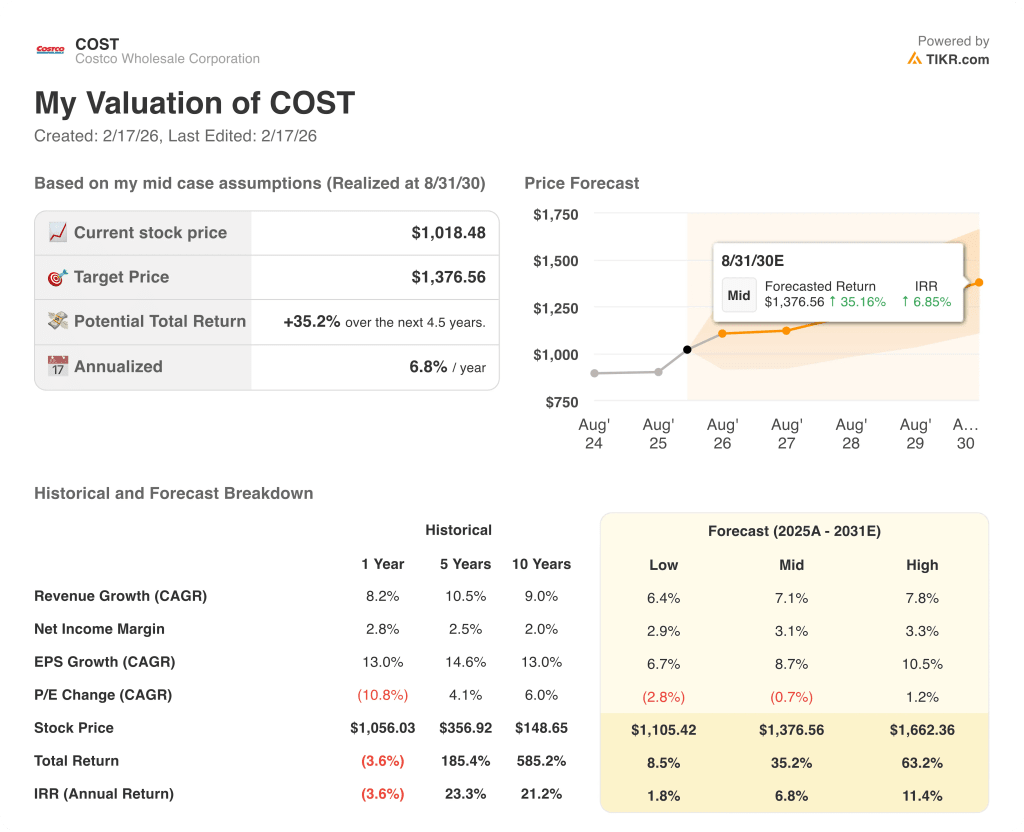

- Low Case: If rotisserie chicken litigation costs escalate and tariff duties compress margins, revenue grows 6% and net margins hold near 3% → 2% annualized return.

- Mid Case: With comparable traffic up 2% and digitally-enabled sales sustaining 34% growth, revenue grows 7% and net margins reach 3% → 7% annualized return.

- High Case: If nofoods category outperformance continues and litigation resolves without material cost, revenue grows 8% and net margins approach 3% → 11% annualized return.

How Much Upside Does Costco Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!