Key Takeaways:

- Digital Transformation: Companies are consolidating reporting and compliance solutions onto unified platforms, driving multi-solution adoption.

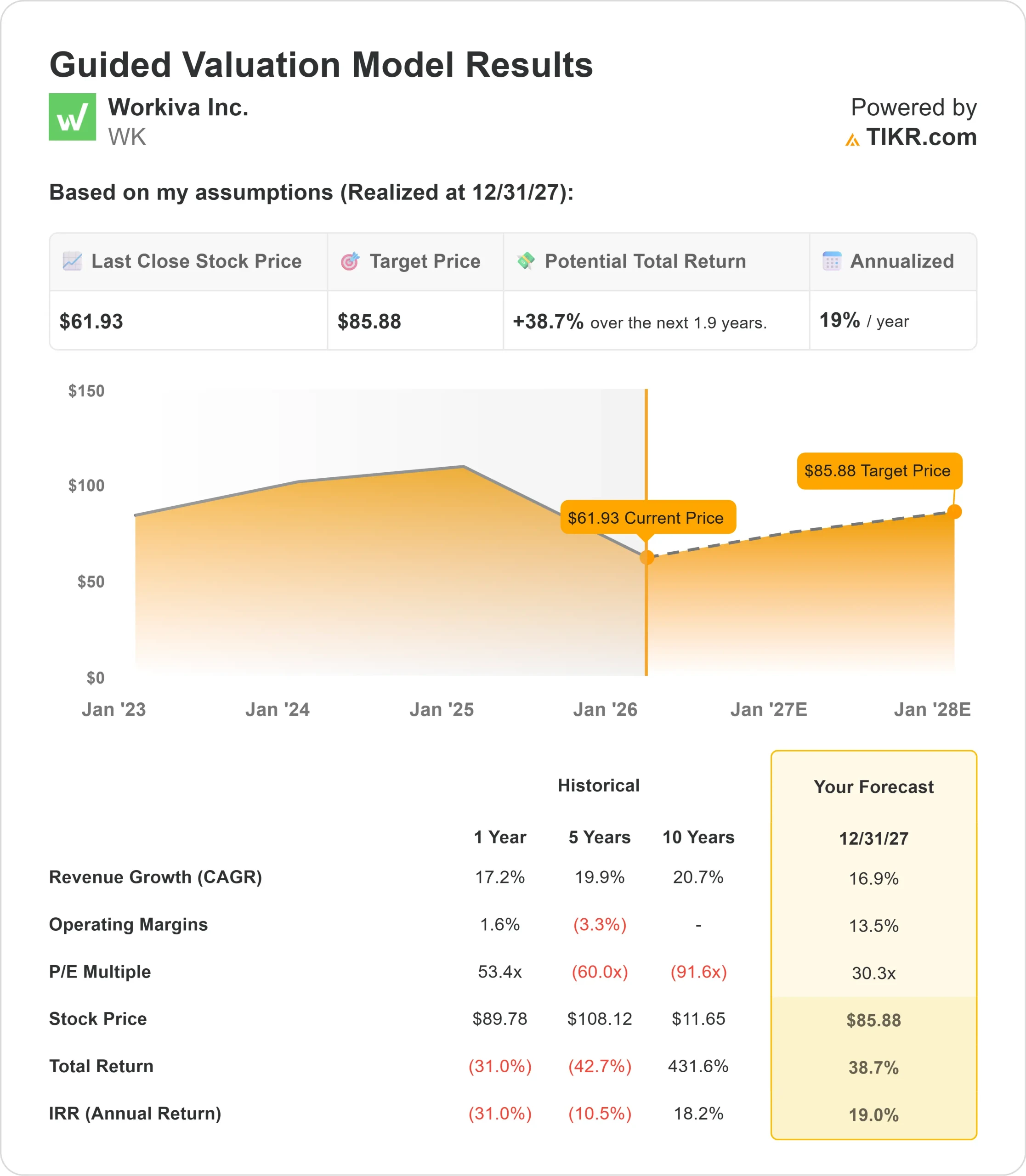

- Price Projection: Based on current execution, WK stock could reach $86 by December 2027.

- Potential Gains: This target implies a total return of 39% from the current price of $62.

- Annual Return: Investors could see roughly 19% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Workiva Inc. (WK) delivered a strong third quarter in 2025 with 23% subscription revenue growth and raised full-year guidance across key metrics. The company now expects subscription revenue to grow at least 21% year-over-year.

CEO Julie Iskow highlighted robust demand across the company’s broad portfolio of solutions.

- The platform continues to win large enterprise deals as organizations seek to consolidate financial reporting, sustainability disclosures, and governance, risk, and compliance (GRC) functions onto a single platform.

- Large contract growth accelerated significantly. Contracts valued over $100,000 increased 23%, those over $300,000 jumped 41%, and deals exceeding $500,000 surged 42% compared to Q3 2024.

- This momentum was driven by both new customer wins and substantial expansions within the existing base.

- The company’s unified platform approach is resonating with customers managing complex reporting requirements.

- With 73% of subscription revenue now coming from multi-solution customers (up from 68% a year ago), Workiva demonstrates clear value in helping organizations trust their numbers, provide transparency, and maintain accountability with built-in assurance.

Despite strong fundamentals and an expanding product portfolio, Workiva trades at $62, offering upside for investors who recognize the company’s position in critical enterprise infrastructure for compliance and reporting.

See analysts’ full growth forecasts and estimates for WK stock (It’s free) >>>

What the Model Says for Workiva Stock

We analyzed Workiva, which is transforming enterprise reporting and compliance with its AI-powered platform. The company benefits from multiple structural demand drivers.

Organizations are moving away from fragmented legacy systems and manual spreadsheet processes. Workiva’s platform addresses this by unifying financial reporting (SEC, ESEF, multi-entity), sustainability disclosures (CSRD, ISSB), and GRC solutions on a single system with connected data and embedded controls.

International expansion provides additional upside. Revenue outside the Americas now represents over 19% of total revenue, up from 17% a year ago.

Europe has shown particularly strong momentum with broad-based demand across solutions.

The company’s financial services vertical continues to grow.

Q3 saw notable wins, including a seven-figure deal with a European fund services administrator managing 2,500 funds, and a mid-six-figure expansion with one of Europe’s top 10 banks adopting five solutions.

Using a forecast of 16.9% annual revenue growth and 13.5% operating margins, our model projects the stock will rise to $86 within 1.9 years. This assumes a 30.3x price-to-earnings multiple.

That represents compression relative to Workiva’s historical P/E average of 53.4x (one-year). The lower multiple reflects the company’s evolution from a high-growth, low-margin phase to a more balanced growth and profitability profile.

Management delivered non-GAAP operating margin of 12.7% in Q3, an 860 basis point improvement year-over-year, demonstrating tangible progress toward medium-term margin targets.

The real value lies in capturing platform consolidation trends as enterprises modernize their reporting infrastructure while the company scales margins through operational efficiency.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for WK stock:

1. Revenue Growth: 16.9%

Workiva’s growth centers on platform adoption and multi-solution expansion. The company delivered 23% subscription growth in Q3, with particularly strong performance in large enterprise deals.

A net retention rate of 114% indicates healthy expansion in the customer base. Multi-solution adoption continues climbing as customers recognize the value of consolidating on a single platform for financial, sustainability, and GRC reporting.

Recent wins showcase this dynamic. A top-five global pharmaceutical company nearly tripled spending with a mid-six-figure expansion into sustainability and GRC. A North American telecommunications company more than doubled its investment, expanding from two to six solutions.

The IPO market recovery provides additional tailwinds. Q3 saw notable activity with Workiva supporting high-profile listings.

Beyond S-1 filings, a stronger IPO environment expands the addressable market for SEC reporting and internal controls as more private companies prepare for public markets.

2. Operating margins: 13.5%

Workiva has expanded non-GAAP operating margins dramatically, delivering 12.7% in Q3 2025 versus 4.1% a year ago. This performance reflects focused execution of productivity initiatives across all functions.

Management is driving leverage through organizational redesign, process automation, and optimized resource allocation.

The company is shifting low-margin setup and consulting services to partners, scaling digital support, and improving R&D productivity through workforce diversification and engineering efficiency.

Sales productivity remains the largest opportunity.

Initiatives include transitioning to more efficient territory structures, upgrading seller talent with platform-selling experience, and optimizing coverage models to drive better new-logo acquisition and account expansion.

3. Exit P/E Multiple: 30.3x

The market values Workiva at 30.3x current earnings. We assume this multiple holds through our forecast period as the company demonstrates balanced growth and margin expansion.

The valuation reflects Workiva’s transition from pure growth to profitable scaling.

While historical multiples were significantly higher during the high-growth, low-margin phase, the current multiple appropriately values a company delivering strong revenue growth with improving profitability.

As Workiva continues executing on platform consolidation and demonstrates operational leverage, the company should maintain a premium multiple.

The appointment of Michael Pinto as Chief Revenue Officer signals management’s focus on scaling efficiently from $1 billion in revenue to multi-billion-dollar revenue.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

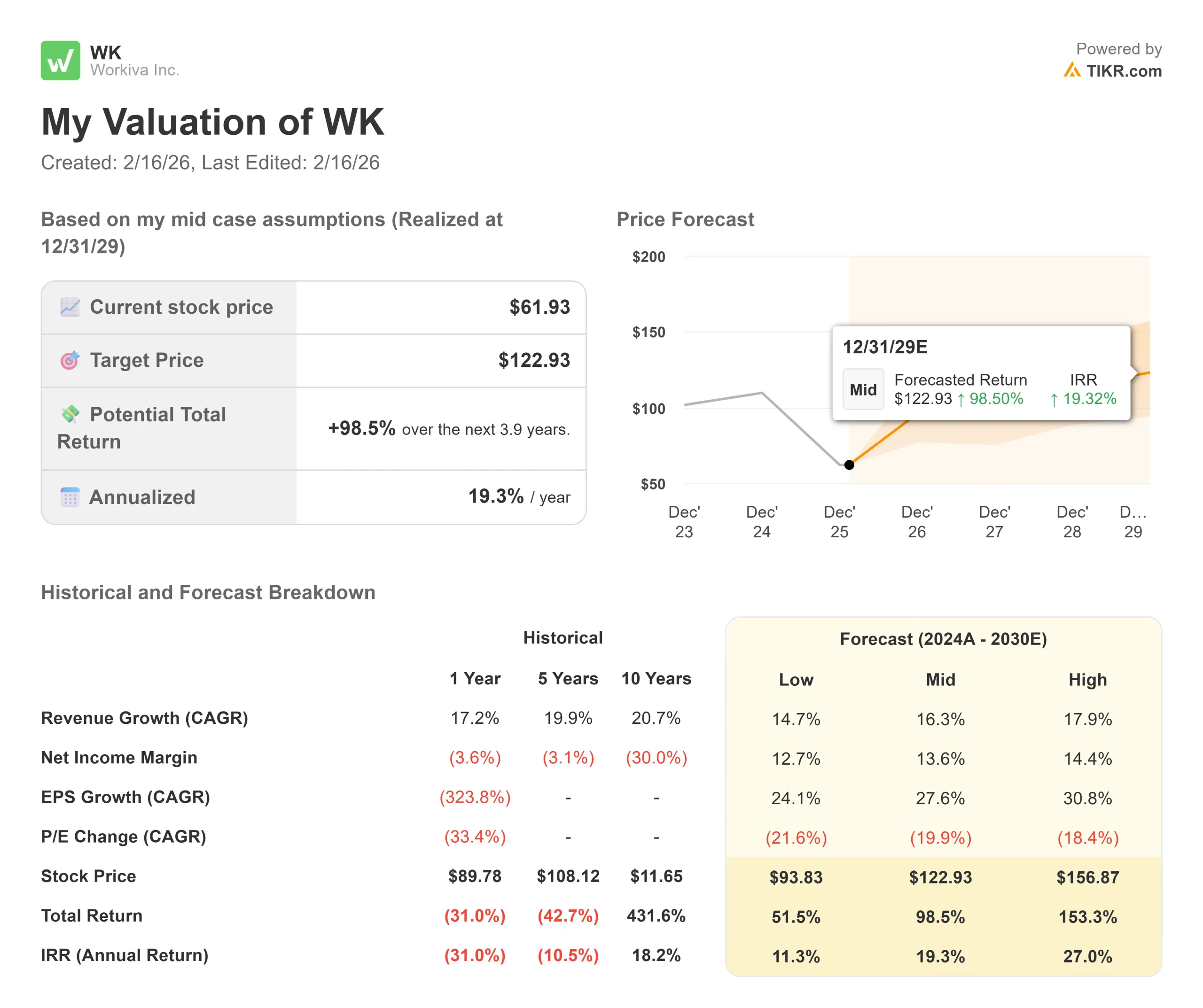

Enterprise software companies face execution risks and market dynamics. Here’s how Workiva stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth moderates to 14.7% and net income margins reach 12.7%, investors could see a 52% total return (11% annually).

- Mid Case: With 16.3% growth and 13.6% margins, we expect a total return of 99% (19% annually).

- High Case: If platform adoption accelerates, driving 17.9% revenue growth while Workiva achieves 14.4% margins, returns could hit 153% total (27% annually).

See what analysts think about WK stock right now (Free with TIKR) >>>

The range reflects execution on multi-solution expansion, international growth, and margin improvement initiatives.

In the low case, competitive pressure or slower enterprise adoption could moderate growth.

In the high case, platform consolidation accelerates faster than expected, international markets exceed projections, and operational efficiency drives margin expansion ahead of schedule.

How Much Upside Does Workiva Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!