Key Takeaways:

- AI Innovation: Qualys is pioneering agentic AI-powered risk management with exploit validation and autonomous remediation.

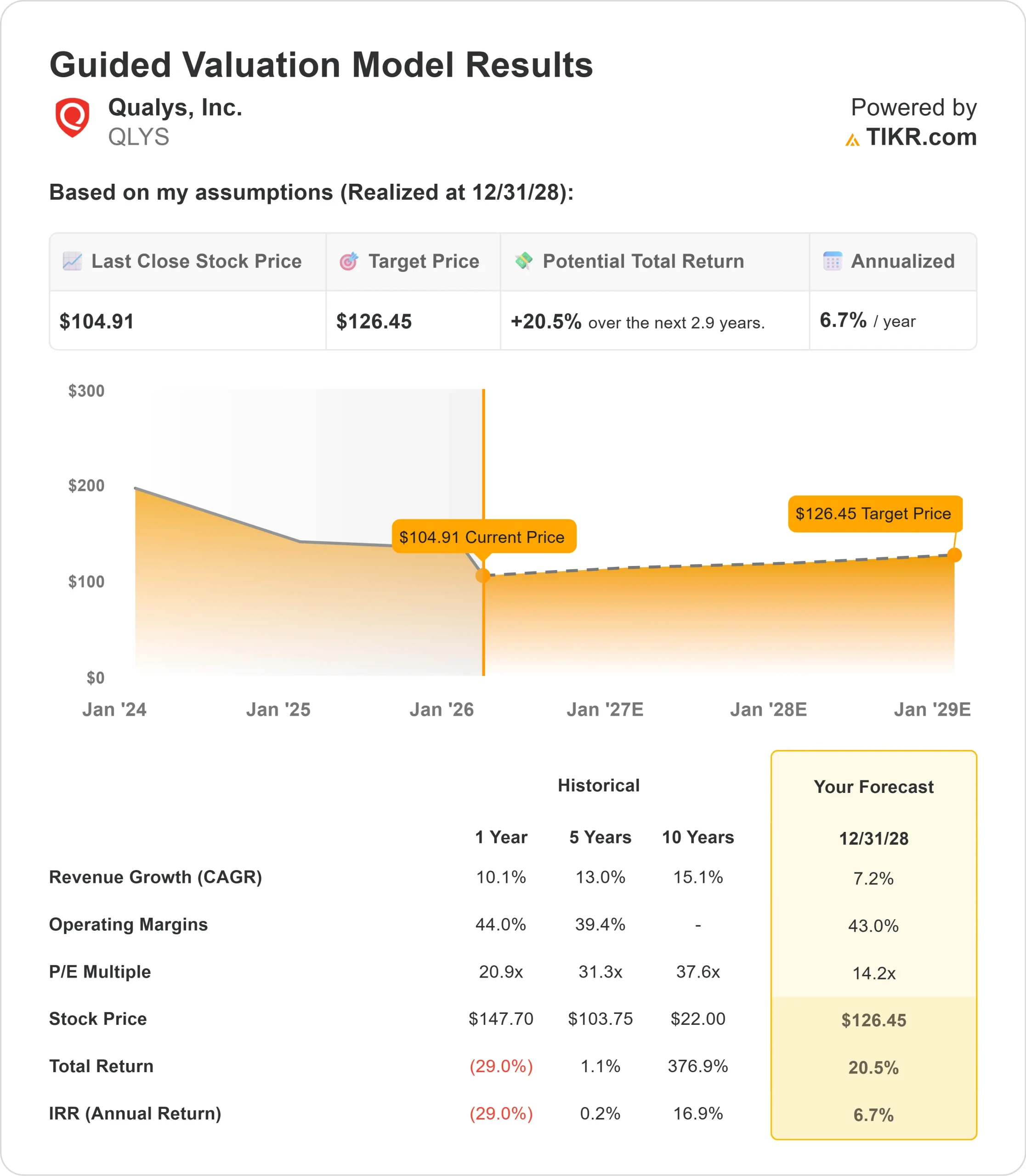

- Price Projection: Based on current execution, QLYS stock could reach $126 by December 2028.

- Potential Gains: This target implies a total return of 20% from the current price of $105.

- Annual Return: Investors could see roughly 7% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Qualys (QLYS) posted solid fourth-quarter 2025 results with 10% revenue growth and maintained its strong profitability profile. The company now expects revenue growth of 7-8% for 2026, driven by its Enterprise ThreatScan Management (ETM) platform and partner-led initiatives.

CEO Sumedh Thakar emphasized the company’s shift toward redefining pre-breach risk management.

- As cyber threats accelerate with AI-powered attacks, traditional vulnerability management tools that simply detect exposures are no longer sufficient.

- Qualys is addressing this gap by building the industry’s first agentic AI-native Risk Operations Center (ROC), which not only identifies vulnerabilities but also validates exploitability, quantifies business risk in dollar terms, and autonomously remediates threats.

- The company’s Agent Val technology confirms whether vulnerabilities are actually exploitable in a customer’s specific environment before remediation begins.

- This eliminates wasted IT resources chasing theoretical risks that existing security controls already mitigate.

- According to recent Mandiant data, the mean time to exploit is now negative one day, indicating attackers are exploiting vulnerabilities before patches are even available.

- Qualys deployed 140 million patches in the last year alone, demonstrating the operational value of integrated remediation.

- Qualys also expanded its ETM platform with Identity Security Posture Management (ISPM) to secure the new AI perimeter and launched an AI marketplace where customers can deploy specialized autonomous agents for tasks such as patch management and exploit validation.

- These agents augment security teams without requiring additional headcount, a critical advantage as talent shortages persist across the industry.

- Federal business momentum accelerated after Qualys achieved FedRAMP High authorization in late 2025, opening opportunities for multi-agency deployments.

- The company secured multiple six-figure federal expansions in Q4, including a shared services program serving several large government agencies.

- Partner-led deal registrations continued growing in Q4 as Qualys certified more managed ROC (mROC) partners.

- These partners can now offer high-value risk quantification services that command premium pricing compared to traditional vulnerability scanning, creating a win-win model that brings new business to Qualys while expanding partner margins.

Despite strong fundamentals and differentiated AI capabilities, Qualys trades at $105, leaving room for upside for investors who recognize the company’s evolution from vulnerability scanning to comprehensive risk operations.

See analysts’ full growth forecasts and estimates for QLYS stock (It’s free) >>>

What the Model Says for Qualys Stock

We analyzed Qualys as it transformed into an agentic, AI-powered risk management platform with autonomous remediation capabilities.

- The company benefits from structural demand drivers as organizations shift budgets toward proactive pre-breach solutions.

- Traditional Security Operations Centers (SOCs) focused on post-breach detection have consumed significant spending over the past decade.

- Now, customers are reallocating resources to prevent breaches before they occur, favoring unified platforms over fragmented point solutions that generate ‘dashboard fatigue’ without reducing actual risk.

- Qualys’s ETM platform addresses this need by consolidating risk signals from multiple sources into a single orchestration layer with business-contextual quantification and automated remediation.

- This enables customers to consolidate their security stack while improving outcomes, creating both immediate operational savings and long-term strategic value.

- The QFlex pricing model, introduced in beta in 2025, allows customers to adopt ETM capabilities progressively throughout their subscription period.

- This flexibility reduces friction for VMDR customers upgrading to ETM while maintaining revenue quality.

Using a forecast of 7.2% annual revenue growth and 43% operating margins, our model projects the stock will rise to $126 within 2.9 years. This assumes a 14.2x price-to-earnings multiple.

That represents compression from Qualys’s historical P/E averages of 20.9x (one year) and 31.3x (five years). The lower multiple reflects near-term uncertainty as ETM adoption remains in early stages despite encouraging customer feedback.

Management will begin providing specific ETM metrics starting in Q1 2026 earnings, which should improve visibility.

The real value lies in capturing the shift toward vendor-agnostic risk operations platforms and expanding higher-margin products such as Patch Management, TotalCloud, and ETM across the customer base.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for QLYS stock:

1. Revenue Growth: 7.2%

Qualys expects 7-8% revenue growth for 2026 based on stable net dollar expansion of around 103% and moderate new business contribution.

The company delivered 10% consolidated organic growth in 2025, with channel partner revenue up 17%, outpacing direct sales growth of 4%.

Management expects the selling environment to remain similar to 2025, with low- to mid-single-digit growth in security spending continuing.

Differentiated products, including ETM, Patch Management, and TotalCloud, are increasing their contribution to bookings, providing growth levers as adoption expands.

2. Operating margins: 43%

Qualys maintained 47% EBITDA margin in 2025 despite 14% growth in sales and marketing investments.

For 2026, management guides to a mid-40s EBITDA margin, implying a modest contraction as the company invests in building the pipeline, accelerating partner programs, and expanding its federal vertical presence.

These investments position Qualys for larger ETM upsells over time while maintaining profitability at a similar level.

3. Exit P/E Multiple: 14.2x

The market values Qualys at 14.2x current earnings. We assume this multiple holds over our forecast period.

The valuation reflects uncertainty about the pace of ETM adoption and the timing of revenue acceleration.

As Qualys demonstrates consistent ETM traction, successful federal deployments, and partner-driven growth, the multiple should expand toward historical averages, especially given the company’s cash generation and strategic positioning in a growing market.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

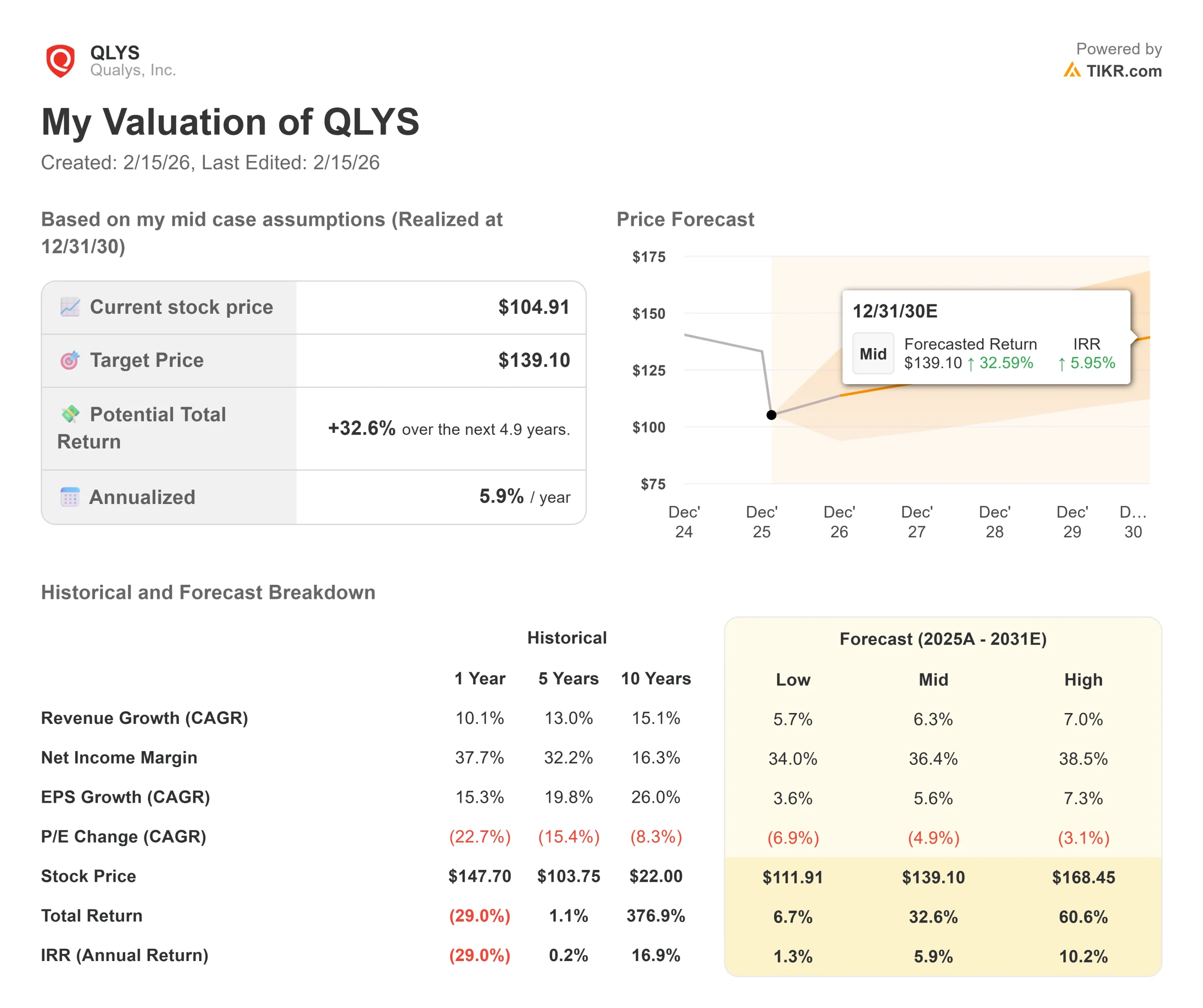

Risk management platforms face execution challenges around product adoption and competitive dynamics. Here’s how Qualys stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth moderates to 5.7% annually and net income margins compress to 34%, investors still see a 7% total return (1.3% annually).

- Mid Case: With 6.3% growth and 36.4% margins, we expect a total return of 33% (5.9% annually).

- High Case: If ETM acceleration drives 7% revenue growth while Qualys maintains 38.5% margins, returns could hit 61% total (10.2% annually).

See what analysts think about QLYS stock right now (Free with TIKR) >>>

The range reflects execution on ETM adoption, federal market expansion, and partner ecosystem leverage.

In the worst case, customers delay ETM upgrades or competitive pressure intensifies.

In the best case, the ROC model gains rapid traction, federal deployments scale faster than expected, and mROC partners drive significant new business.

How Much Upside Does Qualys Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!